Strategi Breakout dan Reversal Tiga-Empat Candlestick

Ringkasan

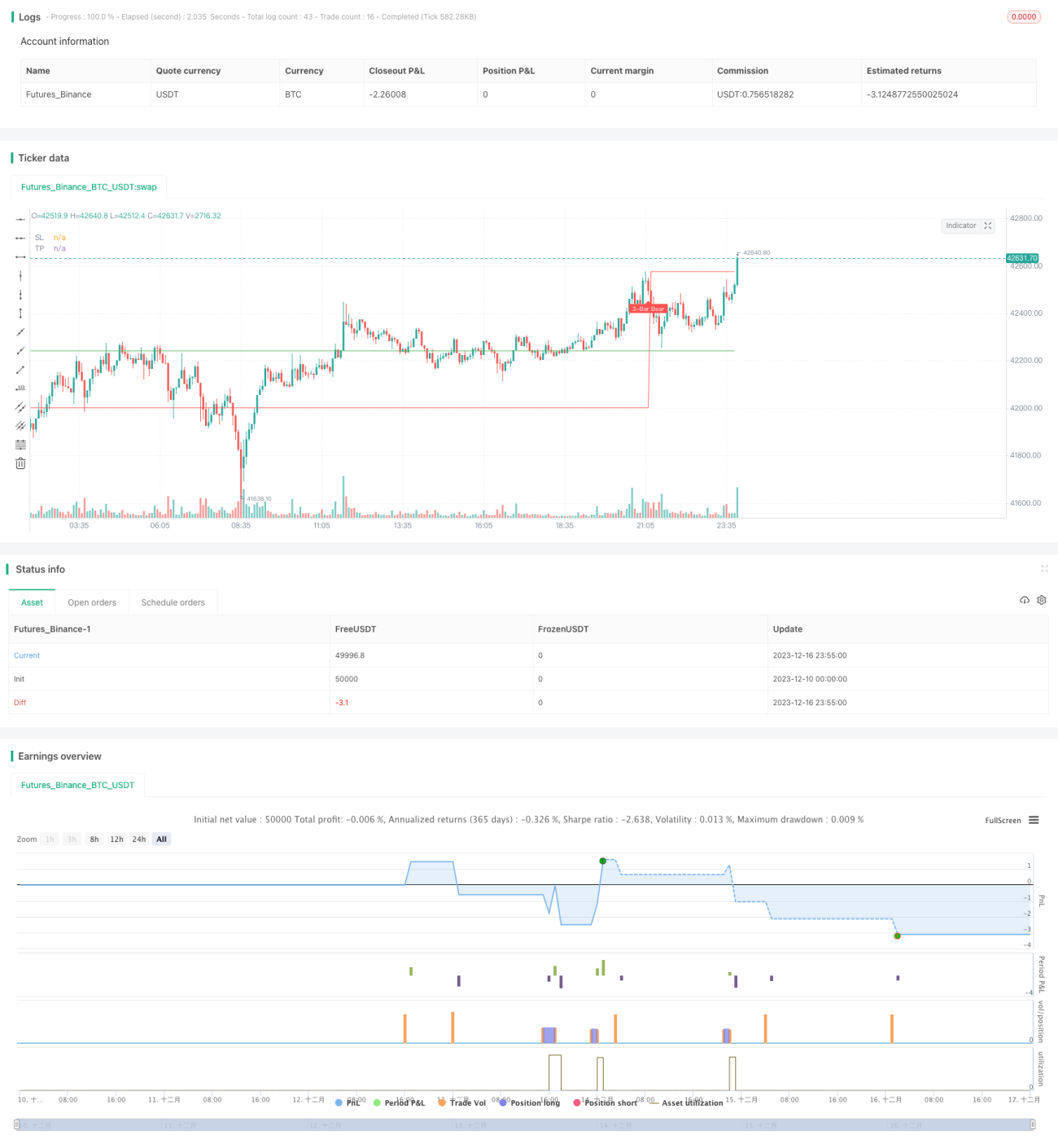

Strategi Pembalikan Tembusan Tiga Empat K-Line mengidentifikasi tiga atau empat K-line dengan momentum kenaikan yang signifikan, kemudian setelah beberapa K-line berikutnya dengan rentang kecil membentuk support atau resistance, strategi ini melakukan trading kontrarian saat K-line pembalikan terjadi. Ini termasuk dalam strategi trading kontrarian.

Prinsip Strategi

Logika identifikasi inti strategi ini terutama terdiri dari beberapa bagian berikut:

-

Identifikasi K-line dengan rentang melebar (Gap Bar): Menembus 1,5 kali rata-rata ATR, bagian badan (real body) lebih besar dari 0,65. K-line ini dianggap memiliki momentum kenaikan atau penurunan yang kuat.

-

Identifikasi K-line konsolidasi dengan volume rendah (Collecting Bar): 1-2 K-line dengan fluktuasi kecil yang mengikuti Gap Bar, di mana titik tertinggi atau terendah mendekati Gap Bar. K-line ini mewakili perlambatan tren dan konsolidasi, membentuk support atau resistance.

