スマート量化低点反転戦略

概要

本戦略は、暗号通貨を対象としたスマートな定量化ボトム反転トレーディング戦略です。マルチタイムフレーム技術と適応型RSIインジケーターを活用し、市場の短期的な底値の可能性を判断し、底値付近で反転エントリーすることで超過収益を獲得します。

戦略の原理

まず、この戦略は変化量と出来高を用いて適応型RSIインジケーターを計算し、市場の短期的な底値の可能性を判断します。次にマルチタイムフレーム技術を組み合わせ、より大きな時間軸で底値シグナルを確定します。適応型RSIのラインが0水準を下から上にクロスしたときに買いシグナルが発生します。

具体的には、適応型RSIの計算方法は次のとおりです。まず各ローソク足の変化量を計算し、そのローソク足の出来高を計算し、変化量に出来高を乗じてそのローソク足の定量化された強さを求めます。この定量化された強さに対してRSI計算を行い、N期間の平均を取ることで適応型RSIを算出します。このインジケーターは市場の底値を明確に判断できます。

これに基づき、本戦略ではさらにマルチタイムフレーム技術を導入し、より高次の時間軸でシグナルを判断することで、短期の市場ノイズによる撹乱を回避します。高次時間軸の移動平均線が底値から反転した時点を、本戦略の買いタイミングと判断します。

優位性分析

本戦略の最大の利点は、適応型RSIインジケーターを用いて市場の短期的な底値を正確に判断できる点にあり、これにより底値反転トレードに有効なシグナルを提供します。さらに、マルチタイムフレーム技術の導入によりシグナルの質が向上し、短期的な市場ノイズによる撹乱を回避できます。

従来のRSIと比較して、適応型RSIは定量化された強さの計算が加わっているため、変動の激しい暗号通貨市場に対してより敏感に反応し、より早く正確に市場の底値を判断できます。これにより底値反転トレードにおいて先行優位性を得られます。

また、本戦略はトレンドフォローと反転トレードの両方の長所を兼ね備えています。トレンドが不明瞭な市場では反転トレードで利益を得ることができ、明確な強気相場ではトレンドに追随して運用することも可能です。

リスク分析

本戦略の主なリスクは、底値判断の精度が100%保証されないことです。市場は短期的に大きな非合理的な変動を起こすことがあります。底値がさらに下落した場合、大きなストップロスのリスクに直面します。

また、マルチタイムフレーム間でもダイバージェンスが発生する可能性があります。高時間軸のシグナルが遅延した場合、トレードの損失につながる恐れがあります。

リスク管理として、本戦略は比較的保守的なストップロス機構を採用し、分割利確を設定して段階的に収益を最適化します。また、適応型RSIのパラメータを適宜調整し、底値判断の精度を最適化することも可能です。

最適化の方向性

本戦略は以下の点から最適化が可能です。

-

適応型RSIインジケーターのパラメータを最適化し、市場の底値判断精度を向上させる。さまざまな周期パラメータを試すことができます。

-

他のインジケーターを追加して確認を行い、誤ったシグナルを回避する。例えば出来高インジケーターとの組み合わせなど。

-

ストップロス機構を最適化し、リワード/リスク比を維持しつつ、ストップロス幅を適度に拡大して、より多くのトレンド利益を獲得する。

-

時間枠の選択を最適化し、より大きな時間軸でシグナルの信頼性を確保する。日足、週足などより高次の移動平均線をテストする。

-

本戦略をさまざまな暗号通貨銘柄でテストし、最適な銘柄を選択する。

まとめ

本スマートな定量化ボトム反転戦略は、適応型RSIインジケーターとマルチタイムフレーム技術を用いて市場の短期的な底値の可能性を判断します。その反転トレード特性により、不確実な相場において超過収益を得ることができます。同時に明確なトレンド相場にも追随可能です。継続的な最適化により、本戦略はより信頼性の高いトレードシグナルを獲得し、長期的な安定収益を得ることが期待されます。

