トレンド追跡反転とエーラーズ先行指標連合戦略

概要

本戦略は、トレンドフォロー反転戦略とエーラーズ先行指標戦略を組み合わせたもので、より信頼性の高い取引シグナルを得ることを目的としています。トレンドフォロー反転戦略はトレンドの反転ポイントを判断し、エーラーズ先行指標戦略は周期的な転換点を判断します。組み合わせたシグナルにより、エントリータイミングをより正確に判断できます。

戦略の原理

トレンドフォロー反転戦略

この戦略は、Ulf Jensen著『How I Tripled My Money in the Futures Market』の183ページに由来します。これは反転タイプの戦略です。終値が2日連続で前日の終値より高く、かつ9日ストキャスティクスの低速線が50未満の場合に買いシグナルとなります。終値が2日連続で前日の終値より低く、かつ9日ストキャスティクスの高速線が50超の場合に売りシグナルとなります。

エーラーズ先行指標戦略

この戦略は日内データを使用し、1日のデトレンド合成価格(Detrended Synthetic Price、DSP)および日内エーラーズ先行指標(Ehlers Leading Indicator、ELI)を描画します。DSPは価格の支配的な周期を捉えることができ、2次バターワースフィルターから3次フィルターを差し引いて計算します。ELIは周期の転換点を事前に示すことができ、デトレンド合成価格からその単純移動平均を差し引いて計算します。ELIがデトレンド合成価格を超えたときに売買シグナルが発生します。

優位性分析

この組み合わせ戦略の最大の利点は、トレンド反転の判断と周期的な転換点の判断を組み合わせることで、取引シグナルがより信頼できる点です。トレンドフォロー反転戦略は、上下のバンドをブレイクするトレンド反転ポイントを判断できます。また、エーラーズ先行指標は周期的な谷や山を事前に示すことができます。両者を組み合わせることで、エントリータイミングをより正確に捉えることができます。

もう一つの利点は、パラメータ調整の柔軟性です。トレンドフォロー反転戦略のストキャスティクスパラメータは市場に応じて調整可能であり、エーラーズ先行指標の周期長も異なる周期に適応するよう調整できます。

リスク分析

この戦略の最大のリスクは、トレンドの継続を見逃すことです。戦略は反転シグナルが現れるのを待ってからエントリーするため、初期の強いトレンド局面を逃す可能性があります。また、反転シグナルが偽のブレイクアウトである可能性があり、ポジションが逆方向に動くリスクもあります。

対策としては、パラメータを調整し、反転判断の期間を短縮してトレンド反転を迅速に捉えることです。また、ストップロスを導入して損失を抑えることも有効です。

最適化の方向性

本戦略は以下の点で最適化が可能です。

- ストップロス戦略を導入し、1回の損失を抑える。

- パラメータを最適化し、反転シグナルの期間を調整して異なる市場環境に対応する。

- 他の指標によるフィルターを追加し、シグナルの質を高め、偽シグナルを減らす。

- 資金管理モジュールを追加し、全体のポジションサイズとリスクを管理する。

- 異なる銘柄でのパラメータ効果をテストし、どの銘柄に最適かを判断する。

- 機械学習モジュールを導入し、パラメータが適応的に調整されるようにする。

まとめ

本戦略は、トレンド反転の判断と周期的な転換点の判断を組み合わせることで、エントリータイミングをより確実に捉えることができます。最大の利点はシグナルの質が高く、調整の柔軟性が高い点です。最大のリスクは初期のトレンドを見逃す可能性であり、パラメータ調整やストップロスによって管理できます。今後はストップロス、パラメータ最適化、シグナルフィルターなどの改良により、戦略をさまざまな市場環境に適応させることが可能です。

