Estratégia de Reversão de Rompimento de Três ou Quatro Velas

Visão Geral

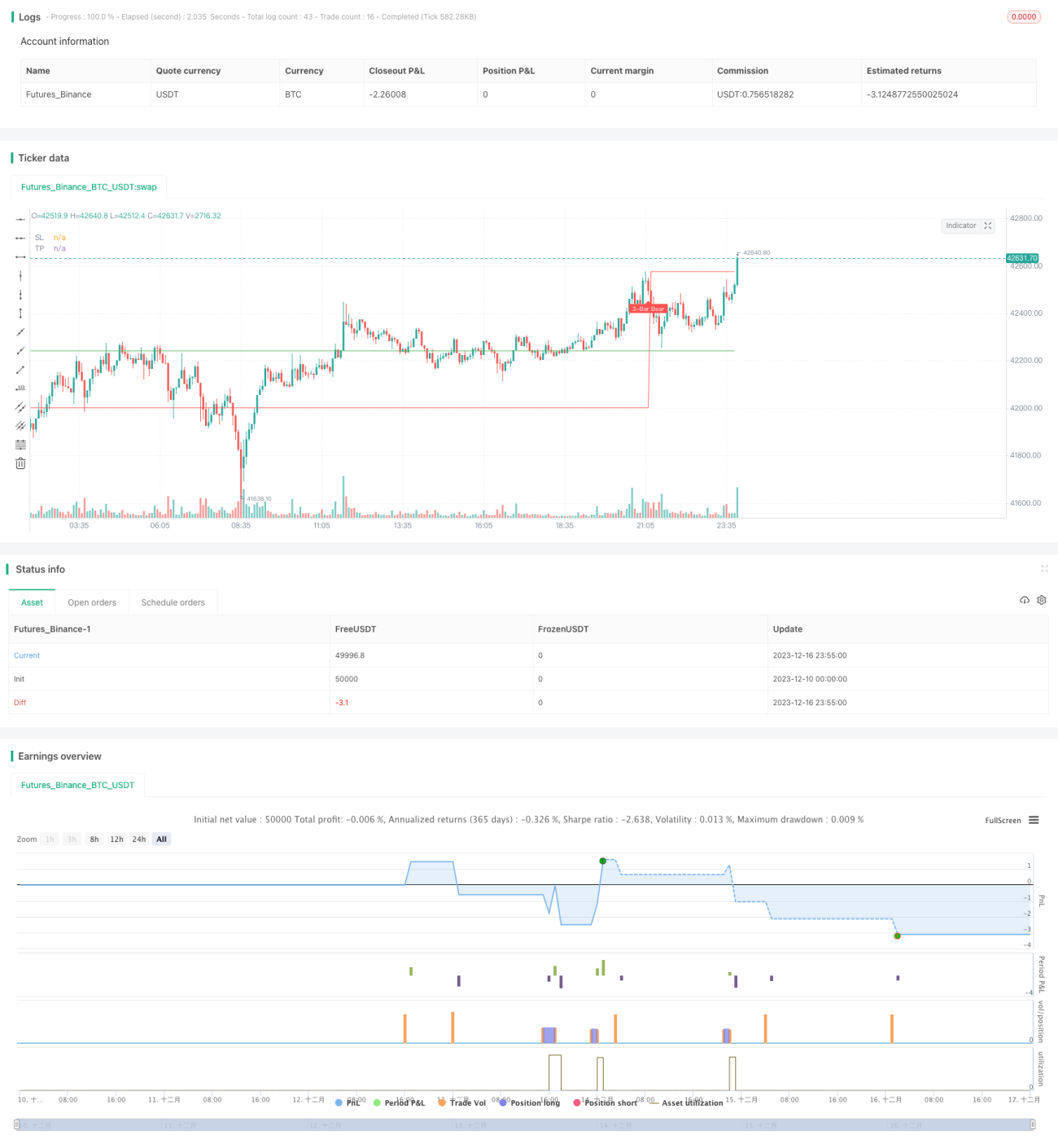

A estratégia de reversão de breakout de três ou quatro velas identifica três ou quatro velas com forte momentum de alta ou baixa e, após algumas velas subsequentes de menor amplitude formarem suporte ou resistência, realiza uma operação contrária quando ocorre uma vela de reversão, sendo uma estratégia de trading de reversão.

