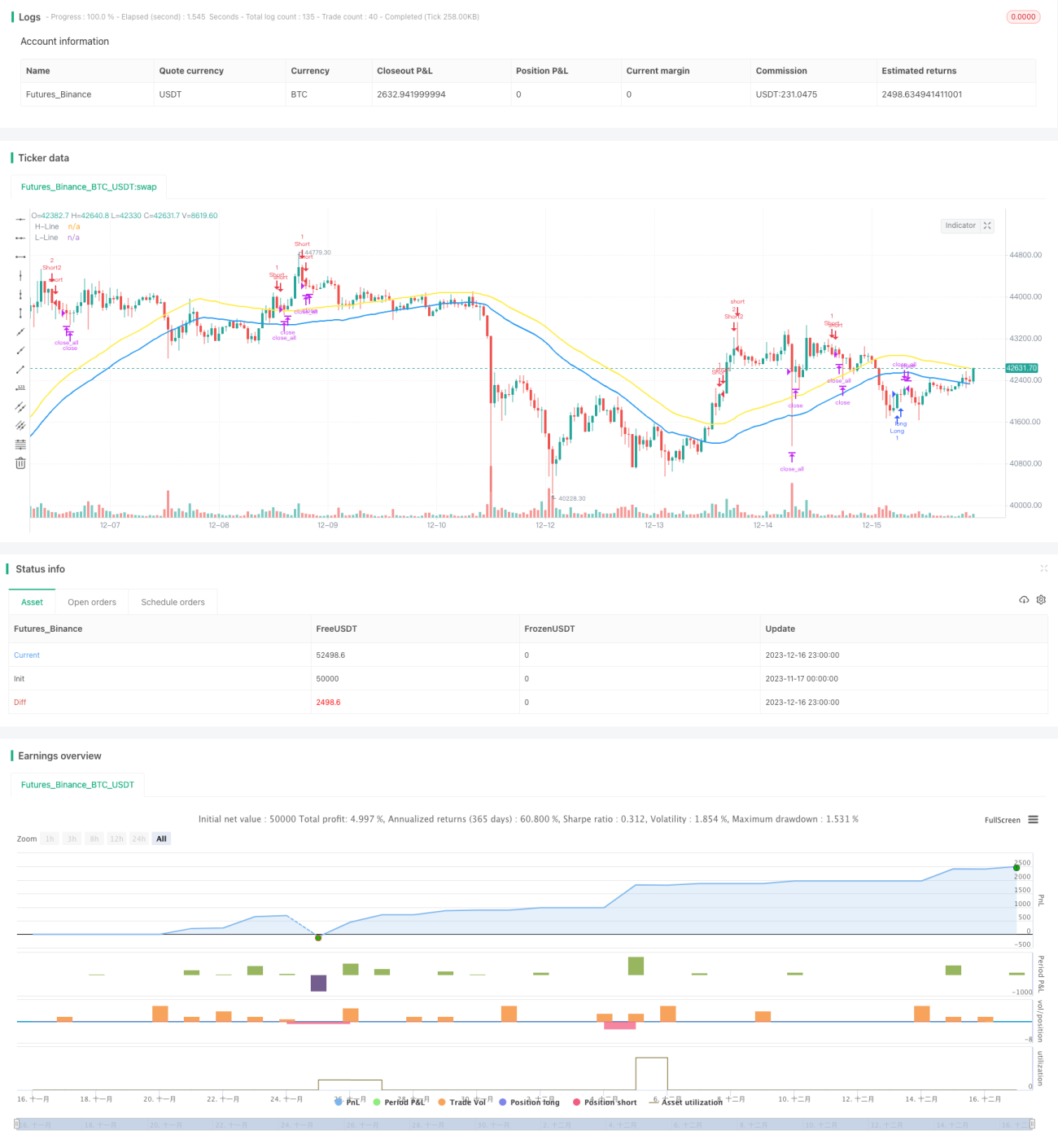

Strategi Pengikut Tren dengan Kombinasi Stochastic yang Dimodifikasi dan Ditingkatkan pada Multi-Kerangka Waktu dan SMA

Ringkasan

Strategi ini menggabungkan indikator Stochastic klasik dengan indikator SMA untuk menghasilkan kemampuan pelacakan tren yang kuat. Ide inti strategi adalah menggunakan indikator Stochastic untuk mengidentifikasi sinyal arah tren, dikombinasikan dengan indikator SMA sebagai filter untuk meningkatkan kualitas sinyal, serta menetapkan parameter indikator berdasarkan mode risiko yang berbeda guna mewujudkan penyesuaian dinamis antara risiko dan imbal hasil. Selain itu, strategi juga memanfaatkan penilaian multi-kerangka waktu untuk mengoptimalkan pemilihan waktu masuk pasar.

