Strategi Mengikuti Terobosan

Ringkasan

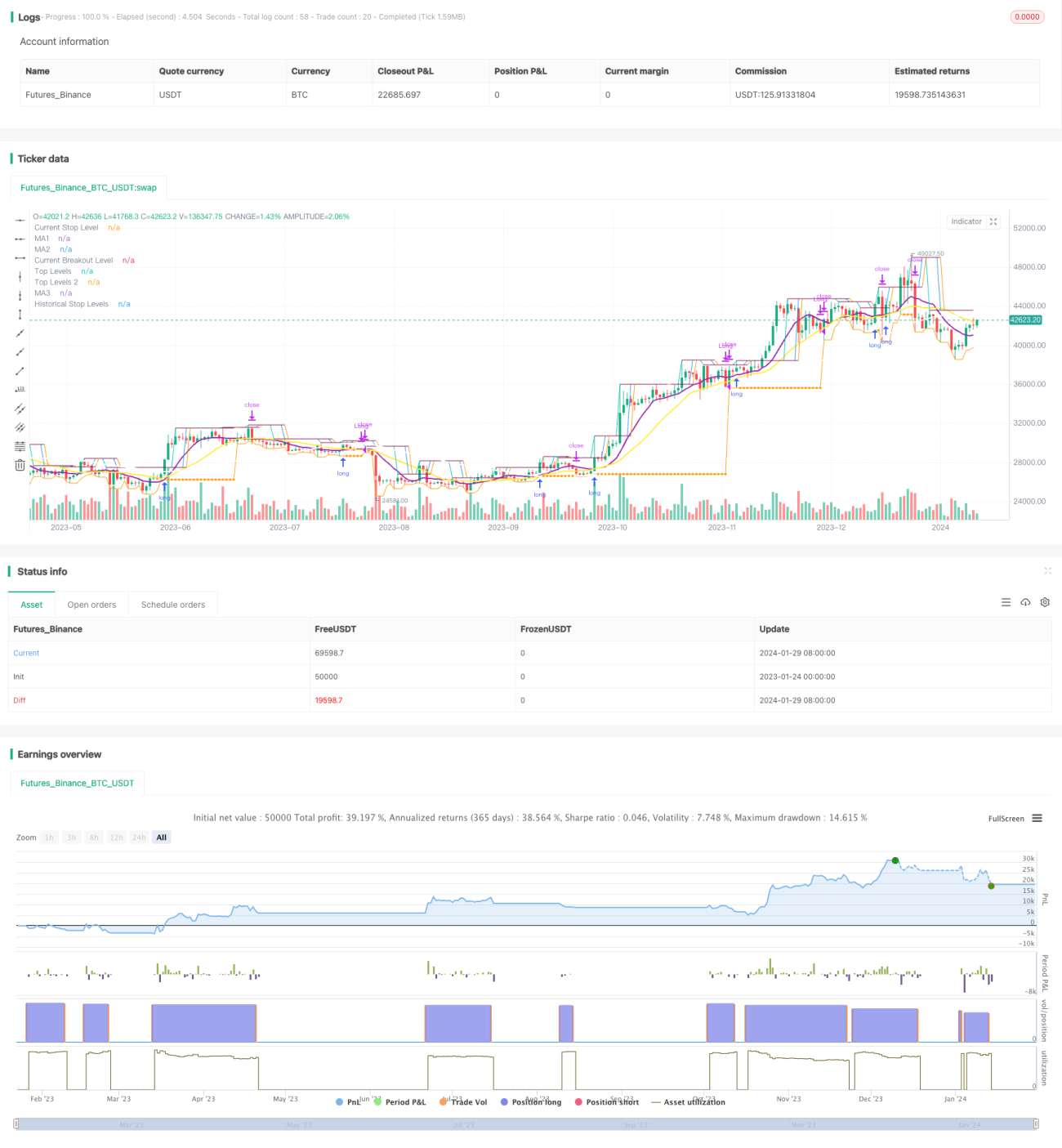

Gagasan utama dari strategi ini adalah untuk mengidentifikasi arah tren pada jangka waktu yang lebih besar dan menemukan titik masuk terobosan pada jangka waktu yang lebih kecil, sementara stop loss exit melacak rata-rata bergerak pada jangka waktu yang lebih besar.

Prinsip Strategi

Strategi ini didasarkan pada tiga indikator utama:

Pertama, menghitung rata-rata bergerak sederhana X hari untuk periode yang lebih panjang (seperti garis matahari), dan hanya mengizinkan pembelian saat rata-rata bergerak tersebut berada di posisi harga. Ini dapat digunakan untuk mengetahui arah tren keseluruhan dan menghindari periode getaran perdagangan.