Princípio da Estratégia

A lógica central de identificação desta estratégia consiste principalmente nas seguintes partes:

- Identificar a vela de amplitude aumentada (Gap Bar): rompe 1,5 vezes a ATR média, com corpo maior que 0,65. Essa vela é considerada como tendo um forte momentum de alta ou baixa.

- Identificar a vela de consolidação com volume reduzido (Collecting Bar): uma ou duas velas de pequena amplitude que seguem a Gap Bar, com máximas ou mínimas próximas à Gap Bar. Essas velas representam a desaceleração da tendência e a consolidação, formando suporte ou resistência.

- Identificar a vela de sinal de reversão: após as velas de consolidação, se aparecer uma vela cujo corpo rompa a máxima ou mínima das velas anteriores, pode-se considerar um sinal de reversão. Decida se comprar ou vender com base na direção do corpo e abra posição nessa vela.

- Stop loss e take profit: o stop loss é colocado abaixo da mínima ou acima da máxima da vela Gap; o take profit é baseado no ponto de stop loss multiplicado pela relação de lucro/perda configurada.

Análise de Vantagens

Esta estratégia possui as seguintes vantagens principais:

- Utiliza as próprias características das velas para julgar a tendência e os pontos de reversão, sem depender de nenhum indicador, realizando um "indicador embutido".

- As condições de seleção da Gap Bar e da Collecting Bar são rigorosas, permitindo identificar efetivamente as verdadeiras tendências e consolidações.

- O julgamento do sinal de reversão é baseado no corpo da vela, reduzindo a probabilidade de sinais falsos.

- São necessárias apenas 3-4 velas para completar uma operação, com ciclo de tempo curto e alta frequência.

- O stop loss e take profit são definidos claramente, facilitando o controle do drawdown e da relação risco/retorno.

Análise de Riscos

Esta estratégia também apresenta os seguintes riscos:

- Depende da qualidade da configuração dos parâmetros; se os parâmetros forem muito flexíveis, aumentam as chances de sinais falsos e operações perdedoras.

- É facilmente perturbado por falsos rompimentos de alta frequência, não conseguindo filtrar efetivamente todos os sinais falsos.

- Existe o risco de ficar preso em uma posição; se a reversão for insuficiente, pode formar um ajuste, impedindo o stop loss.

- A amplitude do stop loss é relativamente grande, e algumas oportunidades de estar preso podem causar perdas significativas.

Para reduzir esses riscos, é possível otimizar nos seguintes aspectos:

- Otimizar parâmetros para tornar a identificação da Gap Bar e Collecting Bar mais precisa.

- Adicionar filtros, abrindo posição somente após a confirmação adicional da vela de reversão.

- Otimizar o algoritmo de stop loss para que fique mais próximo do preço, tornando as perdas mais controláveis.

Direções de Otimização

Esta estratégia tem as seguintes direções principais de otimização:

- Adicionar filtros compostos para evitar interferência de falsos rompimentos. Por exemplo, adicionar um indicador de volume, considerando sinais de negociação apenas quando o volume estiver aumentado.

- Combinar com indicadores de médias móveis, considerando sinais apenas quando o preço romper médias importantes (como EMA de 20 dias, 60 dias).

- Validação em múltiplos timeframes, abrindo posição apenas quando múltiplos períodos derem sinais simultaneamente.

- Otimizar as condições de take profit, ajustando dinamicamente a relação risco/retorno com base na volatilidade do mercado e na tolerância ao risco.

- Combinar com um sistema de julgamento do estado de alta/baixa do mercado, utilizando a estratégia apenas em ambientes de mercado com tendência.

Resumo

A estratégia de reversão de breakout de três ou quatro velas opera identificando segmentos de tendência de alta qualidade e sinais de reversão. Com ciclo de operação curto e alta frequência, tem potencial para obter retornos excedentes robustos. No entanto, também apresenta certos riscos, exigindo otimização contínua para reduzir riscos e aumentar a estabilidade. No geral, a estratégia utiliza efetivamente as características próprias do perfil do mercado para julgar tendências e pontos de reversão, merecendo mais estudo e aplicação.

/*backtest

start: 2023-12-10 00:00:00

end: 2023-12-17 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Three (3)-Bar and Four (4)-Bar Plays Strategy", shorttitle="Three (3)-Bar and Four (4)-Bar Plays Strategy", overlay=true, calc_on_every_tick=true, currency=currency.USD, default_qty_value=1.0,initial_capital=30000.00,default_qty_type=strategy.percent_of_equity)

frommonth = input(defval = 1, minval = 01, maxval = 12, title = "From Month")- 1