ブレイクアウトフォロー戦略

概要

この戦略の主な考えは,より大きな時間枠でトレンドの方向を識別し,より小さな時間枠で突破点の入場を探すことであり,ストップ・エグジットは,より大きな時間枠で移動平均を追跡することである.

戦略原則

この戦略は主に3つの指標に基づいて判断されます.

第一に,より長い周期 (日線など) のX日のシンプル移動平均を計算し,その移動平均が価格ステーションにある時にのみ購入を許す.これは,全体的なトレンドの方向を判断して,取引の揺れ期を避けるために使用できる.

2つ目は,より短い周期 (例えば5日) 内の最高価格のSwing Highを計算し,価格がこの最高価格を破るときに買入シグナルを誘発する.

3つ目は,ストップラインを設定する. ポジションに入ると,ストップラインは,最近の低点から一定の周期lbStopの最低価格にロックする. また,出口機構として移動平均 (日線10日EMAのような) を設定し,価格が移動平均より低いときにポジションを退出する.

この戦略は,過剰なポイント購入を避けるためにATR値を設定します. また,再測定時間範囲などの他の補助条件があります.

この3つの指標の相互作用は,この戦略の核心的な論理を形成しています.

戦略的優位分析

これは突破的な追跡戦略で,以下の利点があります.

-

2つのタイムフレームを使用し,波動的な市場の偽の突破に囚われないようにする.長いタイムフレームは,全体的なトレンドを判断し,短いタイムフレームは,特定の入場点を探す.

-

スウィングハイが形成される突破点を利用して,このような突破は一定の慣性を持ち,簡単に追跡できる.また,周期lbのパラメータを振り返って,本当に有効な突破を探すことができる.

-

止損は厳格な方法で,近年の低値を追跡し,一定の緩衝距離を残して,<unk>盤を避ける.

-

移動平均を退出メカニズムとして使用し,状況に応じて柔軟に停止することができます.

-

ATR指標は,過剰放出によるリスクを回避する.

-

異なるパラメータの組み合わせを設定して効果をテストし,最適化スペースを広げる.

リスク分析

この戦略にはいくつかのリスクがあります.

-

価格が移動平均の近くで上下振動するときは,繰り返し切替されやすい.このとき,高い手数料のリスクに直面する.

-

移動平均の近くで購入ポイントを突破すると,相対的に大きな撤回リスクがあります.これは戦略そのものの特徴です.

-

市場動向がはっきりしない場合,長期にわたって保有し,時間的なリスクに直面する可能性があります.

-

ATRパラメータを合理的に設定する必要があります.ATRが小さすぎるとフィルタリング効果が弱く,大きすぎると入場機会が減少します.

-

異なるlbパラメータが結果に影響を及ぼすことをテストする必要があります. 大きすぎるパラメータは,いくつかの機会を逃し,小さすぎるパラメータは,偽突破を認識する可能性があります.

リスク対策:

- 移動平均のパラメータを適切に調整し,フィルタリング効果を追加します.

- ATRのパラメータを最適化し,視覚的な判断を補助する.

- 周期lbを調整して,最適なパラメータを探します.

- 震災の際に取引を停止する.

戦略最適化の方向性

この戦略は以下の側面から最適化できます.

-

異なる移動平均のパラメータの組み合わせをテストし,最適なパラメータを探します.

-

異なるATRパラメータ設定を試し,入場機会とリスク管理をバランスさせる.

-

周期lbのパラメータを最適化して,より効率的な突破を識別する.

-

動的ストップを設定し,波動率と撤回によってリスクを制御する.

-

取引量指数などの他の要因と組み合わせて,突破の有効性を判断する.

-

極限点を参照として探す方法を開発する.

-

Machine Learning を使って,パラメータを訓練して,最適のパラメータを得ます.

