EMA/ADX/VOL - Pembunuh Kripto

Gunakan sistem purata bergerak EMA untuk menentukan arah trend, penunjuk ADX untuk menentukan kekuatan trend, dan gabungkan penapisan volum dagangan untuk strategi dagangan kuantitatif masuk.

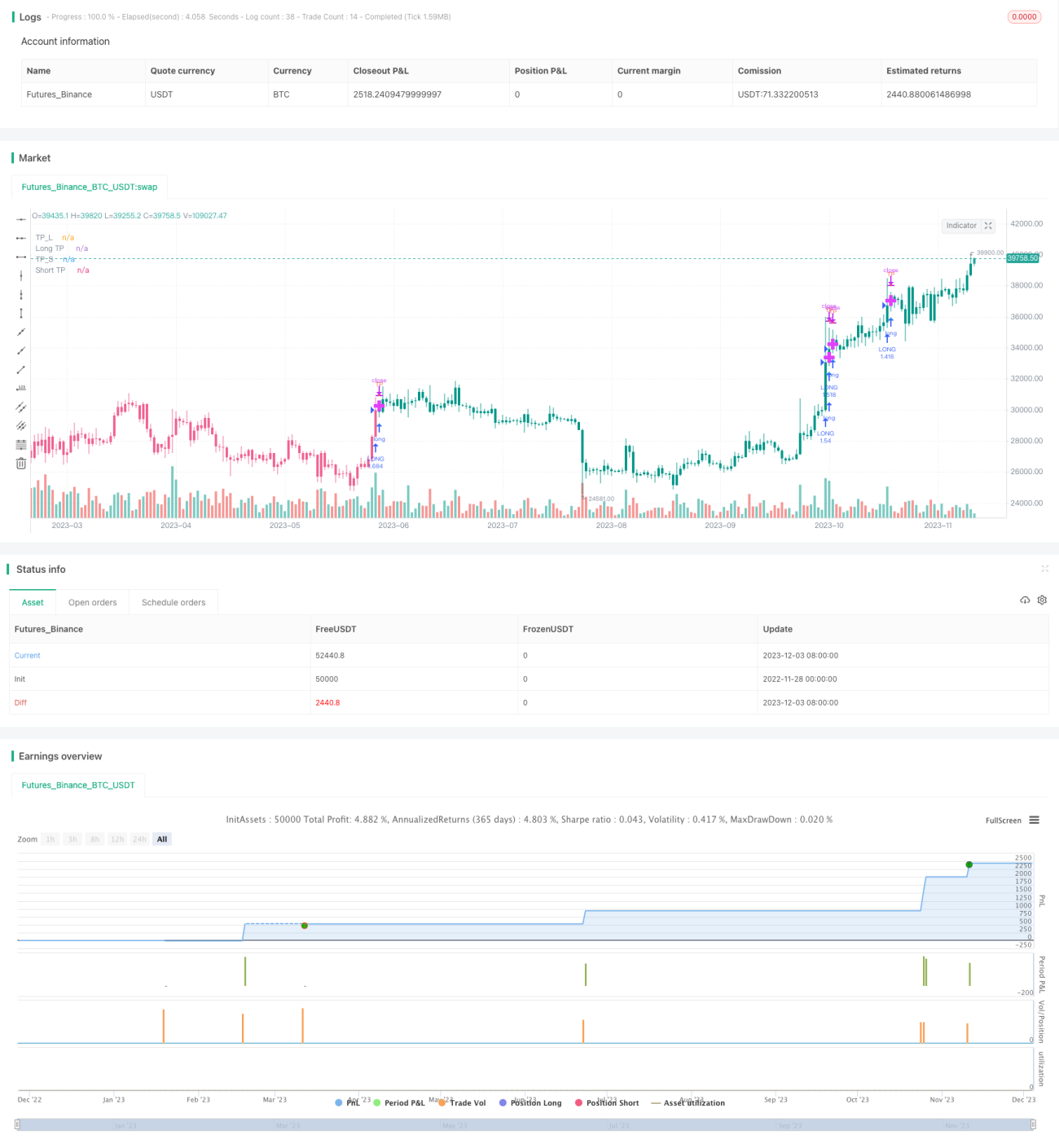

Prinsip

Strategi ini pertama kali menggunakan 5 EMA dengan tempoh berbeza untuk menentukan arah trend harga. Apabila kesemua 5 EMA meningkat, ia dianggap sebagai arah kenaikan; apabila kesemua 5 EMA menurun, ia dianggap sebagai arah penurunan.

Kemudian, gunakan penunjuk ADX untuk menentukan kekuatan trend. Apabila garis DI+ melebihi garis DI- dan nilai ADX melebihi ambang yang ditetapkan, ia dianggap sebagai pasaran kenaikan kukuh. Apabila garis DI- melebihi garis DI+ dan nilai ADX melebihi ambang, ia dianggap sebagai pasaran penurunan.

Pada masa yang sama, gunakan lonjakan volum dagangan sebagai pengesahan tambahan, memerlukan volum Kbar semasa melebihi gandaan purata volum dalam tempoh tertentu, bagi mengelakkan kesilapan masuk di kawasan volum rendah.

Gabungan arah trend, kekuatan trend, dan volum dagangan membentuk logik buka posisi beli dan jual strategi ini.

Kelebihan

-

Menggunakan sistem EMA untuk menentukan arah trend adalah lebih boleh dipercayai berbanding menggunakan satu EMA sahaja.

-

Menggunakan penunjuk ADX untuk menentukan kekuatan trend, mengelakkan kesilapan masuk ketika tiada arah yang jelas.

-

Mekanisme penapisan volum dagangan memastikan terdapat sokongan volum yang mencukupi, meningkatkan kebolehpercayaan strategi.

-

Gabungan pelbagai syarat menjadikan isyarat masuk lebih tepat dan boleh dipercayai.

-

