VWMAおよびATRに基づくトレンドフォロー戦略

概要

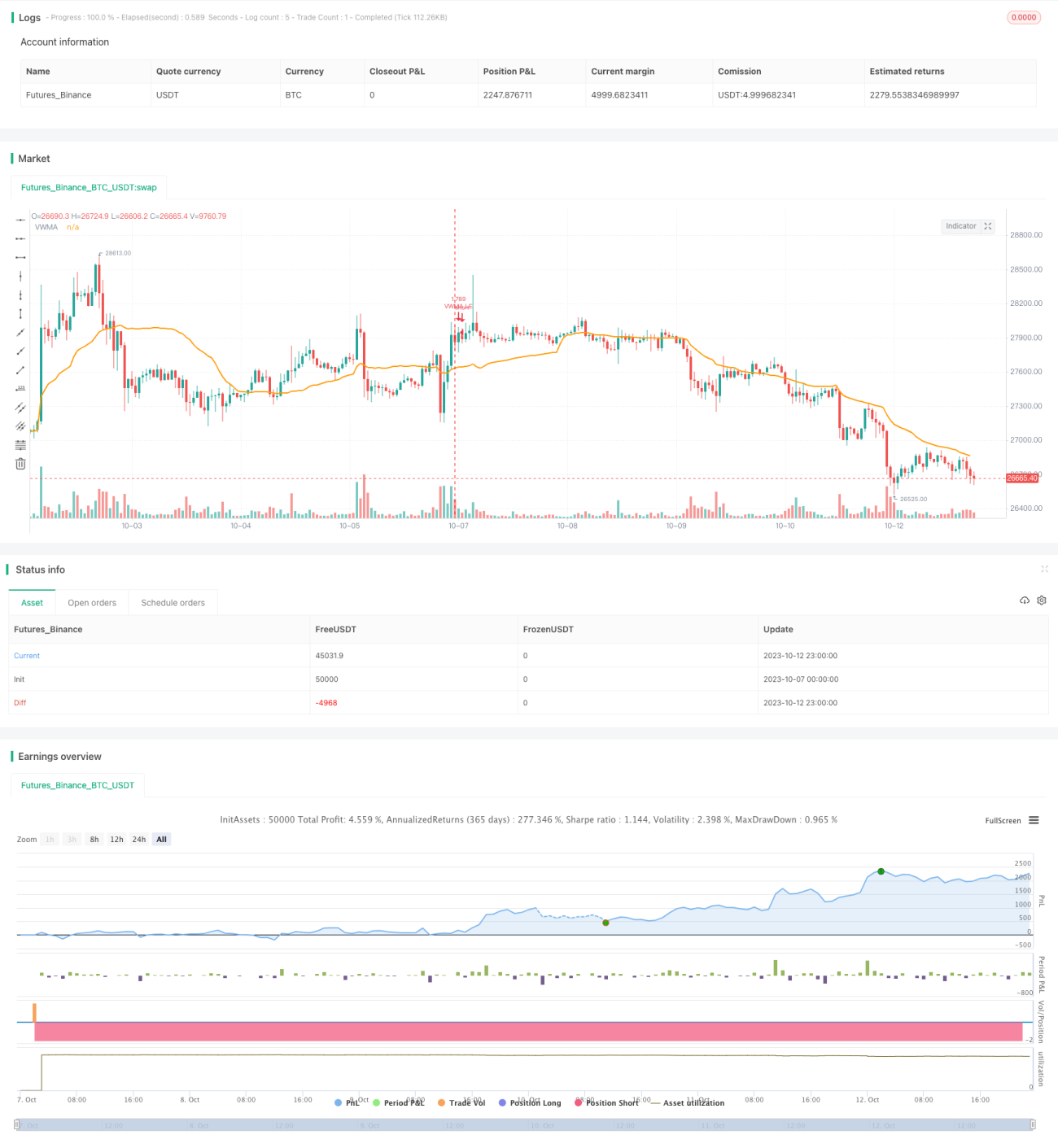

本戦略は、VWMA(出来高加重移動平均)インジケーターを使用してトレンド方向を判断し、ATR(平均真の範囲)インジケーターでストップロスラインを設定することでトレンドフォローを実現します。本戦略は、明確なトレンドが見られる市場環境に適しています。

戦略の原理

-

VWMAを使用してトレンド方向を判断します。価格がVWMAを上回っている場合は上昇トレンドと判断してロング、価格がVWMAを下回っている場合は下降トレンドと判断してショートを行います。

-

偽のブレイクアウトをフィルタリングするために、RSIオシレーターを追加します。RSIが30を上回っている場合のみロングシグナルを発します。

-

ATRを使用してストップロスラインを計算します。ATRの期間はVWMAと同じに設定し、倍率は3.5とします。ストップロスラインは価格に応じてリアルタイムで更新されます。

-

ATR倍率の設定はストップロスラインの収縮幅に影響を与えます。倍率が大きいほどストップロスラインの更新頻度が低くなり、トレンドフォロー効果が高まります。

-

戦略内のストップロスパーセンテージと口座残高に基づいてポジションサイズを計算します。

-

価格がストップロスラインを下回った場合、ロングポジションをストップロス決済します。

戦略の利点

-

VWMAを使用してトレンド方向を判断することで、トレンドの機会を継続的に捉えることができます。

-

RSIフィルターを追加することで、一部の偽ブレイクアウトシグナルを排除できます。

-

ATRによるストップロスラインでトレンドフォローを実現し、逆方向へのストップロスを回避できます。

-

口座残高とストップロスパーセンテージに基づいてポジションサイズを計算するため、リスク管理に有効です。

戦略のリスク

-

トレンド転換点では損失リスクが存在します。ポジションサイズを適切に縮小し、1回あたりの損失額を低減すべきです。

-

ATRパラメーターの設定が不適切だと、ストップロスラインが過敏または鈍感になる可能性があります。適切なパラメーターをテストで決定する必要があります。

-

トレンドが急激に反転した場合、ストップロスラインの更新が間に合わず、損失が拡大する恐れがあります。

-

低ボラティリティ市場では、ポジションサイズを減らし、ストップロスラインの更新頻度を高めるべきです。

最適化の方向性

-

異なるVWMAパラメーターの組み合わせをテストし、最適なシグナルを生成するパラメーターを選択できます。

-

RSIオシレーターの他のパラメーター設定(例:買われすぎ・売られすぎラインなど)をテストできます。

-

ATRの倍率パラメーターをテストし、ドローダウンとトレンドフォローのトレードオフを最適化するポイントを見つけられます。

-

MACDやKDなどの他のインジケーターと組み合わせてシグナルをフィルタリングし、シグナル品質を向上させることができます。

-

市場のボラティリティに応じてポジション管理とストップロスパーセンテージを最適化できます。

まとめ

本戦略は全体的にトレンド指向であり、明確な価格トレンドを捉えるのに適しています。トレンド判断、シグナルフィルタリング、ストップロスフォローなどの利点がある一方、トレンド反転リスクも存在します。パラメーター設定とポジション管理を最適化することで、より良い戦略効果を得ることができます。

- 1