EMA/ADX/VOL - Sát thủ tiền điện tử

Sử dụng hệ thống đường trung bình động EMA để xác định hướng xu hướng, chỉ báo ADX để đánh giá sức mạnh xu hướng, kết hợp với bộ lọc khối lượng giao dịch để vào lệnh trong chiến lược giao dịch định lượng

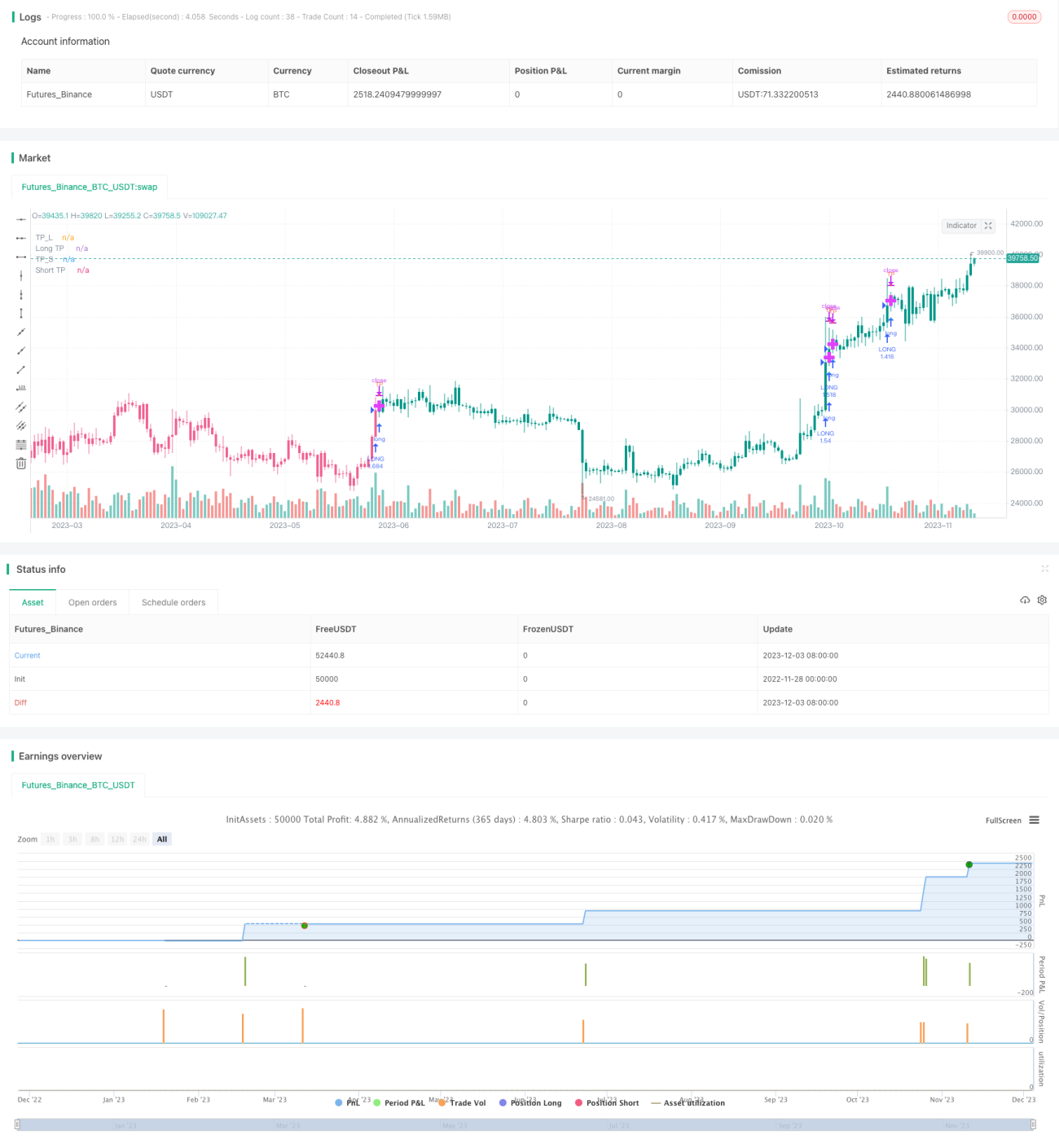

Nguyên lý

Chiến lược này trước tiên sử dụng 5 đường EMA với chu kỳ khác nhau để xác định hướng của xu hướng giá. Khi cả 5 đường EMA đều tăng, xác định xu hướng tăng hình thành; khi cả 5 đường EMA đều giảm, xác định xu hướng giảm hình thành.