Strategi ini mempunyai banyak parameter yang boleh dioptimumkan untuk meningkatkan prestasi secara berterusan.

Risiko dan Penyelesaian

-

Dalam pasaran yang berombak (sideways), EMA, ADX dan lain-lain mungkin memberikan isyarat palsu, menyebabkan kerugian yang tidak perlu. Anda boleh melaraskan parameter dengan sewajarnya atau menambah penunjuk lain untuk bantuan penentuan.

-

Syarat penapisan volum yang terlalu ketat mungkin menyebabkan terlepas peluang pasaran. Anda boleh mengurangkan parameter penapisan volum.

-

Frekuensi dagangan yang dihasilkan oleh strategi mungkin agak tinggi; perhatikan pengurusan modal dan kawal saiz posisi setiap dagangan dengan sewajarnya.

Arah Pengoptimuman

-

Uji pelbagai kombinasi parameter untuk mencari parameter terbaik dan meningkatkan prestasi strategi.

-

Tambah penunjuk lain seperti MACD, KDJ, dan gabungkan dengan EMA serta ADX untuk membentuk penentuan buka posisi yang lebih kukuh.

-

Tambah strategi stop loss untuk mengawal risiko dengan lebih lanjut.

-

Optimumkan strategi pengurusan kedudukan untuk mencapai pengurusan modal yang lebih saintifik.

Kesimpulan

Strategi ini mempertimbangkan arah trend harga, kekuatan trend, dan maklumat volum dagangan untuk membentuk peraturan buka posisi. Ia mengelakkan perangkap biasa pada tahap tertentu dan mempunyai kebolehpercayaan yang tinggi. Walau bagaimanapun, ia masih perlu diperbaiki melalui pengoptimuman parameter, pemilihan penunjuk, dan kawalan risiko untuk meningkatkan prestasi selanjutnya. Secara keseluruhannya, rangka kerja strategi ini mempunyai potensi pengembangan dan ruang pengoptimuman yang besar.

- 1