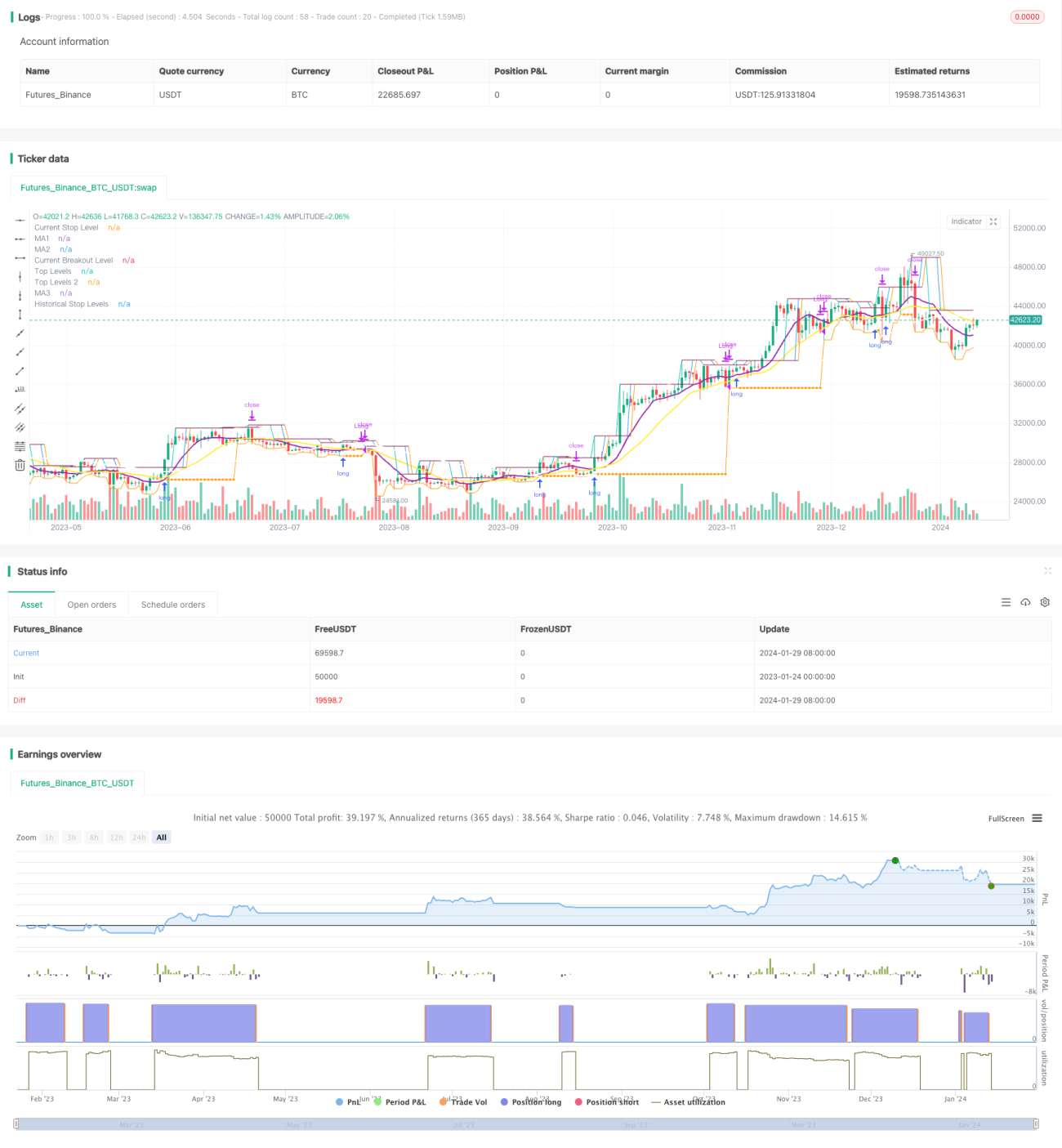

Estrategia de seguimiento de rupturas

Descripción general

La idea principal de esta estrategia es identificar la dirección de la tendencia en un marco de tiempo más grande y encontrar un punto de entrada de ruptura en un marco de tiempo más pequeño, mientras que el stop loss exit sigue la media móvil en un marco de tiempo más grande.

Principio de estrategia

La estrategia se basa principalmente en tres indicadores:

En primer lugar, se calcula un promedio móvil simple de X días de un período más largo (como la línea de sol) y se permite comprar solo cuando el promedio móvil está en la estación de precios. Esto puede usarse para determinar la dirección de la tendencia general y evitar períodos de volatilidad en el comercio.

