複数のインジケーターを組み合わせたビットコインのデイトレード戦略

概要

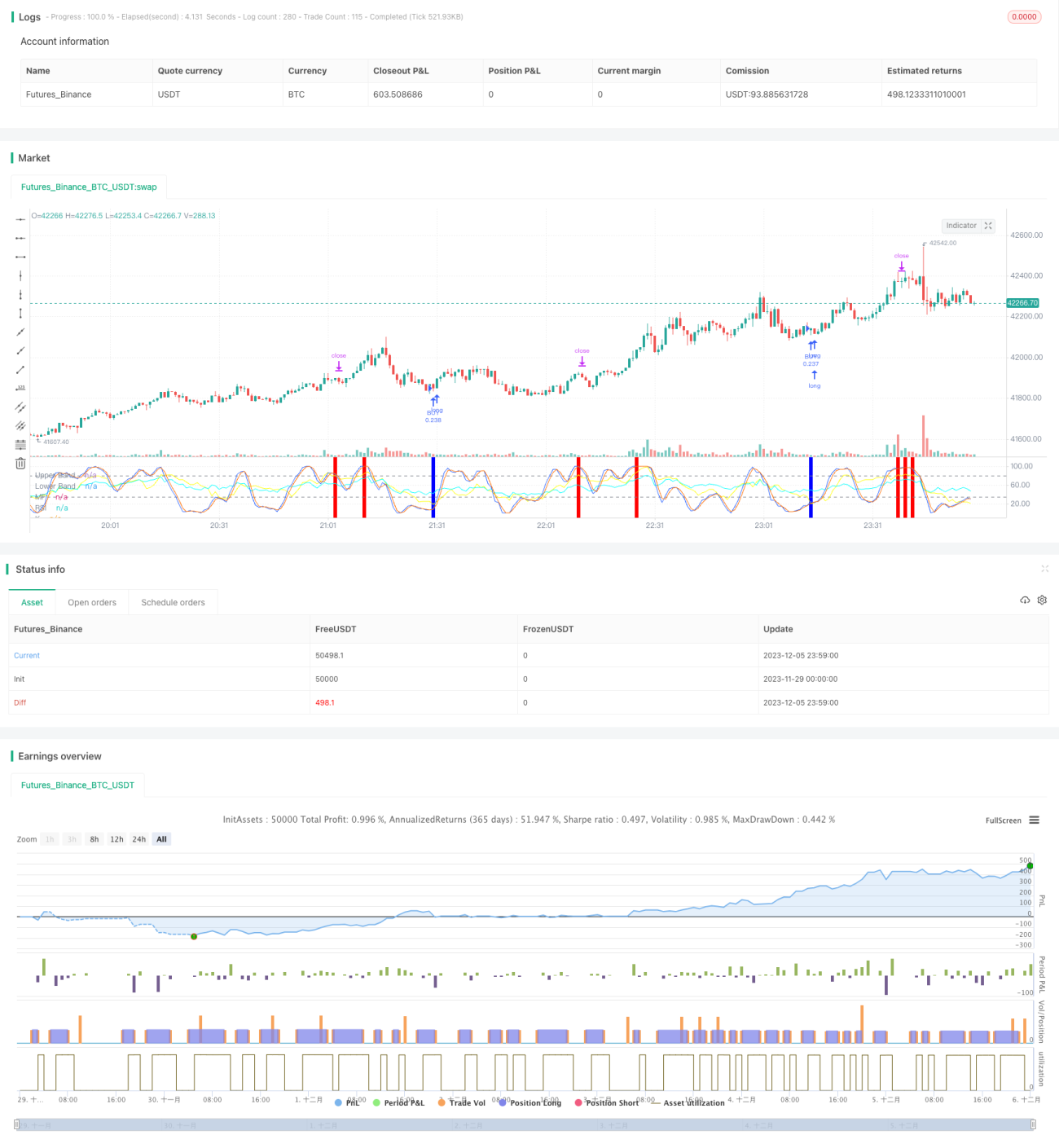

本戦略は、RSI、MFI、ストキャスティクスRSI、MACDの4つの指標を組み合わせ、ビットコインの日内取引を行います。複数の指標が同時に買いまたは売りのシグナルを発した場合にのみ注文を実行し、リスクを管理します。

戦略の原理

-

RSI指標は市場が買われすぎか売られすぎかを判断します。RSIが40未満で買いシグナル、70超で売りシグナルを生成します。

-

MFI指標は市場の資金フローを判断します。MFIが23未満で買いシグナル、80超で売りシグナルを生成します。

-

ストキャスティクスRSI指標は市場が買われすぎか売られすぎかを判断します。Kラインが34未満で買いシグナル、80超で売りシグナルを生成します。

-

MACD指標は市場のトレンドとモメンタムを判断します。高速線が低速線を下回り、ヒストグラムが負の値の場合に買いシグナル、逆の場合に売りシグナルを生成します。

優位性の分析

-

4つの指標を組み合わせることでシグナルの精度が向上し、単一指標の機能不全による損失を回避できます。

-

複数の指標が同時にシグナルを発した場合にのみ注文するため、偽シグナルの発生確率を大幅に低減できます。

-

日内取引戦略を採用することで、夜間のリスクを回避し、資金コストを低減します。

リスクとその解決方法

-

戦略の取引頻度が低くなる可能性があり、一定の時間リスクが存在します。指標パラメータを適宜緩和し、取引回数を増やすことができます。

-

指標が誤ったシグナルを発する確率は依然として存在します。機械学習アルゴリズムを導入し、指標シグナルの信頼性を補助的に判断することができます。

-

一定の買われすぎ・売られすぎリスクが存在します。指標パラメータを適宜調整するか、他の指標の判断ロジックを追加することができます。

最適化の方向性

-

適応型指標パラメータ機能を追加します。市場のボラティリティと変化速度に応じて、指標パラメータをリアルタイムで微調整します。

-

ストップロスロジックを追加します。損失が一定割合を超えた場合にストップロスで退出し、一取引あたりの損失を効果的に抑制します。

-

センチメント指標を組み合わせます。市場の熱気や恐怖度など多次元の判断を追加し、戦略の収益性を向上させます。

まとめ

本戦略は4つの指標が相互に検証しながらシグナルを発することで、偽シグナル率を効果的に低減でき、比較的安定した高頻度収益戦略です。パラメータとモデルの継続的な最適化により、戦略の勝率と収益性はさらに向上することが期待されます。

/*backtest

start: 2023-11-29 00:00:00

end: 2023-12-06 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('John Day Stop Loss', overlay=false, pyramiding=1, default_qty_type=strategy.cash, default_qty_value=10000, initial_capital=10000, currency='USD', precision=2)

strategy.risk.allow_entry_in(strategy.direction.long) - 1