개요

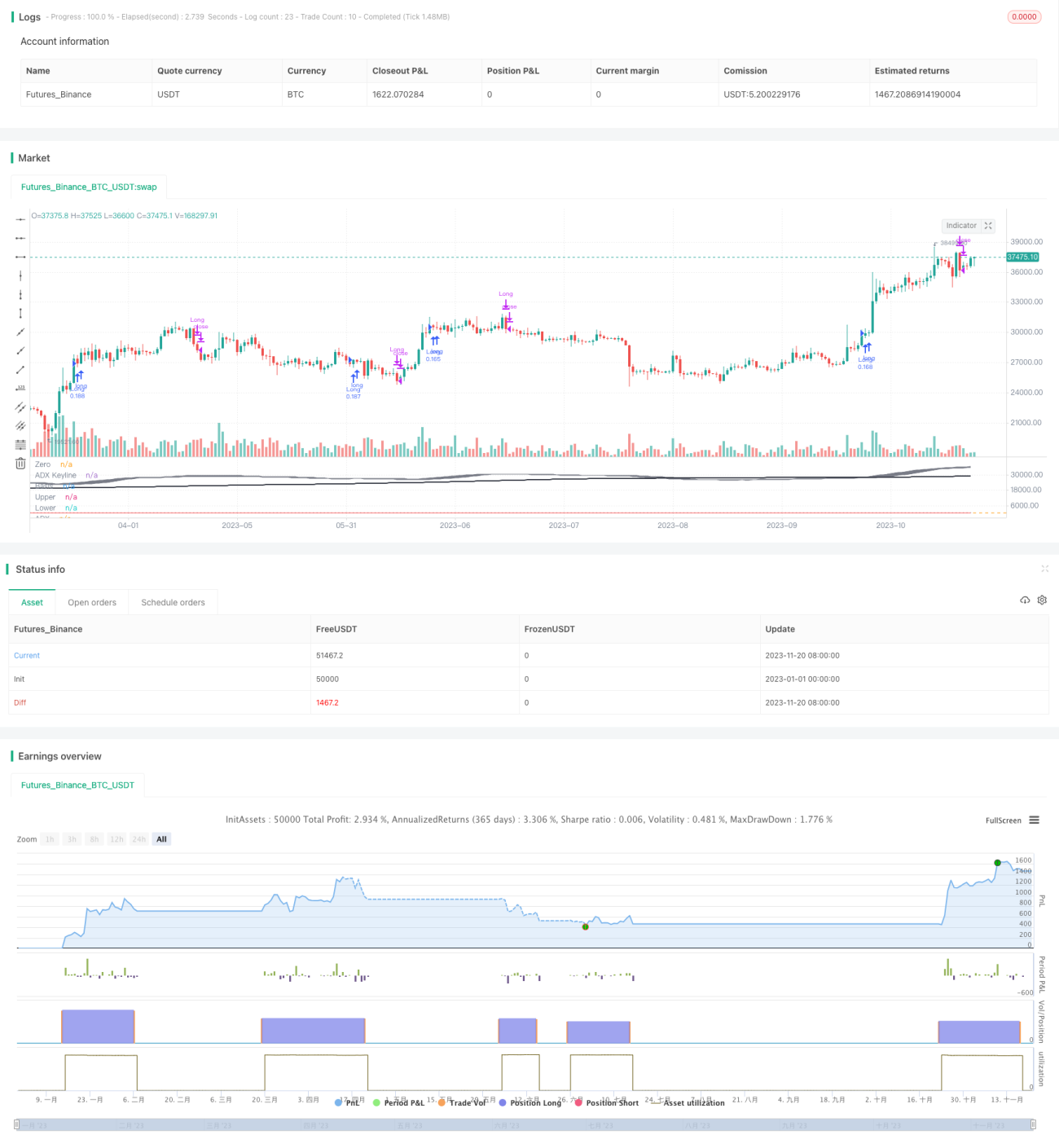

해당 전략은 추세주(또는 다른 추세성 시장)를 추적하는 저위험 전략으로, 최소한의 하락률을 목표로 합니다(예: 글 작성 시점 기준, AAPL은 약 1.36% 하락률, FB는 약 1.93%, SPY는 0.80% 하락률을 기록하며 모두 수익성을 유지하고 있습니다).