En segundo lugar, se calcula el máximo precio de un período más corto (por ejemplo, 5 días) Swing High, cuando el precio se rompe el máximo precio se activa la señal de compra. Aquí se combina con una revisión del parámetro de ciclo lb para encontrar el punto de ruptura adecuado.

En tercer lugar, establezca una línea de parada. Una vez en posición, la línea de parada se bloquea en el precio mínimo de un determinado período de lbStop a la distancia del punto más bajo más reciente. Al mismo tiempo, establezca un promedio móvil (como la línea solar 10 días de EMA) como mecanismo de salida, y salga de la posición cuando el precio esté por debajo de ese promedio móvil.

La estrategia también establece un valor de ATR para evitar la compra de puntos exagerados. Además, hay otras condiciones auxiliares como el rango de tiempo de retracción.

La interacción de estos tres indicadores constituye la lógica central de la estrategia.

Análisis de las ventajas estratégicas

Esta es una estrategia de tipo de seguimiento de brecha que tiene las siguientes ventajas:

-

Utiliza dos marcos de tiempo para evitar estar atrapado en falsas rupturas de mercados convulsivos. El marco de tiempo más largo para juzgar la tendencia general, el marco de tiempo más corto para buscar puntos de entrada específicos.

-

Utilizando los puntos de ruptura que se forman en el swing high, este tipo de ruptura tiene cierta inercia y es fácil de seguir. Al mismo tiempo, se puede ajustar el parámetro de revisión del ciclo lb para buscar una ruptura realmente efectiva.

-

El método de stop loss es más riguroso, ya que se rastrea el punto más bajo más reciente y se deja una cierta distancia de amortiguamiento para evitar que se bloquee.

-

El uso de la media móvil como mecanismo de salida permite una suspensión flexible según las circunstancias.

-

El indicador ATR evita los riesgos de una emisión excesiva.

-

Se pueden configurar diferentes combinaciones de parámetros para probar el efecto, con un mayor espacio de optimización.

Análisis de riesgos

La estrategia también tiene ciertos riesgos:

-

Cuando los precios oscilan hacia arriba y hacia abajo cerca de las medias móviles, es fácil ser cambiado de posición de entrada y salida repetidamente. En este caso, se enfrenta al riesgo de comisiones más altas.

-

Cuando se rompe el punto de compra cerca de la media móvil, existe un mayor riesgo de retiro. Esto es una característica de la estrategia misma.

-

Cuando no hay una tendencia evidente, el tiempo de mantenimiento de la posición puede ser demasiado largo y se enfrenta a un riesgo de tiempo.

-

Es necesario ajustar razonablemente los parámetros de ATR. Si el ATR es demasiado pequeño, el filtro es más débil, y si es demasiado grande, la oportunidad de entrada es menor.

-

Se necesita probar el efecto de los diferentes parámetros lb en los resultados. Parámetros demasiado grandes pueden perder algunas oportunidades, y los parámetros demasiado pequeños pueden identificar falsos avances.

La solución al riesgo:

- Ajuste adecuado de los parámetros de las medias móviles para aumentar el efecto de filtración.

- Optimización de los parámetros de ATR, además de la observación visual.

- Ajuste de vuelta el ciclo lb para encontrar el parámetro óptimo.

- Suspensión de las operaciones en caso de crisis.

Dirección de optimización de la estrategia

La estrategia también se puede optimizar en las siguientes dimensiones:

-

Prueba diferentes combinaciones de parámetros de la media móvil para encontrar el parámetro óptimo.

-

Prueba diferentes configuraciones de parámetros ATR para equilibrar las oportunidades de ingreso y el control de riesgos.

-

Optimización de los parámetros de retrospectiva del ciclo lb para identificar brechas más eficientes.

-

Intentar establecer un stop loss dinámico para controlar el riesgo en función de la volatilidad y el retiro.

-

La efectividad de la brecha se determina en combinación con otros factores, como el indicador de volumen de transacciones.

-

Desarrollar métodos de búsqueda de puntos extremos como referencia, como por ejemplo </',</,><

-

Intentar entrenar a los parámetros con el aprendizaje automático para obtener el parámetro óptimo

Resumir

La estrategia en su conjunto es una estrategia de seguimiento de brecha típica. El juicio de doble marco de tiempo, el Swing High identifica el momento de entrada, la línea de parada y el mecanismo de salida de doble seguro de la media móvil, formando un sistema lógico completo. La estrategia tiene características de riesgo y ganancia más claras y es adecuada para el tipo de inversor que sigue la línea media y larga. Aunque existe un cierto riesgo, se puede reducir el nivel de riesgo mediante la optimización de parámetros y la optimización de reglas.

/*backtest

start: 2023-01-24 00:00:00

end: 2024-01-30 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1