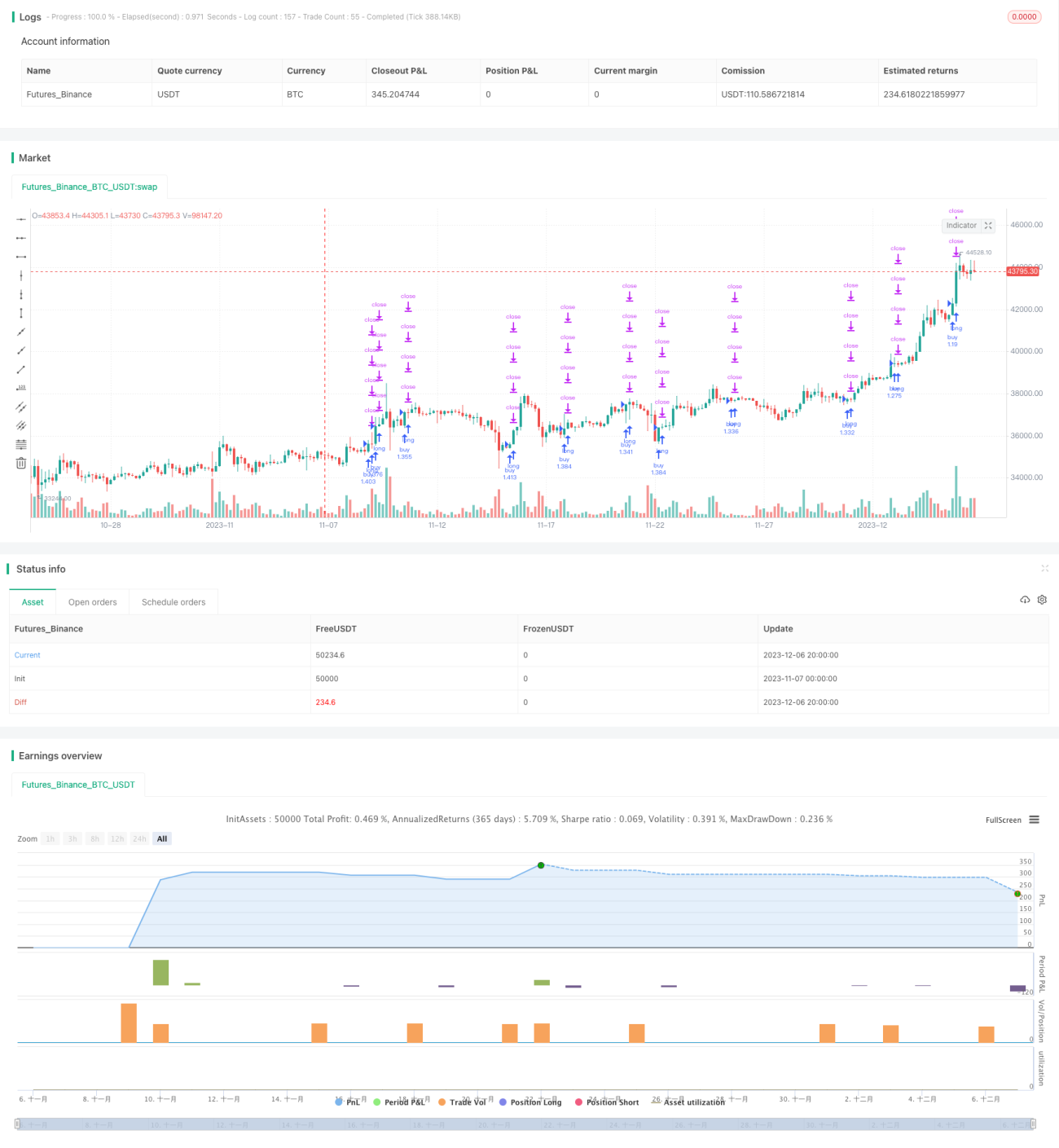

/*backtest

start: 2023-11-07 00:00:00

end: 2023-12-07 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © theCrypster 2020

//@version=4

strategy(title = "Low Scanner strategy crypto", overlay = false, pyramiding=1,initial_capital = 1000, default_qty_type= strategy.percent_of_equity, default_qty_value = 100, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0.075)- 1