다중 지표를 결합한 비트코인 데이 트레이딩 전략

개요

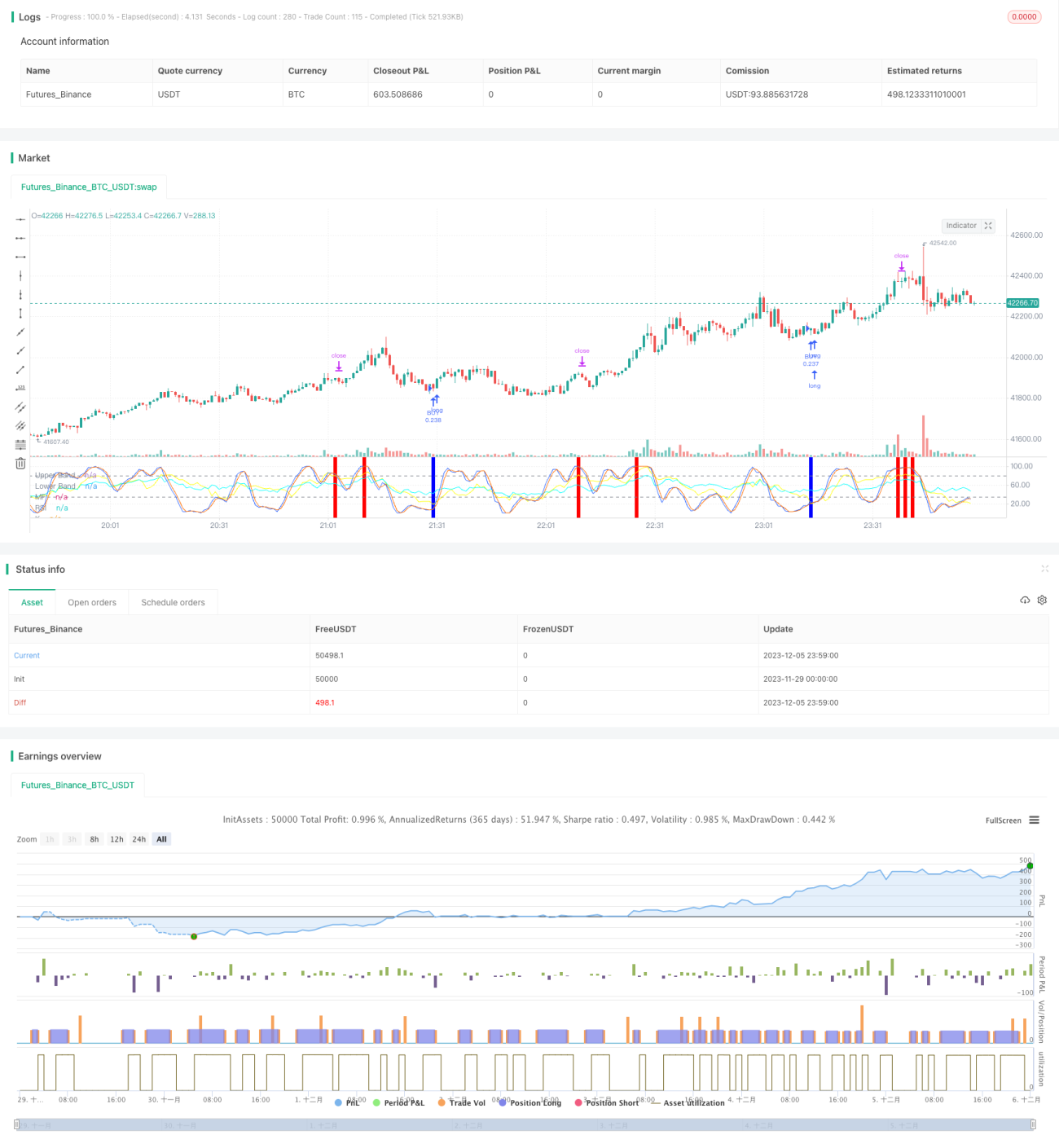

본 전략은 RSI, MFI, Stoch RSI 및 MACD 네 가지 지표를 결합하여 비트코인의 일중 거래를 구현합니다. 여러 지표가 동시에 매수 또는 매도 신호를 발생시킬 때만 전략이 주문을 실행하여 위험을 통제합니다.

전략 원리

-

RSI 지표는 시장이 과매수 또는 과매도 상태인지 판단하는 데 사용됩니다. RSI가 40 미만일 때 매수 신호가 발생하고, 70 이상일 때 매도 신호가 발생합니다.

-

MFI 지표는 시장의 자금 흐름을 판단합니다. MFI가 23 미만일 때 매수 신호가 발생하고, 80 이상일 때 매도 신호가 발생합니다.

-

Stoch RSI 지표는 시장이 과매수 또는 과매도 상태인지 판단합니다. K선이 34 미만일 때 매수 신호가 발생하고, 80 이상일 때 매도 신호가 발생합니다.

-

MACD 지표는 시장 추세와 모멘텀을 판단합니다. 빠른 선이 느린 선보다 낮고 히스토그램이 음수일 때 매수 신호가 발생하며, 반대의 경우 매도 신호가 발생합니다.

장점 분석

-

네 가지 주요 지표를 결합하여 신호의 정확성을 높이고, 단일 지표의 실패로 인한 손실을 방지합니다.

-

여러 지표가 동시에 신호를 보낼 때만 주문을 실행하므로 가짜 신호의 확률을 크게 낮출 수 있습니다.

-

일중 거래 전략을 채택하여 야간 위험을 피하고 자금 비용을 낮춥니다.

위험 및 해결 방법

-

전략의 거래 빈도가 낮을 수 있으며, 일정한 시간 위험이 존재합니다. 지표 매개변수를 적절히 완화하여 거래 횟수를 늘릴 수 있습니다.

-

지표가 잘못된 신호를 보낼 확률은 여전히 존재합니다. 머신러닝 알고리즘을 도입하여 지표 신호의 신뢰성을 보조적으로 판단할 수 있습니다.

-

일정한 과매수 및 과매도 위험이 존재합니다. 지표 매개변수를 적절히 조정하거나 다른 지표 판단 로직을 추가할 수 있습니다.

최적화 방향

-

적응형 지표 매개변수 기능을 추가합니다. 시장 변동성과 변화 속도에 따라 지표 매개변수를 실시간으로 미세 조정합니다.

-

손절매 로직을 추가합니다. 손실이 일정 비율을 초과하면 손절매하여 단일 거래 손실을 효과적으로 제어합니다.

-

감정 지표를 결합합니다. 시장 열기, 시장 공포도 등 다차원 판단을 추가하여 전략의 수익 공간을 높입니다.

요약

본 전략은 네 가지 주요 지표가 서로 검증하는 방식으로 신호를 발생시켜 가짜 신호율을 효과적으로 낮출 수 있으며, 비교적 안정적인 고빈도 수익 전략입니다. 매개변수와 모델의 지속적인 최적화에 따라 전략의 승률과 수익 능력이 더욱 향상될 것으로 기대됩니다.

/*backtest

start: 2023-11-29 00:00:00

end: 2023-12-06 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('John Day Stop Loss', overlay=false, pyramiding=1, default_qty_type=strategy.cash, default_qty_value=10000, initial_capital=10000, currency='USD', precision=2)

strategy.risk.allow_entry_in(strategy.direction.long) - 1