Chiến lược giao dịch định lượng dựa trên số ngẫu nhiên

Tổng quan

Ý tưởng cốt lõi của chiến lược này là sử dụng số ngẫu nhiên để mô phỏng các sự kiện xác suất như tung đồng xu hay xúc xắc, dựa trên kết quả của sự kiện để quyết định mở vị thế mua (long) hoặc bán (short), từ đó thực hiện giao dịch ngẫu nhiên. Chiến lược giao dịch này có thể dùng để kiểm tra mô phỏng hoặc làm khung nền tảng cho việc phát triển các chiến lược phức tạp hơn.

Nguyên lý chiến lược

-

Sử dụng biến

flipđể mô phỏng sự kiện ngẫu nhiên, dựa trên độ lớn của số ngẫu nhiêncoinLabelđể quyết định mua hay bán. -

Sử dụng

riskvàratiođể thiết lập các mức cắt lỗ và chốt lời. -

Kích hoạt tín hiệu giao dịch tiếp theo một cách ngẫu nhiên theo số chu kỳ tối đa đã thiết lập.

-

Sử dụng biến

plotBoxđể kiểm soát việc hiển thị hộp đóng vị thế. -

Các biến

stoppedOutvàtakeProfitđược dùng để phát hiện cắt lỗ hoặc chốt lời. -

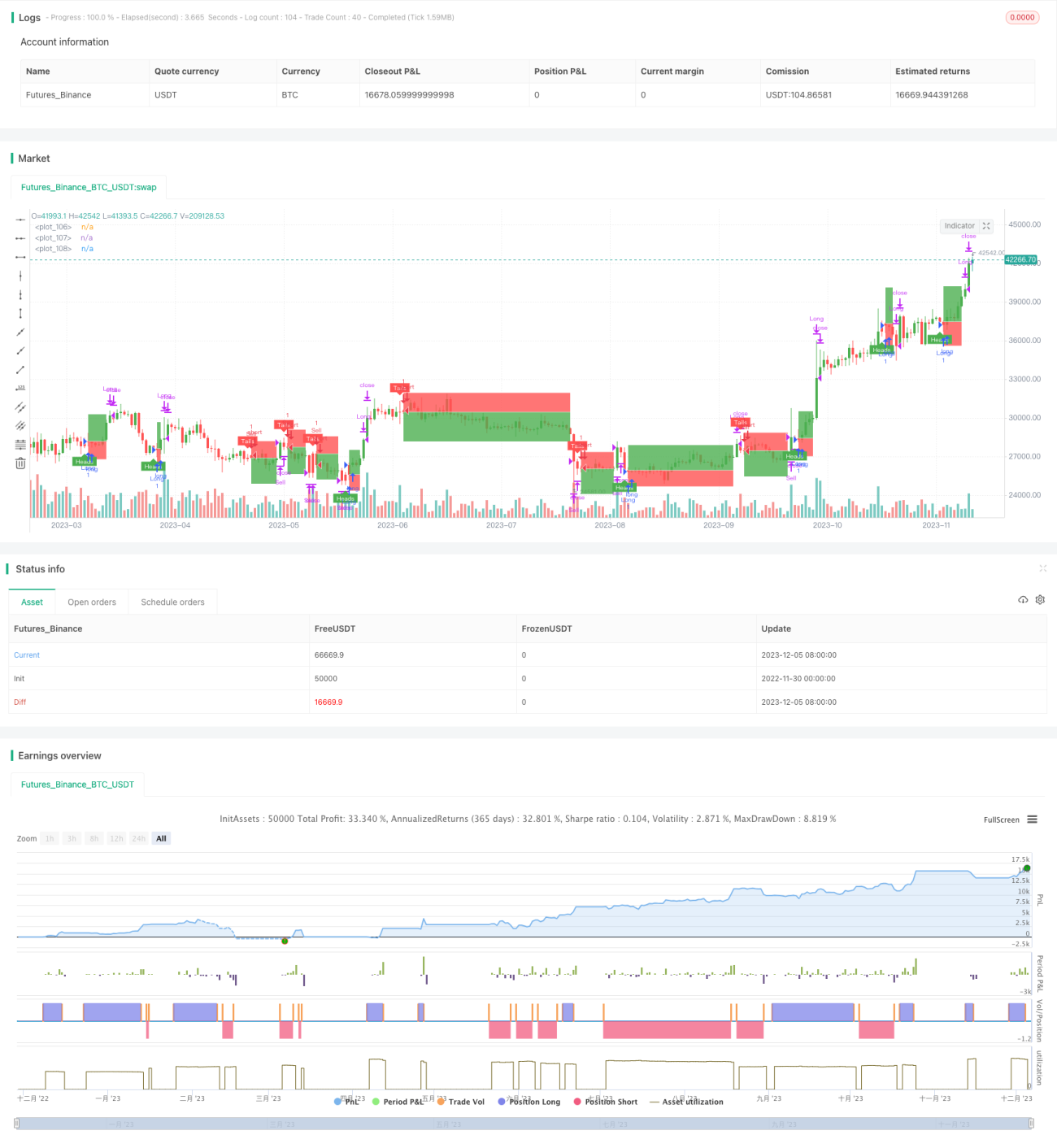

Cung cấp chức năng backtest để kiểm tra hiệu suất của chiến lược.

Phân tích ưu điểm

-

Cấu trúc mã rõ ràng, dễ hiểu và dễ phát triển mở rộng.

-

Giao diện người dùng thân thiện, tất cả các tham số có thể điều chỉnh qua giao diện đồ họa.

-

Tính ngẫu nhiên cao, không bị ảnh hưởng bởi biến động thị trường, độ tin cậy cao.

-

Có thể tối ưu hóa tham số để đạt tỷ suất lợi nhuận tốt hơn.

-

Có thể dùng để trình diễn hoặc kiểm thử các chiến lược khác.

Phân tích rủi ro

-

Giao dịch ngẫu nhiên không thể đánh giá thị trường, tồn tại rủi ro lợi nhuận nhất định.

-

Không thể xác định bộ tham số tối ưu, cần kiểm tra nhiều lần.

-

Tồn tại rủi ro tương quan siêu cao do tín hiệu ngẫu nhiên quá dày đặc.

-

Nên kết hợp cơ chế cắt lỗ/chốt lời để kiểm soát rủi ro.

-

Có thể giảm rủi ro bằng cách kéo dài khoảng cách giao dịch hợp lý.

Hướng tối ưu

-

Kết hợp các yếu tố phức tạp hơn để tạo tín hiệu ngẫu nhiên.

-

Thêm các sản phẩm giao dịch, mở rộng phạm vi kiểm tra.

-

Tối ưu tương tác UI, thêm chức năng kiểm soát chiến lược.

-

Cung cấp thêm nhiều công cụ và chỉ số kiểm tra để thuận tiện cho việc tối ưu tham số.

-

Có thể được sử dụng như một thành phần tín hiệu giao dịch hoặc cắt lỗ/chốt lời tích hợp vào các chiến lược khác.

Kết luận

Chiến lược này có khung tổng thể hoàn chỉnh, dựa trên các sự kiện ngẫu nhiên để tạo tín hiệu giao dịch, độ tin cậy khá cao. Đồng thời cung cấp các chức năng điều chỉnh tham số, backtest và vẽ biểu đồ. Có thể dùng để kiểm thử việc phát triển chiến lược cho người mới, cũng như làm mô-đun cơ sở cho các chiến lược khác. Với việc tối ưu phù hợp, có thể làm cho hiệu suất chiến lược nổi bật hơn.

- 1