전략 원리

이 전략은 200일 이동평균선, 사용자 정의 볼린저 밴드, 52주기 가중 이동평균 TSI 및 ADX 강도를 활용합니다.

매수 신호는 다음과 같습니다: 종가가 200일 이동평균선 위에 있고 + 5개 캔들의 종가가 사용자 정의 상단 볼린저 밴드 위에 있으며 + TSI가 양수이고 + ADX가 20 이상입니다.

백테스트 결과 이 전략은 추세주에만 적용 가능함이 입증되었으므로, 일부 매도/공매도 조건을 삭제하고 롱 포지션(Long Position)만 취합니다.

장점 분석

이 전략의 장점은 낮은 하락률과 최소한의 위험에 있으며, 대부분의 추세주에 대한 저위험 운영에 적합합니다. 테스트 데이터에 따르면 수익률이 높고, 백테스트 기간 동안 AAPL의 최대 하락률은 1.36%, FB는 1.93%에 불과했습니다.

볼린저 밴드, 이동평균선, TSI 지표 등 다양한 기술적 지표를 조합하여 사용하고, ADX로 추세 강도를 판단하여 추세 상승 시 매수함으로써 추세주의 중장기 상승 기회를 포착하려 합니다. 단일 지표 판단에 비해 이 전략은 여러 기술 지표를 종합적으로 활용하여 더 정확하고 신뢰할 수 있으며 리스크가 낮습니다.

또한 이 전략은 손절매 전략을 포함하고 있어, TSI 지표 방향 전환 시 신속히 손절매하여 수익을 최대한 확보하고 리스크를 효과적으로 통제합니다.

리스크 분석

이 전략이 주로 직면하는 리스크는 두 가지입니다:

-

예상치 못한 사건 리스크. 특정 블랙스완 사건이 발생하면 주가가 급격히 변동하여 하락할 수 있으며, 손절매가 불가능할 수 있습니다.

-

추세 종료 리스크. 주가가 추세에서 횡보로 전환될 때 큰 하락이 발생할 수 있습니다.

첫 번째 리스크에 대해서는 보다 엄격한 손절매 메커니즘을 설정하거나 수동 개입을 통해 손절매할 수 있습니다. 두 번째 리스크에 대해서는 거래량 지표 등을 추가하여 추세 종료를 감지하는 판단 요소를 더 많이 결합할 수 있습니다.

최적화 방향

이 전략은 다음과 같은 측면에서 추가 최적화가 가능합니다:

-

손절매 전략을 추가하고, 더 정확한 손절매 지점을 설정하여 리스크를 더 잘 통제합니다.

-

이동평균선 매개변수를 최적화하고, 다양한 매개변수 조합의 안정성을 테스트합니다.

-

거래량 지표 등 판단 시스템을 추가하여 추세의 시작과 종료를 더 정확하게 판단합니다.

-

더 긴 시간 주기 매개변수를 테스트하여 장기 운영에 적응합니다.

요약

이 전략은 ADX로 추세 강도를 판단하고, TSI 지표로 추세 방향을 파악하며, 볼린저 밴드로 돌파를 확인하고, 이동평균선으로 장기 추세를 분석하는 등 여러 지표를 상호 검증하여 매수 시점을 결정합니다. 손절매 전략을 통해 리스크를 효과적으로 통제할 수 있습니다. 이 전략은 장기 추세주 추적에 적합하며, 하락률이 낮고 수익률이 비교적 높아 일정한 장점을 가지고 있습니다. 그러나 리스크에 대한 최적화를 통해 전략을 더욱 안정적으로 만드는 것이 필요합니다.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © gary_trades

//This script has been designed to be used on trending stocks as a low risk trade with minimal drawdown, utilising 200 Moving Average, Custom Bollinger Band, TSI with weighted moving average and ADX strength.

//Backtest dates are set to 2010 - 2020 and all other filters (moving average, ADX, TSI , Bollinger Band) are not locked so they can be user amended if desired. - 1