Drei-Vier-Kerzen-Durchbruch-Umkehrstrategie

Übersicht

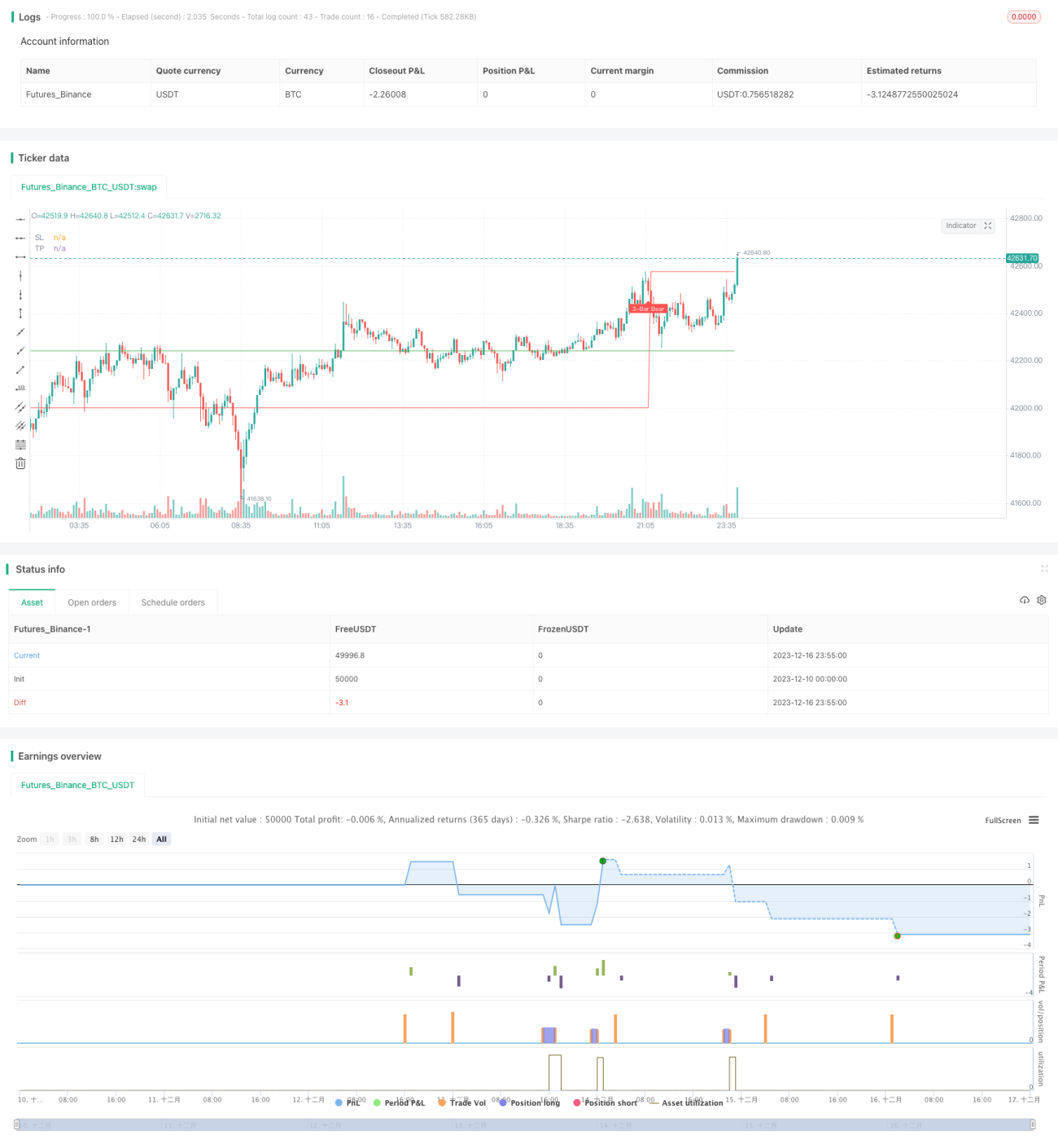

Die Drei-Vier-Kerzen-Ausbruchs-Umkehrstrategie identifiziert drei oder vier Kerzen mit starkem Aufwärts- oder Abwärtsmomentum. Nachdem die folgenden, kleineren Kerzen eine Unterstützung oder einen Widerstand gebildet haben, wird bei Eintreten einer Umkehrkerze gegen den Trend gehandelt. Es handelt sich um eine konträre Handelsstrategie.

Strategieprinzip

Der Kern der Erkennungslogik dieser Strategie besteht aus folgenden Teilen:

-

Erkennung von Kerzen mit vergrößerter Spanne (Gap Bar): Diese überschreiten das 1,5-fache des durchschnittlichen ATR, der Körperanteil beträgt mehr als 0,65. Diese Kerze wird als stark trendstark eingestuft.

-

Erkennung von schrumpfenden, seitwärts tendierenden Kerzen (Collecting Bar): 1-2 Kerzen mit geringer Schwankungsbreite, die der Gap Bar folgen, deren Hoch- oder Tiefpunkte nahe an der Gap Bar liegen. Diese Kerzen repräsentieren eine Verlangsamung des Trends und eine Konsolidierung, die Unterstützung oder Widerstand bildet.