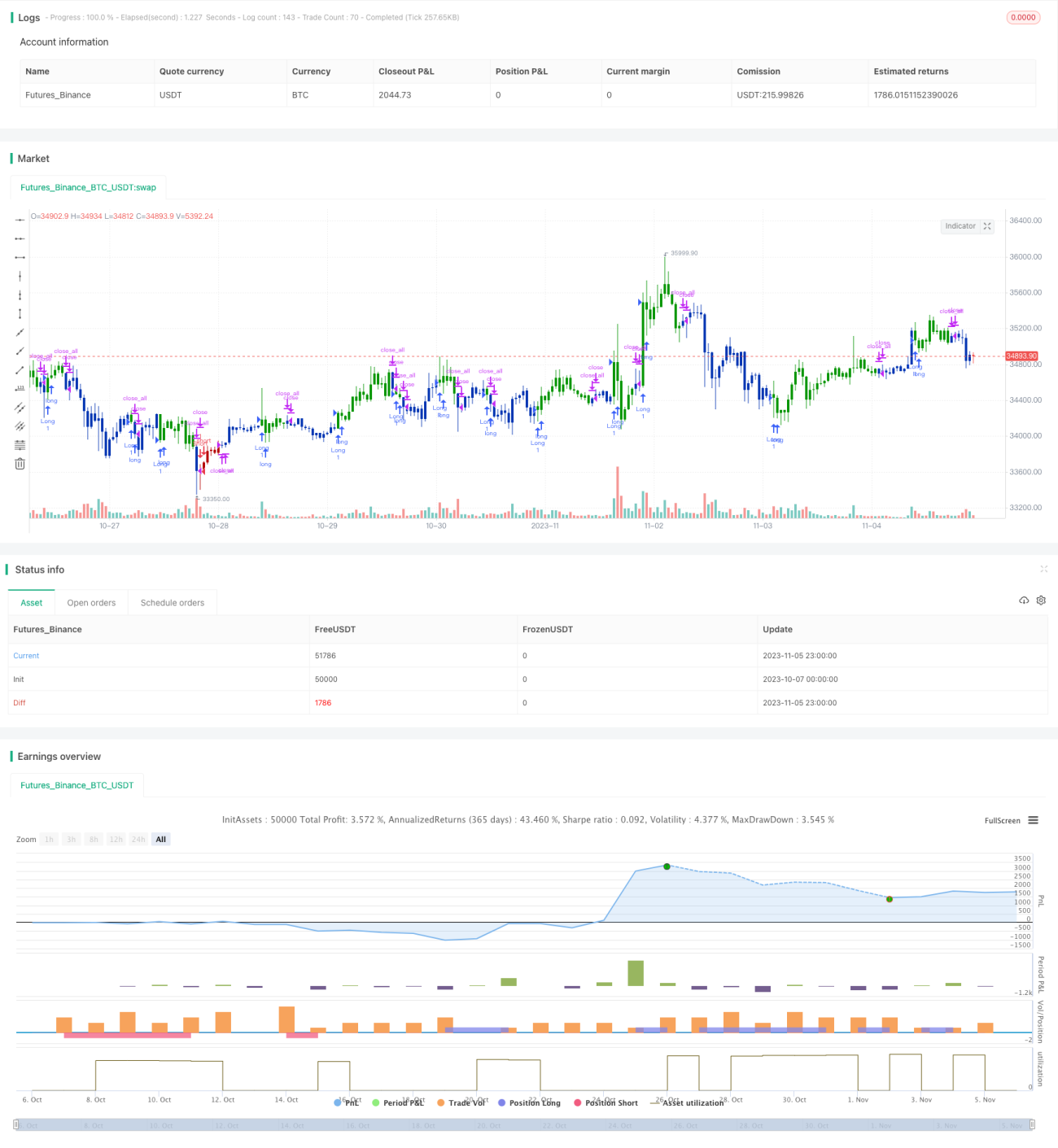

/*backtest

start: 2023-10-07 00:00:00

end: 2023-11-06 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 26/11/2019

// This is combo strategies for get a cumulative signal. - 1