Chiến lược theo dõi xu hướng đa khung thời gian

Tổng quan

Chiến lược giao dịch theo xu hướng đa khung thời gian là một chiến lược bắt xu hướng kết hợp nhiều đường trung bình động và đường hồi quy khác nhau. Chiến lược này có thể lựa chọn từ hơn 20 chỉ báo xu hướng khác nhau, thực hiện tự động mua và bán.

Nguyên lý chiến lược

Cốt lõi của chiến lược là dựa vào chỉ báo xu hướng do người dùng lựa chọn để xác định giá đang ở xu hướng tăng hay giảm. Đầu tiên, chiến lược tính toán hơn 20 đường trung bình động và đường hồi quy. Các chỉ báo này bao gồm các chỉ báo có trong thư viện chuẩn của ngôn ngữ lập trình Pine như đường trung bình động đơn giản, đường trung bình động trọng số, đường trung bình động hàm mũ, cũng như một số chỉ báo tùy chỉnh do cộng đồng Pine phát triển. Sau đó, chiến lược truy vấn các chỉ báo này để lấy giá trị hiện tại của một chỉ báo nhất định, và so sánh với giá trị của chu kỳ trước đó. Nếu giá trị hiện tại lớn hơn giá trị trước đó, xu hướng là tăng; ngược lại, nếu giá trị hiện tại nhỏ hơn giá trị trước đó, xu hướng là giảm. Cuối cùng, chiến lược dựa vào hướng xu hướng để quyết định có nên mở vị thế mua hay không. Mở vị thế mua trong xu hướng tăng và đóng vị thế trong xu hướng giảm.

Phân tích ưu điểm

Chiến lược này kết hợp hơn 20 chỉ báo để xác định xu hướng, tránh khả năng sai lầm khi chỉ dựa vào một chỉ báo duy nhất. Hơn nữa, các chỉ báo này đều đã được các nhà phát triển trong cộng đồng xác thực. Có thể điều chỉnh bằng các tham số khác nhau, phù hợp với nhiều môi trường thị trường khác nhau.

So với chiến lược hai đường trung bình động đơn giản, chiến lược này chỉ phụ thuộc vào một chỉ báo duy nhất để xác định hướng xu hướng, có thể thể hiện xu hướng tốt hơn và không xuất hiện tín hiệu giả gây mâu thuẫn.

Phân tích rủi ro

Chiến lược này phụ thuộc vào chỉ báo để xác định xu hướng và không thể xác định liệu xu hướng đã đảo chiều hay chưa. Do đó sẽ có một mức độ trễ nhất định. Điều này có thể dẫn đến thua lỗ hoặc bỏ lỡ cơ hội. Có thể giảm nhẹ vấn đề này bằng cách điều chỉnh tham số chỉ báo.

Sau khi xảy ra các sự kiện bất ngờ, tất cả các chiến lược theo xu hướng đều sẽ chịu lỗ lớn. Cần thiết lập cắt lỗ để kiểm soát rủi ro.

Hướng tối ưu hóa

Có thể xem xét kết hợp các chỉ báo khác để dự đoán sự đảo chiều xu hướng, nhằm giảm vấn đề trễ. Ví dụ, kết hợp chỉ báo Bollinger Band để xác định xem giá có đang mở rộng quá mức hay không.

Có thể thiết kế cơ chế cắt lỗ khẩn cấp cho các sự kiện bất ngờ. Ví dụ, kích hoạt cắt lỗ bắt buộc khi mức lỗ vượt quá 5% trong một ngày giao dịch.

Tổng kết

Chiến lược giao dịch theo xu hướng đa khung thời gian kết hợp hơn 20 chỉ báo để xác định xu hướng, có thể thể hiện đầy đủ xu hướng thị trường và tránh tín hiệu giả. Đồng thời vẫn giữ được tính tùy chỉnh cao, phù hợp với các môi trường thị trường khác biệt lớn. Đây là một chiến lược bắt xu hướng rất hiệu quả. Bằng cách thiết lập cắt lỗ phù hợp và tối ưu hóa tham số chỉ báo, có thể đạt được lợi nhuận tốt trong khi kiểm soát rủi ro.