Prinsip Strategi

- Strategi menggunakan indikator Stochastic yang dimodifikasi dan ditingkatkan, dengan parameter indikator meliputi periode %K, periode smoothing %K, dan periode smoothing %D. Sensitivitas indikator dikendalikan melalui pengaturan parameter.

- Parameter indikator SMA meliputi SMA titik tertinggi dan SMA titik terendah, digunakan untuk menyaring sinyal, meningkatkan kualitas sinyal, dan menghindari false breakout.

- Berdasarkan preferensi risiko yang berbeda, strategi menyediakan pilihan mode risiko rendah, mode risiko sedang, dan mode risiko tinggi. Mode risiko akan memengaruhi parameter persilangan indikator Stochastic, sehingga mewujudkan penyesuaian dinamis antara risiko dan imbal hasil.

- Strategi menentukan sinyal posisi beli (long) ketika indikator Stochastic melintasi ke atas dari ambang batas dan harga penutupan di bawah SMA titik terendah; sinyal posisi jual (short) ketika indikator Stochastic melintasi ke bawah dari ambang batas dan harga penutupan di atas SMA titik tertinggi.

- Strategi memperkenalkan modul penilaian multi-kerangka waktu untuk memverifikasi sinyal dalam rentang waktu yang berbeda, memilih waktu masuk yang lebih optimal guna mengendalikan risiko perdagangan.

Keunggulan Strategi

- Menggunakan indikator Stochastic versi modifikasi yang ditingkatkan, meningkatkan sensitivitas indikator sehingga mampu menangkap perubahan pasar dengan cepat.

- Menambahkan mekanisme penyaringan ganda SMA, yang secara efektif dapat menyaring sinyal palsu dan meningkatkan kualitas sinyal.

- Menyediakan berbagai mode risiko untuk dipilih, pengguna dapat menyesuaikan parameter secara fleksibel sesuai preferensi risiko masing-masing.

- Menambahkan modul penilaian multi-kerangka waktu, mengoptimalkan pemilihan waktu masuk pasar, mengurangi risiko perdagangan.

- Pengaturan parameter strategi yang wajar, penggunaan indikator yang alami, kerangka kerja keseluruhan yang ilmiah dan ketat, stabilitas baik, dan adaptasi yang kuat.

Risiko Strategi

- Strategi itu sendiri tidak memiliki mekanisme stop loss, sehingga perlu mengatur level stop loss secara manual untuk mengendalikan risiko kerugian.

- Sinyal strategi yang sering dapat menyebabkan overtrading dan meningkatkan biaya perdagangan.

- Strategi cukup sensitif terhadap pengaturan parameter dan mode risiko, sehingga perlu diuji dan dioptimalkan untuk menemukan parameter terbaik.

- Drawdown strategi mungkin cukup besar, tidak cocok untuk operasi full position, sehingga perlu mengendalikan ukuran modal perdagangan.

Metode penanganan:

- Tetapkan rasio stop loss yang wajar berdasarkan tingkat volatilitas pasar untuk meminimalkan kerugian.

- Sesuaikan parameter indikator Stochastic dengan tepat untuk mengurangi frekuensi sinyal. Atau tetapkan take profit minimal untuk mengurangi perdagangan yang tidak perlu.

- Disarankan untuk memilih mode risiko rendah default, lalu sesuaikan parameter lain berdasarkan data backtest.

- Kendalikan ukuran posisi, bangun posisi secara bertahap untuk mengurangi risiko per transaksi.

Arah Optimasi Strategi

- Lakukan pengujian menyeluruh terhadap parameter indikator Stochastic dan SMA untuk menemukan kombinasi parameter yang optimal.

- Tingkatkan jumlah kerangka waktu dalam penilaian multi-kerangka, perkaya dasar penilaian, optimalkan pemilihan waktu masuk pasar.

- Perkenalkan kombinasi indikator stop loss seperti ATR stop loss, yang dapat melacak level stop loss secara dinamis untuk mengurangi risiko.

- Bangun mekanisme penyaringan dan konfirmasi sinyal indikator, misalnya menambahkan indikator volume untuk menilai, guna menghindari jebakan pasar.

- Tambahkan modul manajemen posisi, yang secara aktif menyesuaikan posisi berdasarkan kondisi pasar, untuk mengurangi risiko per transaksi.

Kesimpulan

Strategi ini secara komprehensif memanfaatkan keunggulan indikator Stochastic dan SMA, menghasilkan efek pelacakan tren yang kuat. Kerangka strategi yang wajar, penggunaan indikator yang alami, melalui pengaturan parameter dan mode risiko mengembalikan esensi indikator, mengoptimalkan stabilitas strategi. Modul penilaian multi-kerangka waktu juga meningkatkan adaptasi strategi, memungkinkan penyesuaian berdasarkan berbagai instrumen dan periode. Secara keseluruhan, strategi ini memiliki generalisasi yang baik, sekaligus memiliki ruang optimasi yang besar, layak untuk diteliti lebih lanjut.

- 1