1

Follow

1802

Followers

概要

双陰線反転戦略は、ローソク足の形状に基づく短期取引戦略です。この戦略では、連続する2本のローソク足に影(ヒゲ)がない特殊なローソク足パターンを識別し、反転の可能性を判断します。戦略の利点はシンプルでわかりやすく、実装が容易なことですが、同時に一定のリスクにも注意が必要です。

原理

この戦略の核心的なロジックは「双陰線」パターンを識別することです。具体的には、現在のローソク足が「始値=最安値、終値=最高値」という条件を満たすかどうかを判定します。これは下ヒゲと上ヒゲがないローソク足であり、「陰線」と呼びます。前のローソク足も同じ条件を満たしている場合、連続する2本の陰線、すなわち「双陰線」パターンが出現したと見なします。

テクニカル分析理論によれば、この双陰線パターンは通常、現在のトレンドが間もなく反転することを示唆します。連続する2本のローソク足の値動きが非常に狭い範囲に収まっているということは、買い手と売り手の力が均衡していることを意味し、反転の可能性を示唆します。

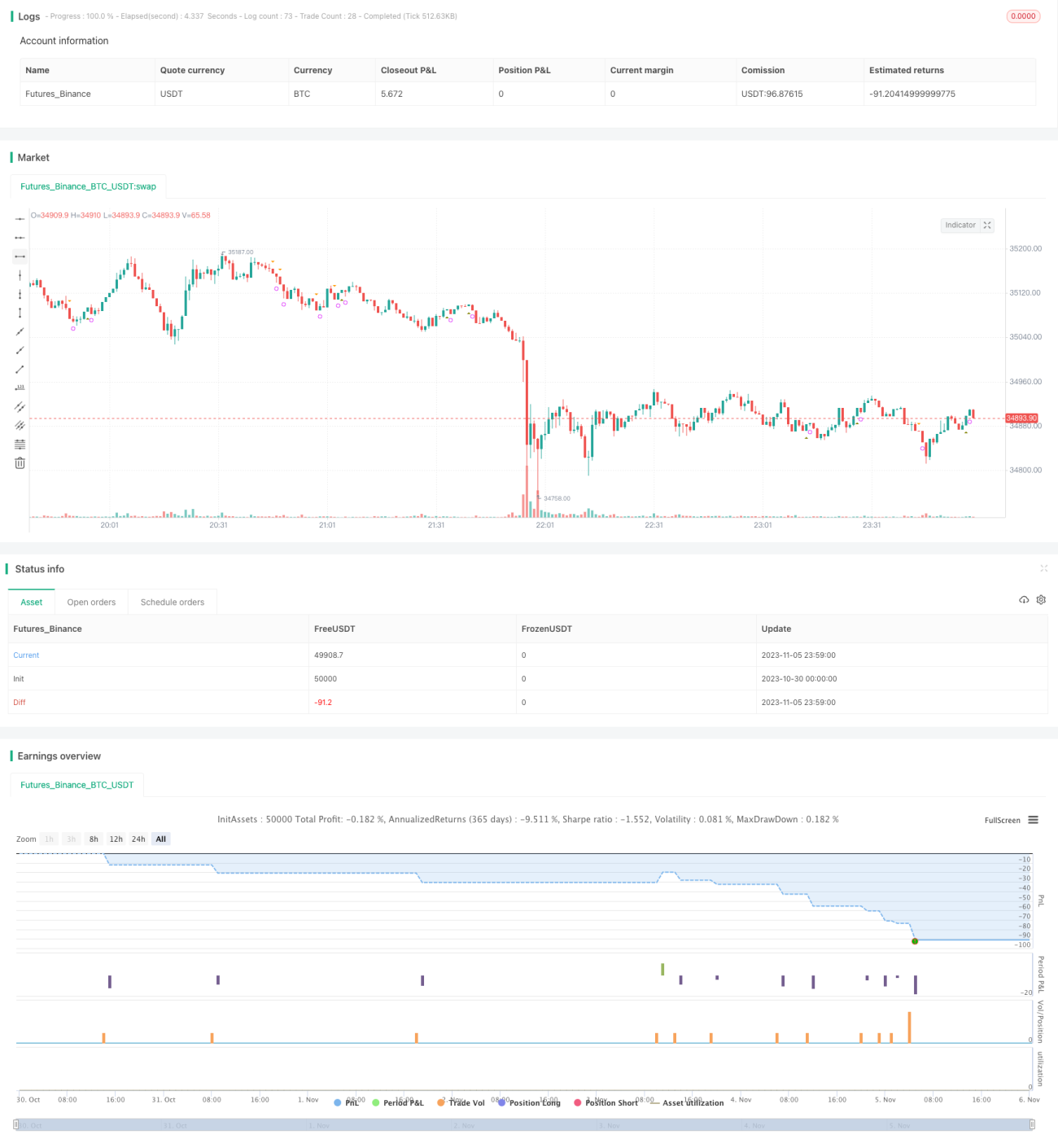

双陰線パターンを検出した後、戦略は次のローソク足の始値で、終値でロングまたはショートのポジションを取ります。そして、設定したバー数経過後に決済します。

優位性

- 戦略の考え方が明確で理解しやすく、シンプルなパターン判定であり、実装が容易です。

- 古典的な双陰線反転パターンを利用しており、一定のテクニカル分析の根拠があります。

- 取引頻度が高くなく、取引コストとリスクの低減に寄与します。

- バックテスト機能を簡単に追加でき、パラメータの最適化が可能です。

リスク

- パターン取引は過去のチャートの統計的確率に依存するため、乖離を完全に回避することはできません。

- 双陰線が反転を示唆していても、実際に反転が起こるとは限らず、維持される保証もありません。

- 固定された利食い幅では、相場が急変した場合に対応できません。

- 1~2本のローソク足の情報のみを見るため、過度に積極的なエントリー・エグジットにつながりやすいです。

最適化のアイデア

- トレンド指標を組み合わせて、逆張りを避ける。

- 確認を待ってエントリーし、反転確定シグナルを待つ。

- 損切り・利食いはATR(平均真のレンジ)に基づいて動的に設定し、固定日数にしない。

- 機械学習を用いて、どの双陰線パターンがより信頼できるかを判断する。

まとめ

双陰線反転戦略は、古典的なパターン取引の考え方を利用しており、シンプルで直感的です。初心者の学習に適しているだけでなく、ボットのモジュールの一つとしても利用できます。ただし、リスク管理には注意が必要であり、エントリータイミングや利食い方法の最適化によって改善できます。全体的に、この戦略の長所と短所はどちらも顕著であり、参考にすることができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1