トレンド信頼度に基づくトレンドフォロー戦略

概要

本戦略の主なアイデアは、可能な限り正確なトレンドフォロー戦略を実現することです。過去一定期間の終値の「信頼度」を計算し、現在の線形トレンドの継続可能性を判断します。この戦略は、信頼度が一定の水準を超えると、進行中の線形トレンドが継続する可能性が高いと仮定します。

戦略の原理

この戦略は、通常の線形回帰法を用いて過去N本の終値の線形フィットを計算し、線形フィットの傾きkと終値との偏差の標準偏差σを取得します。そして、トレンド信頼度をk/σと定義します。

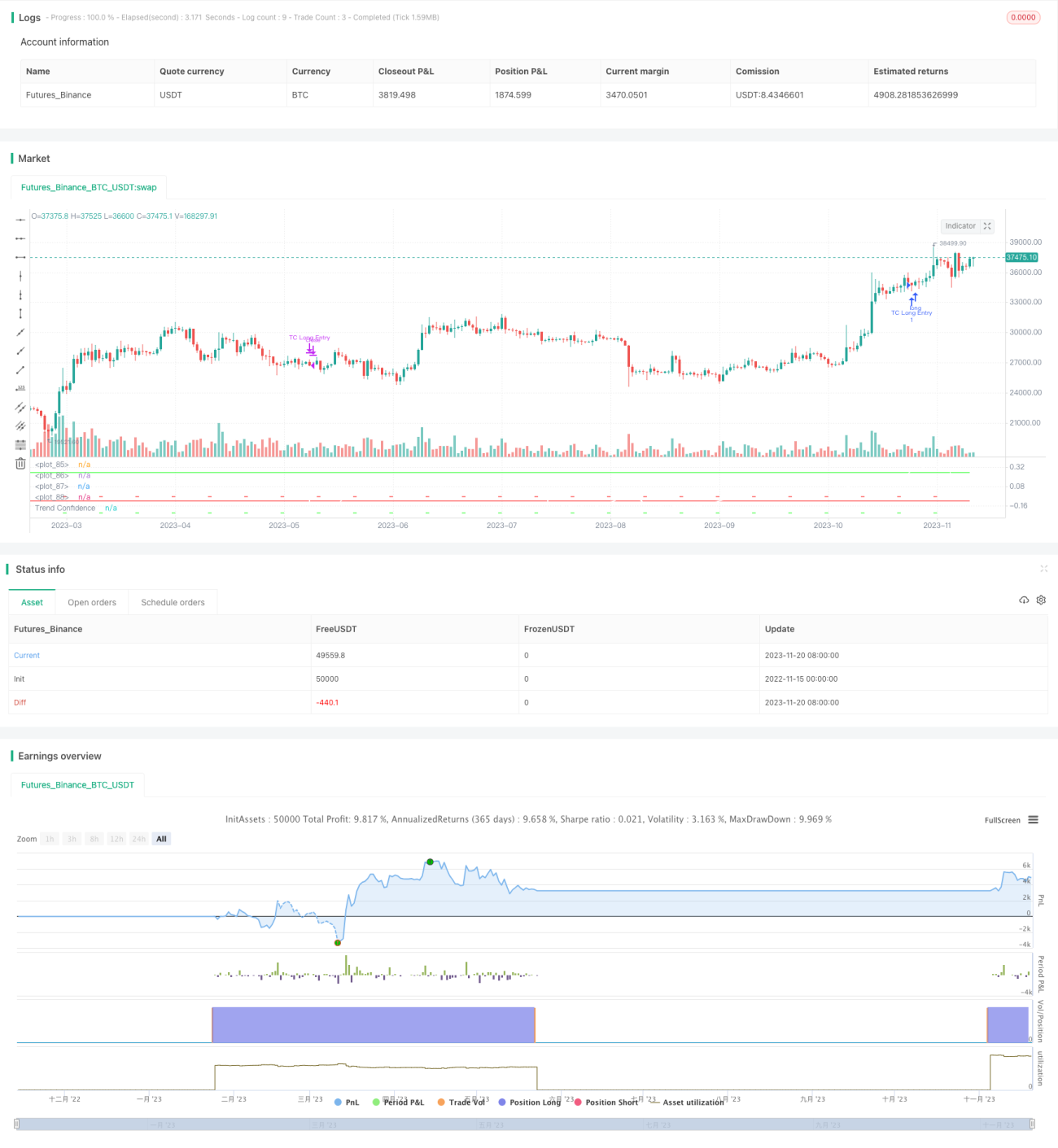

トレンド信頼度が「ロングエントリー」閾値を超えた場合に買い建て、「ロング決済」閾値まで下落した場合に決済します。同様に、トレンド信頼度が「ショートエントリー」閾値を下回った場合に売り建て、「ショート決済」閾値を超えた場合に決済します。

これにより、明確な線形トレンドに従わない荒い価格変動に伴うシグナルをフィルタリングできます。

優位性分析

この戦略は、トレンドフォローと統計学の線形回帰手法を組み合わせており、短期的な価格変動を追いかけるのを避け、長期的なトレンドにのみ追随することで、取引頻度を低く抑え、勝率を高めることができます。

この戦略はパラメータ調整の余地が大きく、パラメータを調整することで異なる銘柄や時間足に適用でき、優れた汎化性を実現できます。

リスク分析

この戦略には、逆張りで損失が発生するリスクがあります。価格が明確にトレンド転換した場合、戦略は大きな損失を出す可能性があります。また、パラメータ設定が不適切だと、過剰な取引や優れた取引機会を逃すことにつながります。

ストップロスを設定することで損失リスクをコントロールできます。同時に、パラメータ選択を慎重に評価し、過度な最適化を避ける必要があります。

最適化の方向性

この戦略は以下の点でさらなる最適化が可能です:

-

利益確定・損失限定のロジックを追加して、利益確定とリスクコントロールを実現する

-

パラメータの自己適応最適化モジュールを追加し、パラメータを動的に調整可能にする

-

機械学習モデルを追加してトレンド転換点を判断し、戦略の勝率をさらに向上させる

-

異なる銘柄や時間足への適合性を試し、汎化能力を高める

まとめ

本戦略は全体的に、長期的なトレンドに基づきリスクをコントロールする定量戦略です。トレンドフォローと線形回帰手法を融合し、ノイズの多い取引シグナルをフィルタリングできます。パラメータ調整により、様々な銘柄や期間にうまく適応でき、重点的に研究し改善する価値のある有効な戦略です。

/*backtest

start: 2022-11-15 00:00:00

end: 2023-11-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © carefulCamel61097

// ################################################################################################- 1