-

Identifikasi K-line sinyal pembalikan: Setelah K-line konsolidasi, jika muncul K-line yang badannya menembus titik tertinggi atau terendah dari beberapa K-line sebelumnya, maka itu dapat dianggap sebagai sinyal pembalikan. Berdasarkan arah badan, tentukan apakah posisi long atau short, dan buka posisi pada K-line tersebut.

-

Stop loss dan take profit: Stop loss ditempatkan di bawah titik terendah Gap K-line atau di atas titik tertingginya; take profit didasarkan pada stop loss dikalikan dengan rasio untung-rugi yang dikonfigurasi.

Analisis Keunggulan

Strategi ini memiliki beberapa keunggulan utama berikut:

-

Menggunakan karakteristik K-line itu sendiri untuk menilai tren dan titik pembalikan, tanpa bergantung pada indikator apa pun, sehingga mencapai "indikator bawaan".

-

Kondisi penyaringan Gap Bar dan Collecting Bar ketat, sehingga dapat secara efektif mengidentifikasi tren dan konsolidasi yang sebenarnya.

-

Penilaian sinyal pembalikan didasarkan pada badan K-line, mengurangi kemungkinan sinyal palsu.

-

Hanya membutuhkan kombinasi 3-4 K-line untuk menyelesaikan satu transaksi, dengan periode waktu pendek dan frekuensi tinggi.

-

Pengaturan stop loss dan take profit jelas, sehingga drawdown dan rasio untung-rugi mudah dikendalikan.

Analisis Risiko

Strategi ini juga memiliki beberapa risiko berikut:

-

Bergantung pada kualitas pengaturan parameter. Jika parameter terlalu longgar, akan meningkatkan peluang sinyal palsu dan transaksi merugi.

-

Rentan terhadap gangguan tembusan palsu frekuensi tinggi, sehingga tidak dapat menyaring semua sinyal palsu secara efektif.

-

Ada risiko terjebak (terkunci). Jika pembalikan tidak cukup, dapat membentuk penyesuaian sehingga tidak dapat melakukan stop loss.

-

Rentang stop loss relatif besar, beberapa peluang terjebak dapat menyebabkan kerugian besar.

Untuk mengurangi risiko ini, optimalisasi dapat dilakukan dari beberapa aspek berikut:

-

Optimalkan parameter agar identifikasi Gap Bar dan Collecting Bar lebih akurat.

-

Tambahkan filter, baru buka posisi setelah konfirmasi ulang K-line pembalikan.

-

Optimalkan algoritma stop loss agar lebih mendekati harga, sehingga kerugian lebih terkendali.

Arah Optimalisasi

Strategi ini juga memiliki beberapa arah optimalisasi utama berikut:

-

Tambahkan filter komposit untuk menghindari gangguan tembusan palsu. Misalnya, tambahkan indikator volume, hanya pertimbangkan sinyal trading saat volume meningkat.

-

Kombinasikan dengan indikator moving average, hanya pertimbangkan sinyal trading saat harga menembus moving average penting (misalnya garis 20 hari, garis 60 hari).

-

Verifikasi multi-kerangka waktu, hanya buka posisi saat beberapa siklus memberikan sinyal secara bersamaan.

-

Optimalkan kondisi take profit, sesuaikan rasio untung-rugi secara dinamis berdasarkan tingkat volatilitas pasar dan preferensi risiko.

-

Kombinasikan dengan sistem penilaian kondisi pasar bullish/bearish, hanya gunakan strategi ini di lingkungan pasar yang cenderung tren.

Optimalisasi ini dapat lebih meningkatkan stabilitas dan probabilitas keuntungan strategi.

Kesimpulan

Strategi Pembalikan Tembusan Tiga Empat K-line melakukan trading dengan mengidentifikasi segmen potensi tren berkualitas tinggi dan sinyal pembalikan. Siklus operasi pendek, frekuensi tinggi, berpotensi memperoleh keuntungan berlebih yang besar. Namun, juga memiliki risiko tertentu, perlu terus dioptimalkan untuk mengurangi risiko dan meningkatkan stabilitas. Secara keseluruhan, strategi ini secara efektif memanfaatkan karakteristik kerangka pergerakan harga itu sendiri untuk menilai tren dan titik pembalikan, layak untuk penelitian dan aplikasi lebih lanjut.

/*backtest

start: 2023-12-10 00:00:00

end: 2023-12-17 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Three (3)-Bar and Four (4)-Bar Plays Strategy", shorttitle="Three (3)-Bar and Four (4)-Bar Plays Strategy", overlay=true, calc_on_every_tick=true, currency=currency.USD, default_qty_value=1.0,initial_capital=30000.00,default_qty_type=strategy.percent_of_equity)

frommonth = input(defval = 1, minval = 01, maxval = 12, title = "From Month")- 1