EMA/ADX/VOL - Assassino de Criptomoedas

Estratégia de trading quantitativo que utiliza o sistema de médias móveis EMA para determinar a direção da tendência, o indicador ADX para avaliar a força da tendência e a filtragem por volume para entrar no mercado.

Princípio

A estratégia primeiro utiliza 5 EMAs de diferentes períodos para determinar a direção da tendência de preço. Quando todas as 5 EMAs estão subindo, considera-se que uma tendência de alta se formou; quando todas as 5 EMAs estão caindo, considera-se que uma tendência de baixa se formou.

Em seguida, utiliza-se o indicador ADX para avaliar a força da tendência. Quando a linha DI+ está acima da linha DI- e o valor do ADX ultrapassa o limite definido, considera-se um mercado de alta forte; quando a linha DI- está acima da linha DI+ e o valor do ADX ultrapassa o limite definido, considera-se um mercado de baixa forte.

Ao mesmo tempo, utiliza-se o rompimento do volume como confirmação adicional, exigindo que o volume do candle atual seja maior que um múltiplo da média de volume em um determinado período, evitando assim entradas equivocadas em locais de baixo volume.

Combinando a direção da tendência, a força da tendência e o volume, forma-se a lógica de abertura de posições longas e curtas desta estratégia.

Vantagens

- O uso do sistema de médias móveis EMA para determinar a direção da tendência é mais confiável do que usar uma única EMA.

- O indicador ADX ajuda a avaliar a força da tendência, evitando entradas equivocadas quando não há tendência clara.

- O mecanismo de filtragem por volume garante suporte de volume suficiente, aumentando a confiabilidade da estratégia.

- A combinação de múltiplas condições torna os sinais de abertura mais precisos e confiáveis.

- A estratégia possui vários parâmetros que podem ser otimizados para melhorar continuamente seu desempenho.

Riscos e soluções

- Em mercados laterais, as avaliações das EMAs e do ADX podem gerar sinais falsos, resultando em perdas desnecessárias. É possível ajustar adequadamente os parâmetros ou adicionar outros indicadores para auxiliar a análise.

- Se a condição de filtragem por volume for muito rigorosa, pode-se perder oportunidades de movimento. É possível reduzir o parâmetro de filtragem de volume.

- A estratégia pode gerar uma frequência de negociações relativamente alta, sendo necessário atenção ao gerenciamento de capital e controle adequado do tamanho da posição por operação.

Direções de otimização

- Testar diferentes combinações de parâmetros para encontrar os melhores e melhorar o desempenho da estratégia.

- Adicionar outros indicadores, como MACD, KDJ, etc., em combinação com as EMAs e o ADX, para formar um julgamento de abertura mais robusto.

- Incluir uma estratégia de stop loss para controlar ainda mais o risco.

- Otimizar a estratégia de gerenciamento de posição para um gerenciamento de capital mais científico.

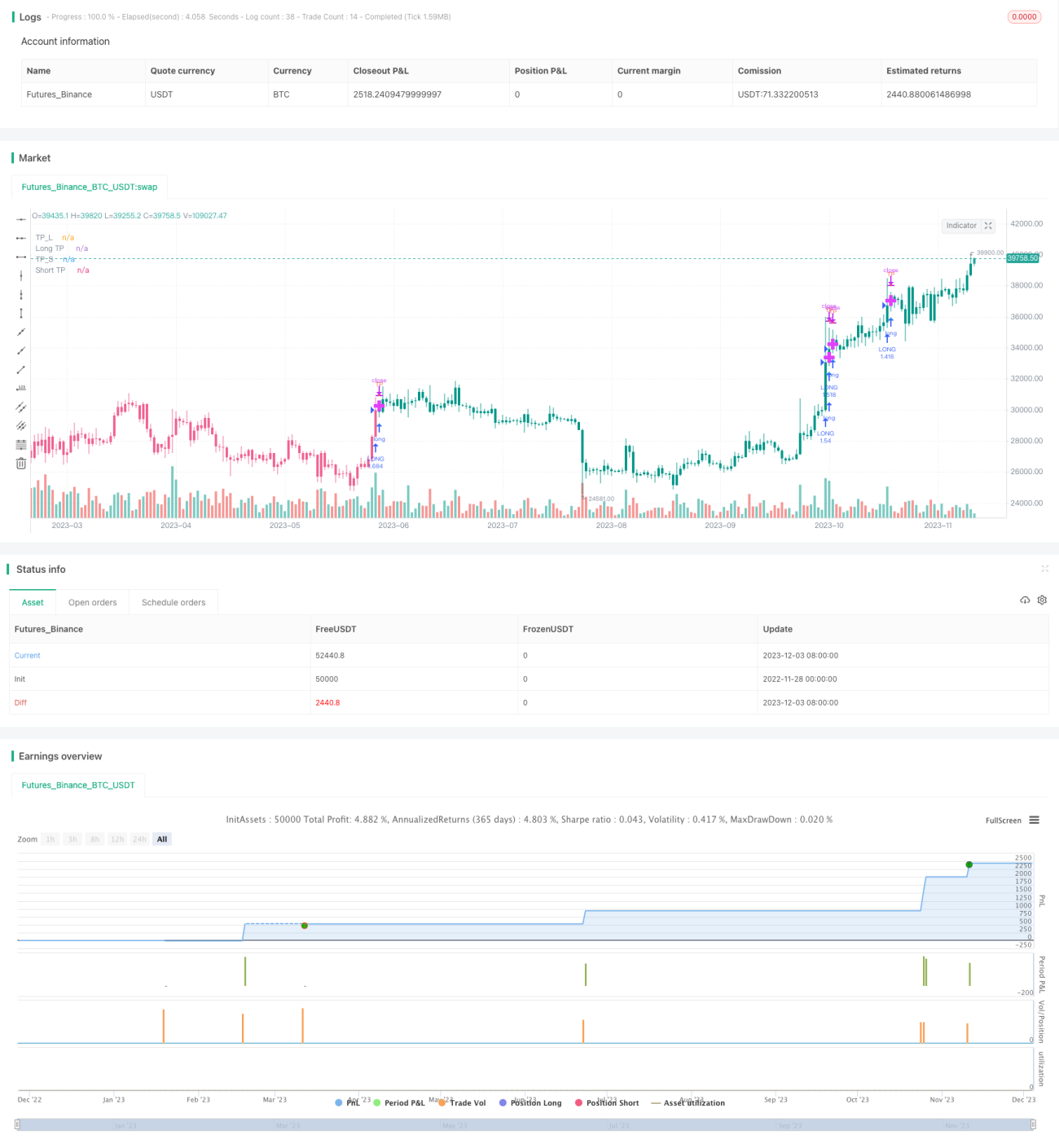

Resumo

Esta estratégia considera de forma abrangente a direção da tendência de preço, a força da tendência e as informações de volume para formar regras de abertura. Em certa medida, evita armadilhas comuns de entrada e possui forte confiabilidade. No entanto, ainda é necessário aprimorar o sistema através de otimização de parâmetros, seleção de indicadores e controle de risco para melhorar ainda mais o desempenho. De modo geral, este framework de estratégia possui grande potencial de expansão e espaço para otimização.

- 1