Handelsstrategie mit dem gleitenden Durchschnittsindikator

Strategieübersicht

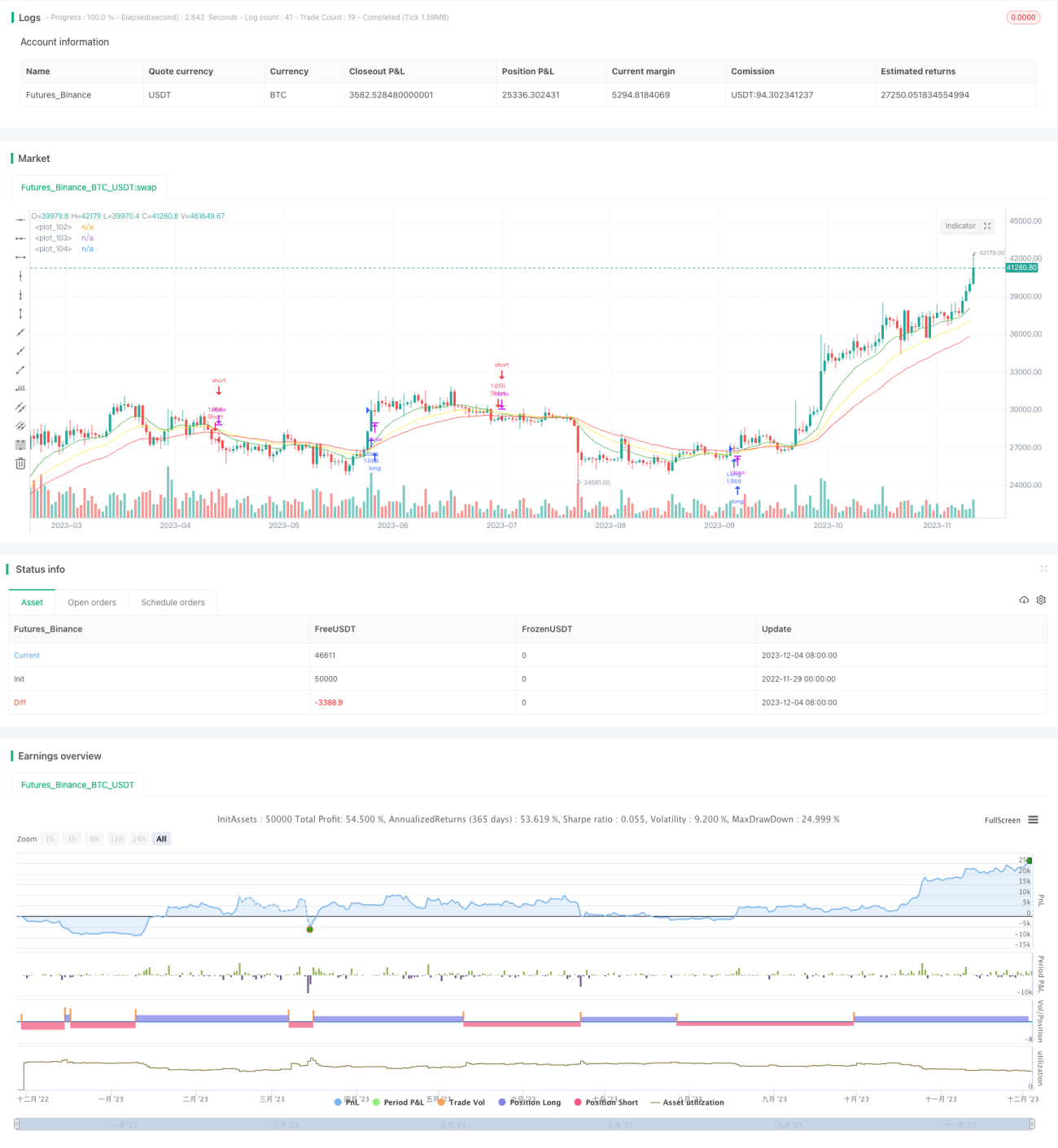

Diese Strategie generiert Handelssignale basierend auf mehreren gleitenden Durchschnitten. Sie berücksichtigt gleichzeitig kurzfristige, mittelfristige und langfristige gleitende Durchschnitte und ermittelt anhand deren Kreuzungen die Trendrichtung, um Handelssignale zu erzeugen.

