Estratégia de Rastreamento de Momentum entre Múltiplos Períodos

Visão Geral

Esta estratégia combina os indicadores de Reversão 123 e MACD para realizar o acompanhamento de momentum em múltiplos períodos de tempo. A Reversão 123 identifica pontos de reversão de curto prazo, enquanto o MACD avalia a tendência de médio/longo prazo. A combinação de ambos gera sinais de compra/venda ao identificar reversões de curto prazo alinhadas com a tendência de médio/longo prazo.

Princípio da Estratégia

A estratégia é composta por duas partes:

-

Parte da Reversão 123: Quando as duas últimas velas formam uma máxima/mínima e o oscilador estocástico está abaixo/acima de 50, é gerado um sinal de compra/venda.

-

Parte do MACD: Quando a linha rápida cruza acima da linha lenta, é gerado um sinal de compra; quando cruza abaixo, um sinal de venda.

Finalmente, os dois são combinados: o sinal final é emitido apenas quando a Reversão 123 e o MACD geram sinais na mesma direção.

Análise de Vantagens

A estratégia combina reversões de curto prazo com tendências de médio/longo prazo, permitindo capturar movimentos de curto prazo enquanto acompanha a tendência principal, o que resulta em uma maior taxa de acerto. Especialmente em mercados oscilantes, a Reversão 123 pode filtrar parte do ruído, aumentando a estabilidade.

Além disso, ajustando os parâmetros, é possível equilibrar a proporção entre sinais de reversão e sinais de tendência, adaptando-se a diferentes condições de mercado.

Análise de Riscos

A estratégia apresenta certo atraso, especialmente ao usar MACD de período longo, podendo perder movimentos de curto prazo. Além disso, sinais de reversão possuem um grau de aleatoriedade, o que pode resultar em armadilhas.

É possível reduzir o período do MACD ou adicionar um stop loss para controlar o risco.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

-

Ajustar os parâmetros da Reversão 123 para melhorar a eficácia das reversões.

-

Ajustar os parâmetros do MACD para refinar a identificação de tendências.

-

Adicionar outros indicadores auxiliares para filtrar sinais e melhorar o desempenho.

-

Implementar estratégias de stop loss para controlar riscos.

Resumo

Esta estratégia integra múltiplos parâmetros e indicadores técnicos de diferentes períodos de tempo, equilibrando as vantagens do trading de reversão e do trading de tendência por meio do acompanhamento de momentum em múltiplos períodos. Pode ser ajustada através de parâmetros para equilibrar o desempenho e pode ser otimizada com a introdução de mais indicadores ou stops, representando uma abordagem de estratégia com grande potencial.

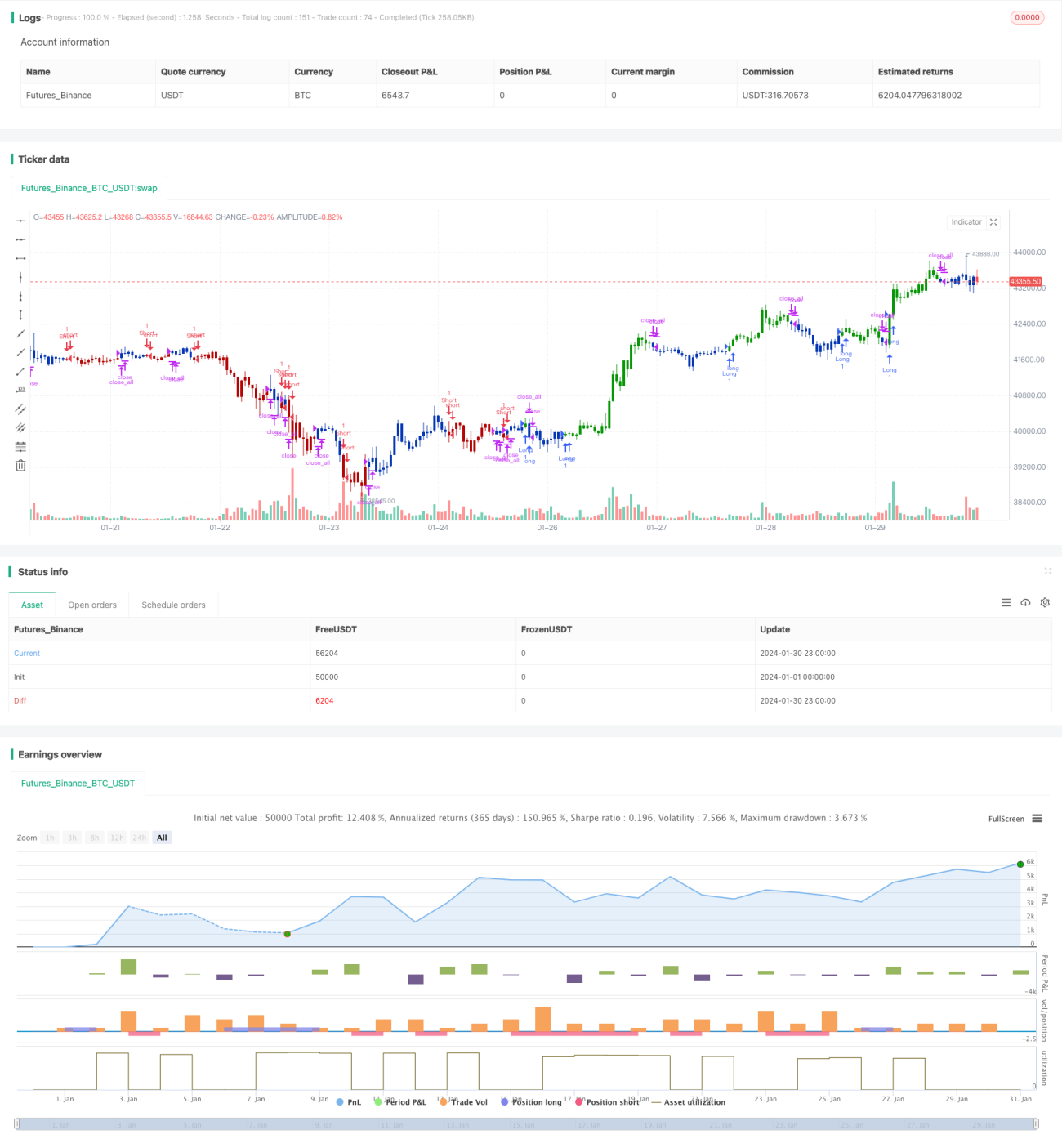

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 28/01/2021

// This is combo strategies for get a cumulative signal. - 1