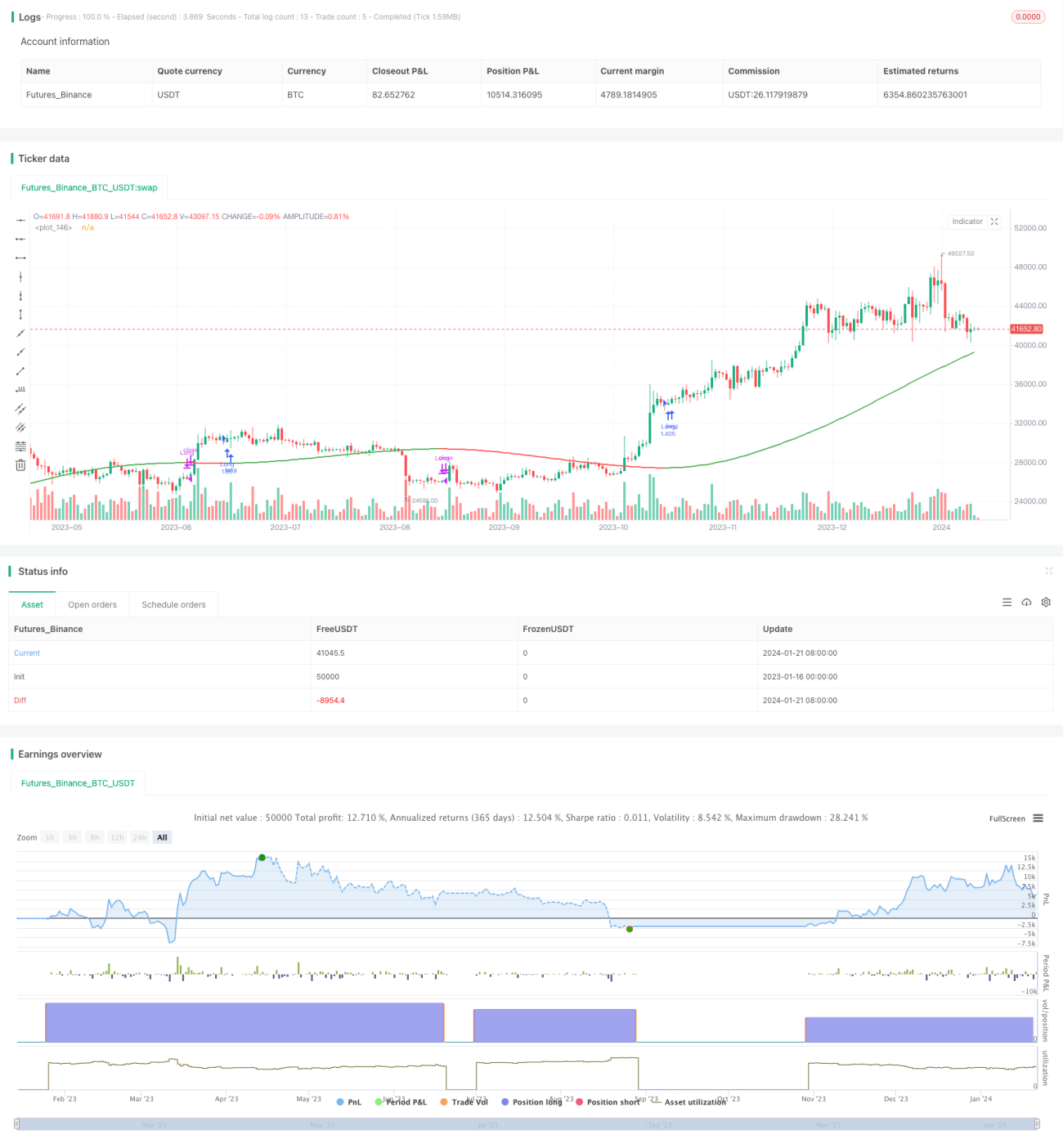

/*backtest

start: 2023-01-16 00:00:00

end: 2024-01-22 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// @version=5

// Author = TradeAutomation

- 1