Sau đó, sử dụng chỉ báo ADX để đánh giá sức mạnh của xu hướng. Khi đường DI+ cao hơn đường DI- và giá trị ADX vượt quá ngưỡng thiết lập, xác định thị trường tăng mạnh; khi đường DI- cao hơn đường DI+ và giá trị ADX vượt quá ngưỡng thiết lập, xác định thị trường giảm.

Đồng thời, sử dụng sự bùng nổ khối lượng giao dịch để xác nhận thêm, yêu cầu khối lượng giao dịch của nến hiện tại lớn hơn một bội số nhất định của khối lượng trung bình trong một chu kỳ, nhằm tránh vào lệnh sai ở những vị trí có khối lượng thấp.

Kết hợp đánh giá tổng hợp về hướng xu hướng, sức mạnh xu hướng và khối lượng giao dịch, hình thành logic mở lệnh mua và bán của chiến lược này.

Ưu điểm

-

Sử dụng hệ thống đường EMA để xác định hướng xu hướng, đáng tin cậy hơn so với chỉ dùng một đường EMA đơn lẻ.

-

Nhờ chỉ báo ADX đánh giá sức mạnh xu hướng, tránh vào lệnh sai khi không có xu hướng rõ ràng.

-

Cơ chế lọc khối lượng giao dịch, đảm bảo có đủ khối lượng hỗ trợ, tăng độ tin cậy của chiến lược.

-

Đánh giá tổng hợp nhiều điều kiện, tín hiệu vào lệnh chính xác và đáng tin cậy hơn.

-

Chiến lược có nhiều tham số, có thể liên tục tối ưu hóa để nâng cao hiệu quả.

Rủi ro và giải pháp

-

Trong thị trường đi ngang, các đánh giá từ EMA, ADX có thể phát ra tín hiệu sai, dẫn đến thua lỗ không cần thiết. Có thể điều chỉnh tham số phù hợp hoặc thêm các chỉ báo khác để hỗ trợ đánh giá.

-

Điều kiện lọc khối lượng giao dịch quá nghiêm ngặt có thể bỏ lỡ cơ hội thị trường. Có thể giảm nhẹ tham số lọc khối lượng.

-

Tần suất giao dịch của chiến lược có thể khá cao, cần chú ý quản lý vốn và kiểm soát quy mô lệnh hợp lý.

Hướng tối ưu

-

Thử nghiệm các tổ hợp tham số khác nhau để tìm ra tham số tối ưu, nâng cao hiệu quả chiến lược.

-

Thêm các chỉ báo khác như MACD, KDJ kết hợp với EMA và ADX để hình thành đánh giá vào lệnh tổng hợp mạnh mẽ hơn.

-

Thêm chiến lược cắt lỗ để kiểm soát rủi ro tốt hơn.

-

Tối ưu hóa chiến lược quản lý vị thế, thực hiện quản lý vốn khoa học hơn.

Tổng kết

Chiến lược này xem xét tổng hợp hướng xu hướng giá, sức mạnh xu hướng và thông tin khối lượng giao dịch để hình thành quy tắc vào lệnh, ở một mức độ nhất định tránh được các bẫy phổ biến và có độ tin cậy cao. Tuy nhiên, vẫn cần tiếp tục hoàn thiện hệ thống chiến lược thông qua tối ưu hóa tham số, lựa chọn chỉ báo ưu việt và quản lý rủi ro để nâng cao hiệu quả hơn nữa. Nhìn chung, khung chiến lược này có tiềm năng mở rộng và không gian tối ưu rất lớn.

- 1