Kedua, menghitung harga tertinggi dalam periode yang lebih pendek (misalnya 5 hari) Swing High, yang memicu sinyal beli ketika harga melampaui harga tertinggi tersebut. Di sini digabungkan dengan parameter siklus lb untuk mencari titik penembusan yang sesuai.

Ketiga, membuat stop loss line. Setelah memasuki posisi, stop loss line terkunci pada harga terendah untuk periode tertentu lbStop dari titik terendah terdekat. Pada saat yang sama, mengatur moving average (seperti 10-hari EMA) sebagai mekanisme keluar, dan keluar dari posisi ketika harga lebih rendah dari moving average.

Strategi ini juga menetapkan nilai ATR untuk menghindari pembelian poin yang terlalu besar. Selain itu, ada kondisi tambahan lainnya seperti rentang waktu pengukuran.

Pertimbangan dari interaksi antara ketiga indikator tersebut membentuk logika inti dari strategi tersebut.

Analisis Keunggulan Strategi

Ini adalah strategi tracking yang inovatif, dengan beberapa keuntungan:

-

Gunakan dua frame waktu untuk menghindari terjerat dalam pasar yang bergoyang. Frame waktu yang lebih panjang untuk menilai tren keseluruhan, dan frame waktu yang lebih pendek untuk mencari titik masuk tertentu.

-

Terobosan ini memiliki inersia tertentu dan mudah untuk dilacak. Pada saat yang sama, melihat kembali parameter lb dapat disesuaikan untuk menemukan terobosan yang benar-benar efektif.

-

Stop loss lebih ketat, melacak titik terendah terbaru dan meninggalkan jarak penyangga untuk menghindari penarikan.

-

Menggunakan Moving Average sebagai mekanisme exit, stop-loss dapat dilakukan secara fleksibel sesuai situasi.

-

Indikator ATR menghindari risiko yang ditimbulkan oleh pelepasan berlebihan.

-

Anda dapat mengatur kombinasi parameter yang berbeda untuk menguji efek, ruang yang lebih besar untuk optimasi.

Analisis risiko

Strategi ini juga memiliki beberapa risiko:

-

Ketika harga bergejolak di sekitar Moving Average, maka Anda akan sering bertukar posisi masuk dan keluar. Anda akan menghadapi risiko biaya yang lebih tinggi.

-

Jika Anda melakukan breakout di dekat Moving Average, Anda akan menghadapi risiko penarikan yang lebih besar. Ini adalah karakteristik strategi itu sendiri.

-

Ketika tidak ada tren yang jelas, jangka waktu yang terlalu lama dapat menyebabkan risiko waktu.

-

Parameter ATR harus diatur secara wajar. ATR terlalu kecil akan mengurangi efek penyaringan, dan terlalu besar akan mengurangi peluang masuk.

-

Perlu untuk menguji dampak dari parameter lb yang berbeda pada hasil. Parameter yang terlalu besar akan kehilangan beberapa peluang, parameter yang terlalu kecil dapat mengidentifikasi terobosan palsu.

Solusi untuk Mengatasi Risiko:

- Penyesuaian parameter rata-rata bergerak untuk meningkatkan efek filter.

- Optimalkan parameter ATR dan pertimbangan visual.

- Perbaiki kembali siklus lb untuk mencari parameter optimal.

- "Kami tidak akan melakukan apa-apa", kata dia.

Arah optimasi strategi

Strategi ini juga dapat dioptimalkan dari dimensi-dimensi berikut:

-

Uji berbagai kombinasi parameter moving average untuk mencari parameter optimal.

-

Cobalah pengaturan parameter ATR yang berbeda untuk menyeimbangkan peluang masuk dan kontrol risiko.

-

Optimalkan kembali parameter siklus lb untuk mengidentifikasi terobosan yang lebih efisien.

-

Cobalah untuk membangun stop loss dinamis, dengan risiko kontrol berdasarkan volatilitas dan penarikan.

-

Efektivitas terobosan ini dinilai dengan faktor-faktor lain seperti volume transaksi.

-

Mengembangkan metode untuk mencari titik ekstrim sebagai referensi.

-

Cobalah Machine Learning untuk melatih parameter untuk mendapatkan parameter yang optimal

Meringkaskan

Strategi ini secara keseluruhan adalah strategi pelacakan terobosan yang khas. Pertimbangan kerangka waktu ganda, Swing High mengidentifikasi waktu masuk, stop loss, dan mekanisme keluar dari moving average, membentuk sistem logis yang lengkap. Strategi ini memiliki karakteristik risiko dan keuntungan yang lebih jelas, cocok untuk investor dengan jenis pelacakan garis panjang dan menengah.

/*backtest

start: 2023-01-24 00:00:00

end: 2024-01-30 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1