バンドトレンドフォロワー

概要

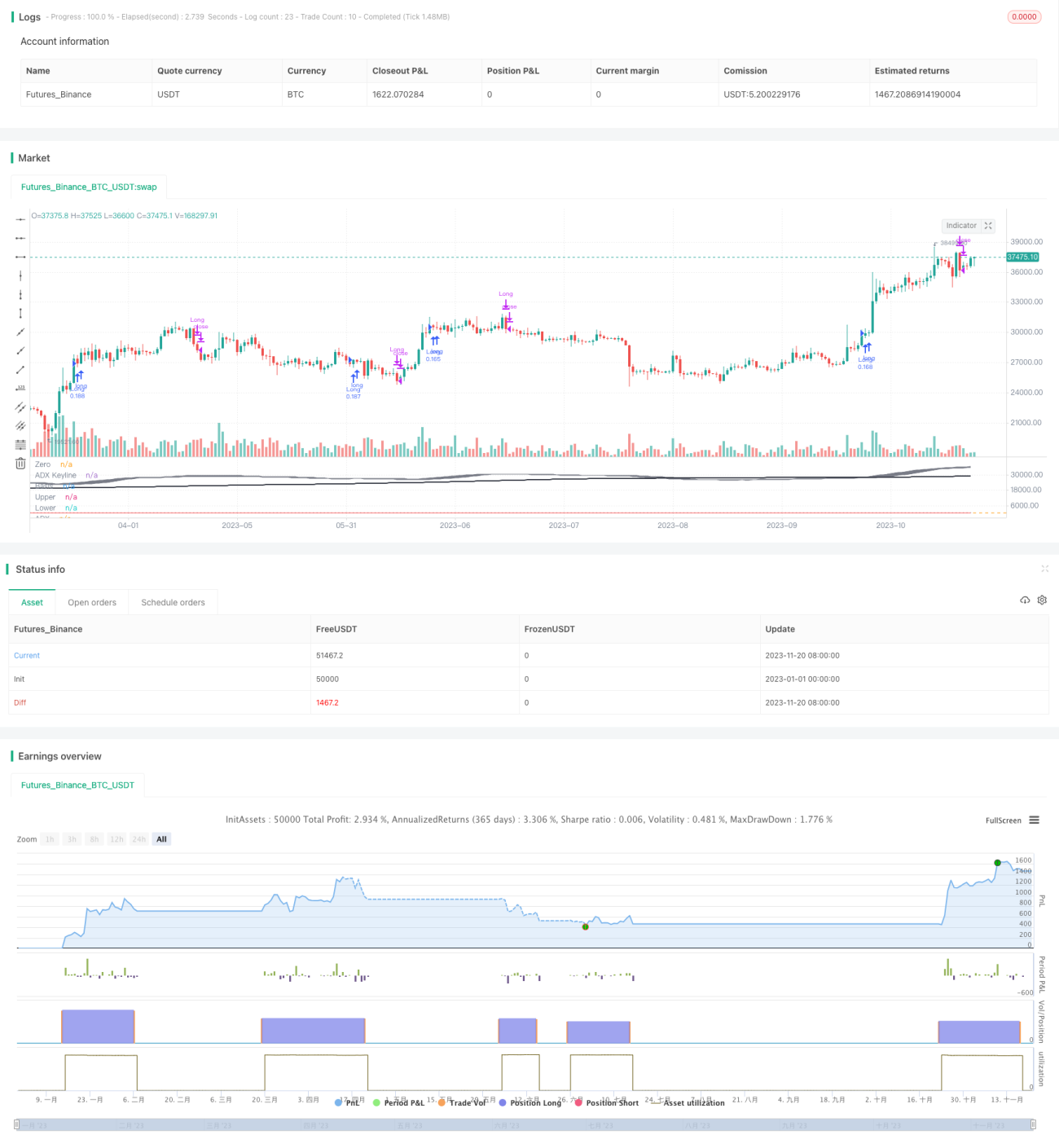

本戦略は、トレンド銘柄(またはその他のトレンド市場)を対象とした低リスク戦略であり、最小限のドローダウン率を目指します(例えば、本稿執筆時点で、AAPLのドローダウン率は約1.36%、FBは約1.93%、SPYは0.80%であり、いずれも収益を維持しています)。

戦略の原理

本戦略は、200日移動平均線、カスタムボリンジャーバンド、52期間加重移動平均TSI、およびADX強度を利用します。

買いシグナルは以下の通りです。終値が200日移動平均線を上回る + 5本のローソク足の終値がカスタムボリンジャーバンドの上部を上回る + TSIがプラス + ADXが20を超える。

バックテストの結果、本戦略はトレンド銘柄にのみ有効であることが証明されたため、売り/空売り条件を一部削除し、買い注文のみを採用しています。

優位性分析

本戦略の優位性は、ドローダウン率が低くリスクが最小限である点、ほとんどのトレンド銘柄に対する低リスク運用に適している点にあります。テストデータによれば、バックテスト期間中のAAPLの最大ドローダウンは1.36%、FBの最大ドローダウンは1.93%であり、高い収益を示しています。

ボリンジャーバンド、移動平均線、TSI指標など複数のテクニカル指標を組み合わせて使用し、ADXでトレンドの強さを判断することで、トレンドが上向きの時に買いを入れ、トレンド銘柄の中長期的な上昇のチャンスを捉えようとします。単一の指標による判断と比較して、本戦略は複数のテクニカル指標を総合的に活用するため、より正確で信頼性が高く、リスクも低くなります。

本戦略にはストップロス戦略も含まれており、TSI指標の方向転換時に迅速に損切りを行い、利益を最大限に確定し、リスクを効果的にコントロールします。

リスク分析

本戦略が主に直面するリスクは2つあります。

-

突発的なイベントリスク。一部のブラックスワン事象により、株価が大きく変動して下落し、ストップロスが機能しない可能性があります。

-

トレンド終了リスク。銘柄がトレンドからレンジ相場に移行した場合、大きなドローダウンが発生する可能性があります。

リスク1に対しては、より厳格なストップロスメカニズムを設定するか、手動でストップロスを介入させることができます。リスク2に対しては、トレンド終了を検知するために、出来高指標などを追加するなど、より多くの判断要素を組み合わせることができます。

最適化の方向性

本戦略は以下の点からさらに最適化が可能です。

-

ストップロス戦略を追加し、より正確なストップロスポイントを設定してリスクをより適切にコントロールする。

-

移動平均線のパラメータを最適化し、異なるパラメータ組み合わせの安定性をテストする。

-

出来高指標などの判断システムを追加し、トレンドの開始と終了をより正確に判断する。

-

より長い時間枠のパラメータをテストし、より長期的な運用に対応する。

まとめ

本戦略は、ADXでトレンドの強さを、TSI指標でトレンドの方向を、ボリンジャーバンドでブレイクアウトを、移動平均線で長期トレンドを判断し、複数の指標が相互に検証することで買いのタイミングを判断します。ストップロス戦略はリスクを効果的にコントロールできます。本戦略はトレンド銘柄の長期追跡に適しており、ドローダウン率が低く、収益が比較的高く、一定の優位性を持っています。ただし、リスクに対する最適化をさらに行い、より堅牢な戦略とすることが求められます。

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © gary_trades

//This script has been designed to be used on trending stocks as a low risk trade with minimal drawdown, utilising 200 Moving Average, Custom Bollinger Band, TSI with weighted moving average and ADX strength.

//Backtest dates are set to 2010 - 2020 and all other filters (moving average, ADX, TSI , Bollinger Band) are not locked so they can be user amended if desired. - 1