乱数に基づくクォンツ取引戦略

1

Follow

1802

Followers

概要

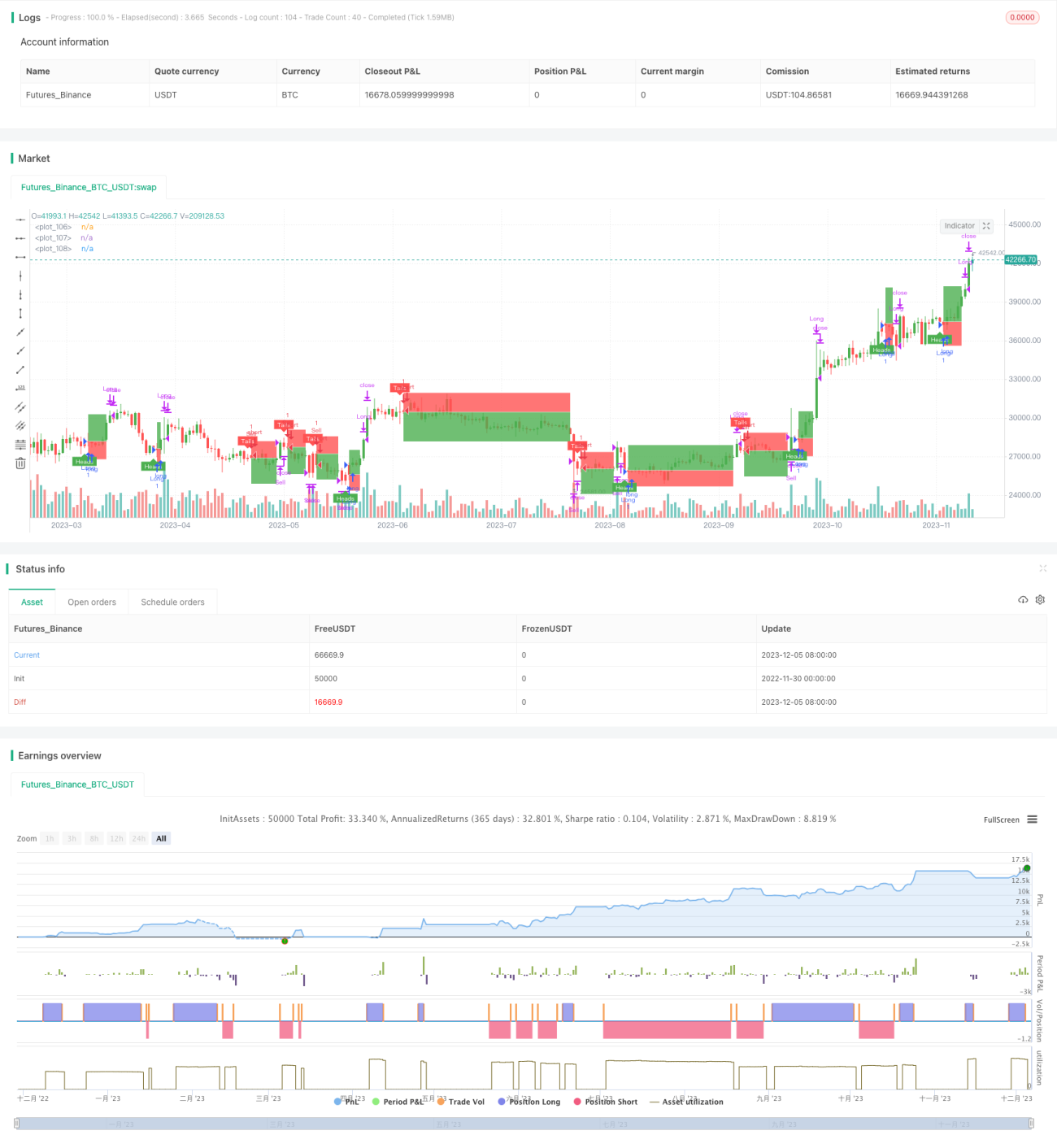

本戦略の核となる考え方は、乱数を用いてコイン投げやサイコロ振りなどの確率イベントをシミュレートし、その結果に基づいて買い(ロング)または売り(ショート)を決定することで、ランダムな取引を実現することです。この取引戦略はシミュレーションテストに利用できるほか、より複雑な戦略を開発するための基本フレームワークとしても使用できます。

戦略の原理

flip変数でランダムイベントをシミュレートし、coinLabel乱数の大きさに応じて買いまたは売りを決定します。riskとratioを用いてストップロスとテイクプロフィットのラインを設定します。- 設定した最大サイクル数に従って、ランダムに次の取引シグナルをトリガーします。

plotBox変数でポジションクローズボックスの表示有無を制御します。stoppedOutとtakeProfit変数でストップロスまたはテイクプロフィットを検出します。- バックテスト機能を提供し、戦略のパフォーマンスをテストします。

優位性分析

- コード構造が明確で、理解と二次開発が容易です。

- UIの対話性が高く、各種パラメータをグラフィカルなインターフェイスで調整できます。

- ランダム性が強く、市場の変動に影響されず、信頼性が高い。

- パラメータ最適化により、より良い収益率を得られる可能性があります。

- 他の戦略のデモやテストとして使用できます。

リスク分析

- ランダム取引では市場を判断できないため、収益に関するリスクが存在します。

- 最適なパラメータの組み合わせを特定できず、繰り返しテストが必要です。

- ランダムシグナルが過密になることで、スーパー相関リスクが生じる可能性があります。

- リスク管理のためにストップロス・テイクプロフィット機能と組み合わせることを推奨します。

- 取引間隔を適切に延長することでリスクを低減できます。

最適化の方向性

- より複雑なファクターを組み合わせてランダムシグナルを生成する。

- 取引銘柄を増やし、テスト範囲を拡大する。

- UIの対話性を最適化し、戦略コントロール機能を追加する。

- より多くのテストツールや指標を提供し、パラメータ最適化を容易にする。

- 取引シグナルやストップロス・テイクプロフィットコンポーネントとして他の戦略に組み込む。

まとめ

本戦略は全体的なフレームワークが完成しており、ランダムイベントに基づいて取引シグナルを生成するため、信頼性が高いです。同時に、パラメータ調整、バックテスト、プロット機能を備えています。初心者が戦略開発をテストするためにも、他の戦略の基本モジュールとしても使用できます。適切な最適化により、戦略のパフォーマンスをさらに向上させることができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1