Chiến lược nén động lượng gấu lười

Tổng quan

Chiến lược nén động lượng Lazy Bear là một chiến lược giao dịch định lượng kết hợp Bollinger Bands, Kênh Keltner và chỉ báo động lượng. Nó sử dụng Bollinger Bands và Kênh Keltner để xác định xem thị trường hiện tại có đang ở trạng thái nén hay không, sau đó kết hợp với chỉ báo động lượng để tạo ra tín hiệu giao dịch.

Ưu điểm chính của chiến lược này là có thể tự động nhận diện sự khởi đầu của một xu hướng và kết hợp với chỉ báo động lượng để xác định thời điểm vào lệnh. Tuy nhiên, nó cũng tồn tại một số rủi ro nhất định và cần được tối ưu hóa tham số cho từng loại tài sản khác nhau.

Nguyên lý chiến lược

Chiến lược nén động lượng Lazy Bear đánh giá dựa trên ba chỉ báo sau:

- Bollinger Bands: bao gồm đường giữa, đường trên và đường dưới

- Kênh Keltner: bao gồm đường giữa, đường trên và đường dưới

- Chỉ báo Động lượng (Momentum Indicator): chênh lệch giữa giá hiện tại và giá cách đây n ngày

Khi đường trên của Bollinger Bands thấp hơn đường trên của Kênh Keltner, đồng thời đường dưới của Bollinger Bands cao hơn đường dưới của Kênh Keltner, chúng ta cho rằng thị trường đang ở trạng thái nén. Điều này thường có nghĩa là xu hướng sắp bắt đầu.

Để xác định thời điểm vào lệnh, chúng ta sử dụng chỉ báo động lượng để đánh giá tốc độ thay đổi giá. Khi động lượng vượt lên trên giá trị trung bình của nó, tín hiệu mua được tạo ra; khi động lượng phá vỡ xuống dưới giá trị trung bình của nó, tín hiệu bán được tạo ra.

Phân tích ưu điểm chiến lược

Các ưu điểm chính của chiến lược nén động lượng Lazy Bear bao gồm:

- Có thể tự động nhận diện thời điểm bắt đầu xu hướng, vào lệnh sớm

- Kết hợp nhiều chỉ báo để đánh giá, tránh tín hiệu giả

- Cân bằng cả hai phương pháp giao dịch theo xu hướng và đảo chiều

- Có thể tùy chỉnh tham số để tối ưu hóa cho các loại tài sản khác nhau

Phân tích rủi ro

Chiến lược nén động lượng Lazy Bear cũng tồn tại một số rủi ro nhất định:

- Xác suất Bollinger Bands và Kênh Keltner phát ra tín hiệu giả khá cao

- Chỉ báo động lượng hoạt động không ổn định, có thể bỏ lỡ điểm vào lệnh tối ưu

- Cần tối ưu hóa tham số, nếu không hiệu quả sẽ kém

- Hiệu quả phụ thuộc nhiều vào loại tài sản giao dịch

Để giảm thiểu rủi ro, khuyến nghị tối ưu hóa tham số độ dài của Bollinger Bands và Kênh Keltner, điều chỉnh điểm dừng lỗ, lựa chọn các loại tài sản giao dịch có thanh khoản tốt, đồng thời kết hợp với các chỉ báo khác để xác minh.

Hướng tối ưu hóa chiến lược

Để tăng cường hơn nữa hiệu quả của chiến lược nén động lượng Lazy Bear, các hướng tối ưu hóa chính bao gồm:

- Kiểm tra các tổ hợp tham số cho các loại tài sản và khung thời gian khác nhau

- Tối ưu hóa độ dài của Bollinger Bands và Kênh Keltner

- Tối ưu hóa độ dài của chỉ báo động lượng

- Xây dựng chiến lược dừng lỗ và chốt lời khác nhau cho vị thế mua và bán

- Thêm các chỉ báo khác để xác minh tín hiệu

Thông qua kiểm tra và tối ưu hóa đa chiều, có thể cải thiện đáng kể tỷ lệ thắng và khả năng sinh lời của chiến lược này.

