EMA/ADX/VOL - Asesino de criptomonedas

Estrategia de trading cuantitativa que utiliza el sistema de medias móviles EMA para determinar la dirección de la tendencia, el indicador ADX para medir la fuerza de la tendencia, y un filtro de volumen para las entradas.

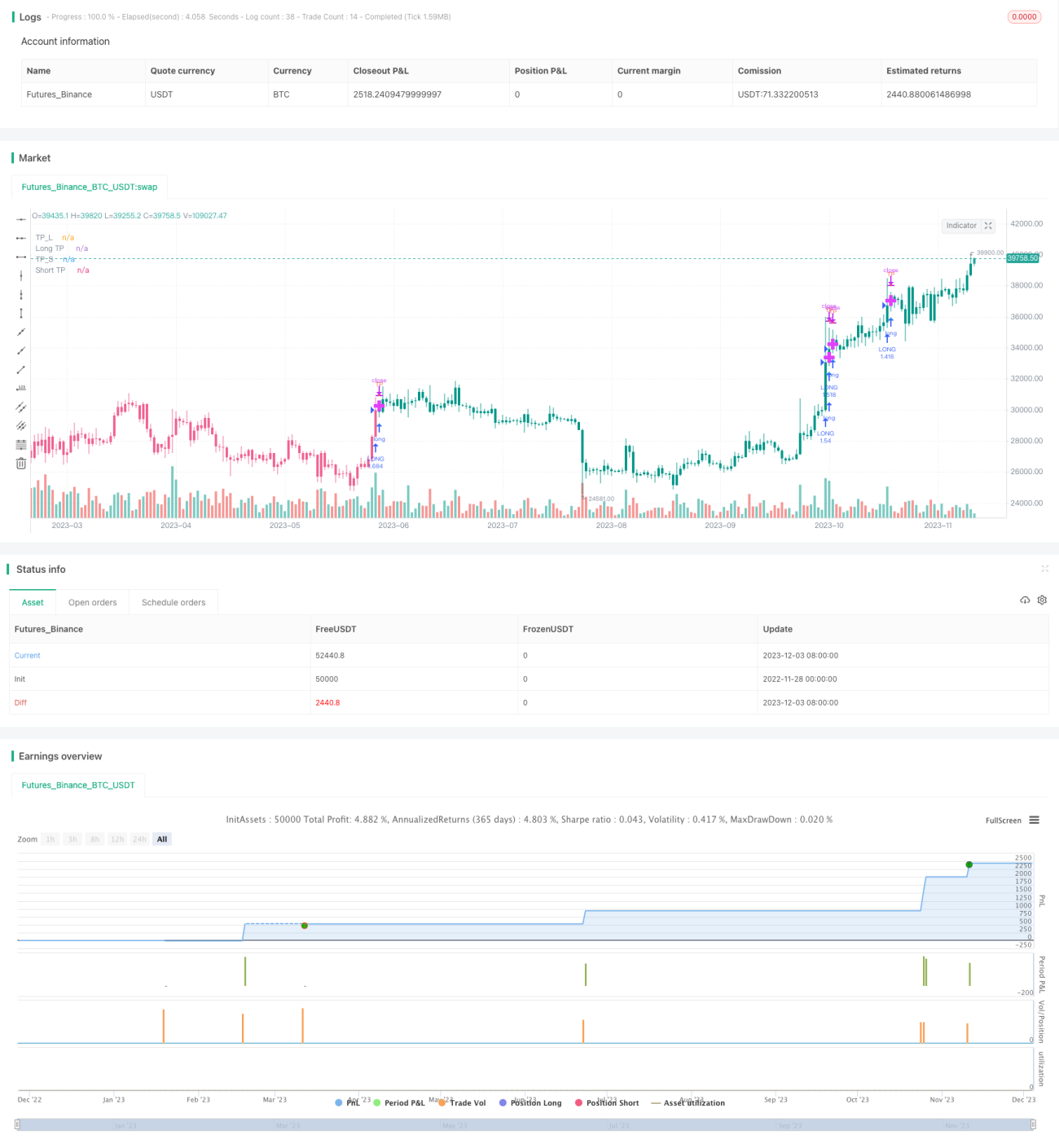

Principio

La estrategia primero utiliza 5 EMA de diferentes períodos para determinar la dirección del precio. Cuando las 5 EMA están todas subiendo, se considera que se ha formado una tendencia alcista; cuando las 5 EMA están todas bajando, se considera que se ha formado una tendencia bajista.

A continuación, se utiliza el indicador ADX para evaluar la fuerza de la tendencia. Cuando la línea DI+ está por encima de la línea DI- y el valor ADX supera un umbral establecido, se considera un mercado alcista fuerte; cuando la línea DI- está por encima de la línea DI+ y el valor ADX supera el umbral, se considera un mercado bajista.

Además, se utiliza una ruptura de volumen como confirmación adicional, requiriendo que el volumen de la vela actual sea mayor que un múltiplo del volumen medio de un cierto período, para evitar entradas erróneas en zonas de bajo volumen.

Combinando la dirección de la tendencia, la fuerza de la tendencia y el volumen, se forma la lógica de apertura de posiciones largas y cortas de la estrategia.

Ventajas

-

El uso del sistema de EMA para determinar la dirección de la tendencia es más fiable que una sola EMA.

-

El indicador ADX ayuda a medir la fuerza de la tendencia, evitando entradas erróneas cuando no hay una tendencia clara.

-

El filtro de volumen garantiza un respaldo suficiente de volumen, aumentando la fiabilidad de la estrategia.

-

La combinación de múltiples condiciones produce señales de entrada más precisas y fiables.

-

La estrategia tiene múltiples parámetros que pueden optimizarse para mejorar continuamente su rendimiento.

Riesgos y soluciones

-

En mercados laterales, las EMA, el ADX y otros indicadores pueden generar señales falsas, provocando pérdidas innecesarias. Se pueden ajustar los parámetros adecuadamente o añadir otros indicadores de apoyo.

-

Si el filtro de volumen es demasiado estricto, se pueden perder oportunidades. Se puede reducir el parámetro del filtro de volumen.

-

La frecuencia de trading puede ser alta, por lo que es necesario gestionar el capital adecuadamente y controlar el tamaño de cada posición.

Direcciones de optimización

-

Probar diferentes combinaciones de parámetros para encontrar los óptimos y mejorar el rendimiento de la estrategia.

-

Añadir otros indicadores como MACD, KDJ, etc., combinándolos con EMA y ADX para formar un criterio de apertura más completo y potente.

-

Incorporar una estrategia de stop loss para controlar aún más el riesgo.

-

Optimizar la gestión del tamaño de las posiciones para lograr una gestión de capital más científica.

Resumen

Esta estrategia considera de forma integral la dirección de la tendencia del precio, la fuerza de la tendencia y el volumen para formar reglas de apertura, evitando en cierta medida trampas comunes y ofreciendo una alta fiabilidad. Sin embargo, aún es necesario perfeccionar el sistema de la estrategia mediante la optimización de parámetros, la selección de indicadores y el control de riesgos para mejorar aún más su eficacia. En general, este marco de estrategia tiene un gran potencial de expansión y espacio de optimización.

- 1