Strategiename

Multi Moving Average Crossover Strategy (Mehrfach-Gleitender-Durchschnitt-Kreuzungsstrategie)

Strategieprinzip

Die Strategie verwendet gleichzeitig drei gleitende Durchschnitte mit unterschiedlichen Perioden, darunter den 7-Tage-, den 13-Tage- und den 21-Tage-Durchschnitt. Die Handelslogik basiert auf den folgenden Punkten:

- Wenn der kurzfristige 7-Tage-Durchschnitt den mittelfristigen 13-Tage-Durchschnitt von unten nach oben kreuzt und der langfristige 21-Tage-Durchschnitt im Aufwärtstrend ist, wird ein Long-Signal generiert.

- Wenn der kurzfristige 7-Tage-Durchschnitt den mittelfristigen 13-Tage-Durchschnitt von oben nach unten kreuzt und der langfristige 21-Tage-Durchschnitt im Abwärtstrend ist, wird ein Short-Signal generiert.

Durch die Kombination gleitender Durchschnitte unterschiedlicher Zeiträume kann der Markttrend genauer eingeschätzt und fehlerhafte Trades vermieden werden.

Strategievorteile

- Die Verwendung mehrerer gleitender Durchschnitte ermöglicht eine präzisere Beurteilung der Marktentwicklung und verhindert Fehlinterpretationen durch falsche Ausbrüche oder kurzfristige Schwankungen.

- Signale werden nur bei klarem Trend generiert, wodurch die Anzahl unnötiger Trades reduziert und Transaktionskosten gesenkt werden.

- Die Parametereinstellung ist flexibel; die Perioden der gleitenden Durchschnitte können je nach persönlichen Präferenzen angepasst werden, um sich verschiedenen Instrumenten und Marktbedingungen anzupassen.

Strategierisiken

- In seitwärts tendierenden oder konsolidierenden Märkten können häufige Fehlsignale auftreten.

- Gleitende Durchschnitte als trendfolgende Indikatoren können Trendwenden nicht präzise identifizieren.

- Kreuzungen von gleitenden Durchschnitten erkennen Trends verzögert, wodurch ein Teil der Gewinne verpasst werden kann.

- Durch die Einführung anderer technischer Indikatoren zur Signalverifizierung und Optimierung der Parameter gleitender Durchschnitte können Risiken reduziert werden.

Optimierungsmöglichkeiten

- Einbeziehung von Volatilitätsindikatoren zur Beurteilung der Trendstärke, um Handel in Seitwärtsmärkten zu vermeiden.

- Einsatz quantitativer Techniken wie maschinelles Lernen zur automatischen Optimierung der Parameter gleitender Durchschnitte.

- Hinzufügen von Stop-Loss-Strategien, um Verluste bei zunehmenden Verlusten rechtzeitig zu begrenzen.

- Bei Kreuzungen gleitender Durchschnitte die Verwendung von Limit-Orders zur Reduzierung von Slippage in Betracht ziehen.

Zusammenfassung

Diese Strategie kombiniert kurzfristige, mittelfristige und langfristige gleitende Durchschnitte und beurteilt den Markttrend anhand ihrer Kreuzungsbeziehungen. Sie stellt eine relativ stabile und effiziente Trendfolgestrategie dar. Durch die Optimierung von Indikatorparametern, Stop-Loss-Mechanismen und Orderausführungsarten können Trefferquote und Rentabilität weiter gesteigert werden.

- 1