Tổng kết

Chiến lược nén động lượng Lazy Bear tích hợp nhiều chỉ báo với khả năng đánh giá mạnh mẽ, có thể nhận diện hiệu quả thời điểm bắt đầu xu hướng. Tuy nhiên, nó cũng tồn tại một số rủi ro nhất định và cần được tối ưu hóa tham số cho các loại tài sản giao dịch khác nhau. Thông qua kiểm tra và tối ưu hóa liên tục, chiến lược này có thể trở thành một hệ thống giao dịch thuật toán hiệu quả.

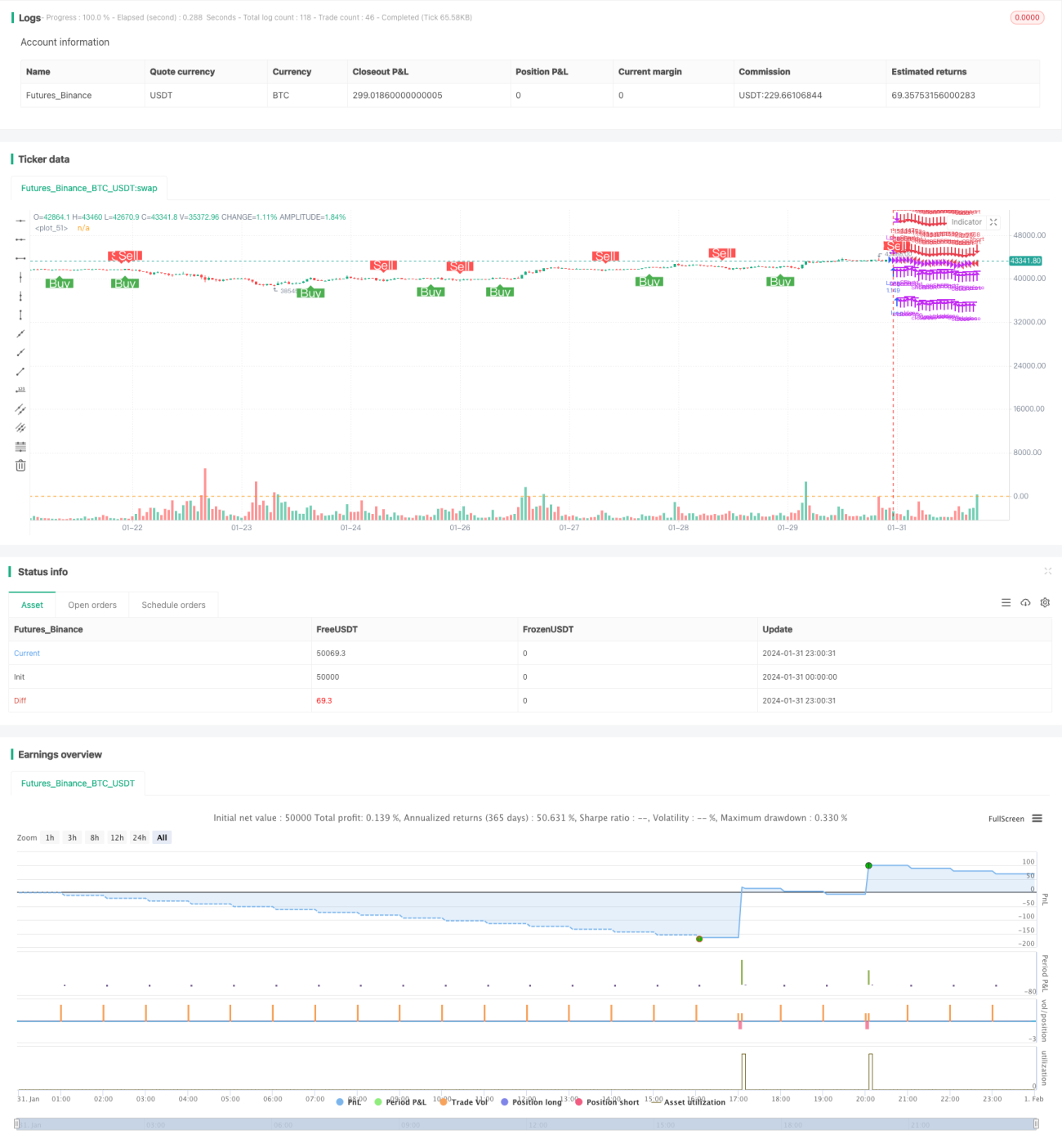

/*backtest

start: 2024-01-31 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mtahreemalam original strategy by LazyBear

- 1