要約する

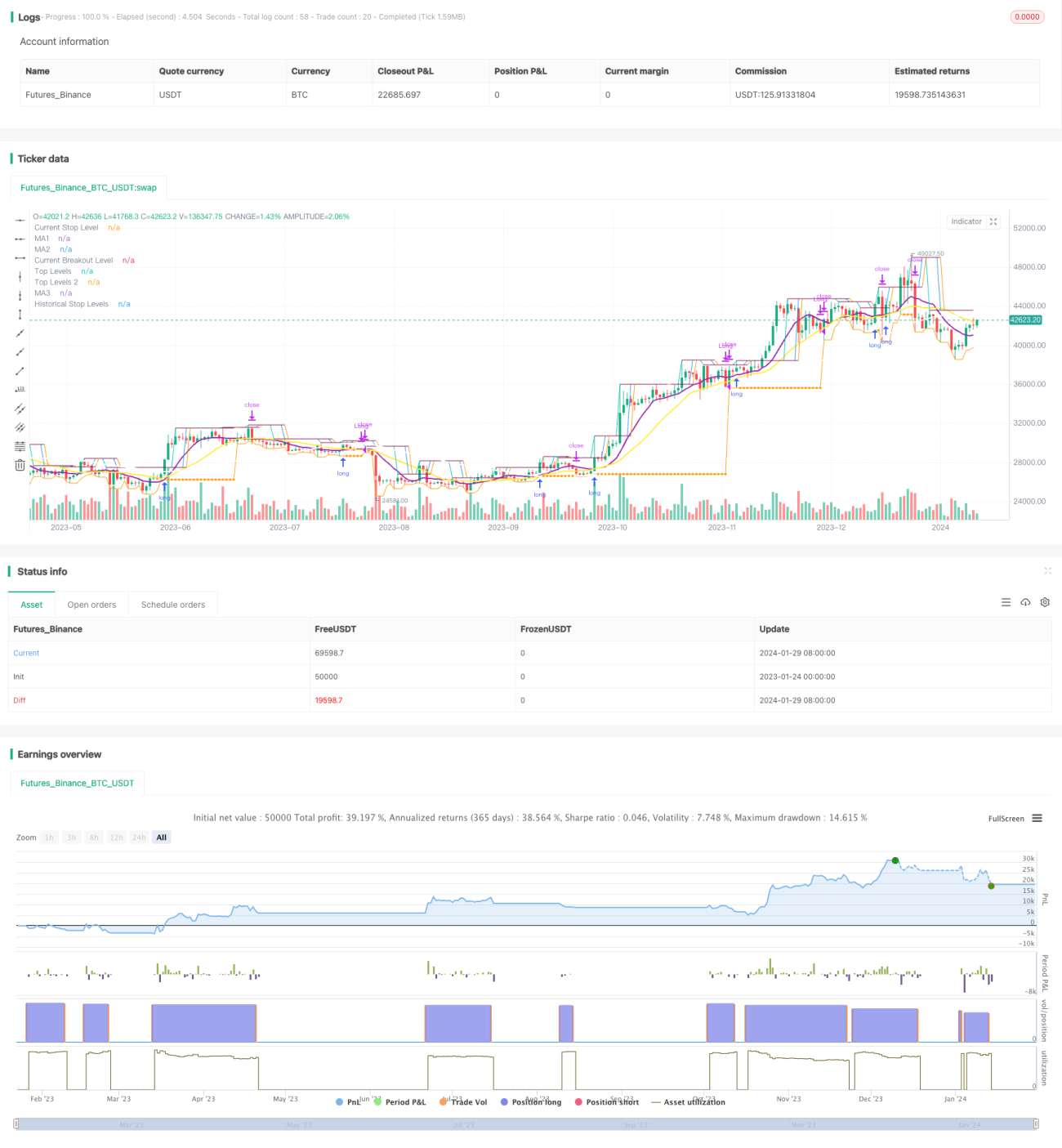

この戦略の全体は,典型的な突破追跡戦略である。二時間枠判断,Swing Highの入場タイミング,止損線,移動平均の二重保険退出機構を識別し,完全な論理体系を形成している。この戦略のリスクと利益の特徴は,より明確であり,中長期線を追跡するタイプの投資家に適している。ある程度のリスクは存在するが,パラメータ最適化とルール最適化によってリスクレベルを低減することができる。この戦略には,改善の余地があり,より多くの指標判断と組み合わせれば,戦略の効果をさらに強化する可能性がある。

/*backtest

start: 2023-01-24 00:00:00

end: 2024-01-30 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1