-

Erkennung von Umkehrsignal-Kerzen: Nach den konsolidierenden Kerzen, wenn eine Kerze den Hoch- oder Tiefpunkt der vorherigen Kerzen durchbricht, kann dies als Umkehrsignal betrachtet werden. Die Position wird in Richtung des Durchbruchs (long oder short) eröffnet.

-

Stop-Loss und Take-Profit: Der Stop-Loss wird unter dem Tief oder über dem Hoch der Gap-Kerze gesetzt; der Take-Profit wird auf Basis des Stop-Loss multipliziert mit dem konfigurierten Gewinn-Verlust-Verhältnis berechnet.

Vorteilsanalyse

Die Strategie bietet folgende Hauptvorteile:

-

Sie nutzt die Eigenschaften der Kerzen selbst, um Trends und Umkehrpunkte zu identifizieren, ohne auf Indikatoren angewiesen zu sein – „Indikator inklusive".

-

Die strengen Auswahlkriterien für Gap Bar und Collecting Bar ermöglichen eine effektive Erkennung echter Trends und Konsolidierungen.

-

Die Beurteilung des Umkehrsignals basiert auf dem Kerzenkörper, was die Wahrscheinlichkeit von Fehlsignalen verringert.

-

Es sind nur 3-4 Kerzenkombinationen für einen Trade erforderlich, was kurze Zeiträume und hohe Frequenz ermöglicht.

-

Stop-Loss und Take-Profit sind klar definiert, sodass Drawdown und Risiko-Ertrags-Verhältnis leicht kontrollierbar sind.

Risikoanalyse

Die Strategie birgt auch folgende Risiken:

-

Abhängigkeit von der Qualität der Parametereinstellungen: Bei zu lockeren Einstellungen steigt die Wahrscheinlichkeit von Fehlsignalen und Verlusttrades.

-

Anfällig für häufige Fehlausbrüche (falsche Durchbrüche), die nicht vollständig gefiltert werden können.

-

Risiko des „Festsitzens": Bei unzureichender Umkehr kann sich eine Korrektur bilden, die eine Stopp-Loss-Auslösung verhindert.

-

Relativ große Stop-Loss-Spannen können bei einzelnen verpassten Gelegenheiten zu erheblichen Verlusten führen.

Um diese Risiken zu reduzieren, können folgende Optimierungen vorgenommen werden:

-

Optimierung der Parameter, um Gap Bar und Collecting Bar präziser zu identifizieren.

-

Hinzufügen von Filtern, die eine Position erst nach erneuter Bestätigung der Umkehrkerze eröffnen.

-

Optimierung des Stop-Loss-Algorithmus, um den Stop-Loss näher am Preis zu platzieren und Verluste besser zu kontrollieren.

Optimierungsrichtungen

Die Strategie bietet folgende Optimierungsmöglichkeiten:

-

Hinzufügen eines zusammengesetzten Filters zur Vermeidung von Fehlausbrüchen, z. B. Volumenindikator: Nur bei steigendem Volumen werden Handelssignale berücksichtigt.

-

Integration von gleitenden Durchschnitten (z. B. 20-Tage-Linie, 60-Tage-Linie): Nur bei Durchbruch wichtiger gleitender Durchschnitte werden Signale betrachtet.

-

Multi-Timeframe-Bestätigung: Nur wenn mehrere Zeitrahmen gleichzeitig ein Signal liefern, wird eine Position eröffnet.

-

Optimierung der Take-Profit-Bedingungen: Dynamische Anpassung des Risiko-Ertrags-Verhältnisses basierend auf Marktvolatilität und Risikobereitschaft.

-

Kombination mit einem System zur Beurteilung der Marktrichtung (bullish/bearish): Nur in trendstarken Märkten anwenden.

Diese Optimierungen können die Stabilität und die Gewinnwahrscheinlichkeit der Strategie weiter verbessern.

Zusammenfassung

Die Drei-Vier-Kerzen-Ausbruchs-Umkehrstrategie handelt durch die Identifizierung hochwertiger Trendphasen und Umkehrsignale. Sie zeichnet sich durch kurze Handelsperioden und hohe Frequenz aus, was potenziell hohe Überschussrenditen ermöglicht. Gleichzeitig birgt sie gewisse Risiken, die durch weitere Optimierung reduziert werden müssen. Insgesamt nutzt die Strategie effektiv die inhärenten Merkmale der Kursformation zur Bestimmung von Trends und Umkehrpunkten und verdient weitere Erforschung und Anwendung.

/*backtest

start: 2023-12-10 00:00:00

end: 2023-12-17 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Three (3)-Bar and Four (4)-Bar Plays Strategy", shorttitle="Three (3)-Bar and Four (4)-Bar Plays Strategy", overlay=true, calc_on_every_tick=true, currency=currency.USD, default_qty_value=1.0,initial_capital=30000.00,default_qty_type=strategy.percent_of_equity)

frommonth = input(defval = 1, minval = 01, maxval = 12, title = "From Month")- 1