ダブルEMAゴールデンクロス取引戦略

概要

本戦略は、デュアルEMAのゴールデンクロス、標準化ATRノイズフィルター、ADXトレンド指標を組み合わせ、トレーダーにより信頼性の高い買いシグナルを提供することを目的としています。この戦略は複数の指標を統合して偽のシグナルをフィルタリングし、より信頼性の高い取引機会を特定します。

戦略の原理

本戦略では、8期間と20期間のEMAを使用してデュアルEMAゴールデンクロスシステムを構築します。短期EMAが長期EMAを上抜けたときに買いシグナルを生成します。

さらに、戦略は複数の補助指標を設定してフィルタリングを行います:

- 14期間のATRを標準化処理し、市場における小さすぎる価格変動をフィルタリングします。

- 14期間のADXを使用してトレンドの強さを識別します。強いトレンドにある場合のみ取引シグナルを検討します。

- 14期間の出来高SMAを使用して、出来高が少ない時点をフィルタリングします。

- 4/14期間のスーパートレンド指標を使用して、市場の方向性(強気/弱気)を判断します。

トレンド方向、ATR標準化値、ADX値、出来高条件を満たした後、EMAゴールデンクロスが最終的に買いシグナルをトリガーします。

戦略の利点

-

複数指標の組み合わせにより、信頼性が高い

本戦略はEMA、ATR、ADX、スーパートレンドなどの複数の指標を統合し、指標の補完により強力なシグナルフィルターシステムを形成しているため、信頼性が高いです。

-

パラメータ調整の余地が大きい

ATR標準化値の閾値、ADX閾値、保有期間などのパラメータは実際の状況に応じて最適化・調整可能であり、戦略の柔軟性が高いです。

-

強気・弱気市場の区別が可能

スーパートレンド指標で強気・弱気市場を判断し、それぞれ異なるパラメータ基準を適用することで機会損失を防ぎます。

戦略のリスク

-

パラメータ最適化が困難

戦略のパラメータ組み合わせが複雑であり、最適化が難しく、最適なパラメータを見つけるには大量のバックテストが必要です。

-

指標の誤発動リスク

多重フィルタリングがあるものの、指標には本質的に遅延性があるため、誤発動のリスクが残ります。損切りの理論を十分に考慮する必要があります。

-

取引頻度が低い

複数の指標やフィルターの影響により、戦略の取引頻度は低くなり、長期間取引がない可能性があります。

戦略の最適化方向

-

パラメータ組み合わせの最適化

大量のバックテストデータを通じて、指標パラメータの最適な組み合わせを見つけます。

-

機械学習の導入

大量の過去データに基づき、機械学習アルゴリズムを活用して戦略パラメータを自動最適化し、戦略の適応性を実現します。

-

より多くの市場要因の考慮

より多くの指標を組み合わせて市場構造やセンチメントなどの要因を判断し、戦略の多様性を豊かにします。

まとめ

本戦略は、トレンド、ボラティリティ、出来高・価格要因を総合的に考慮し、複数の指標によるフィルタリングとパラメータ調整により取引体系を形成しています。総合的に見ると、本戦略の信頼性は高く、パラメータ組み合わせとモデリング手法のさらなる最適化により、取引効率を向上させることができます。

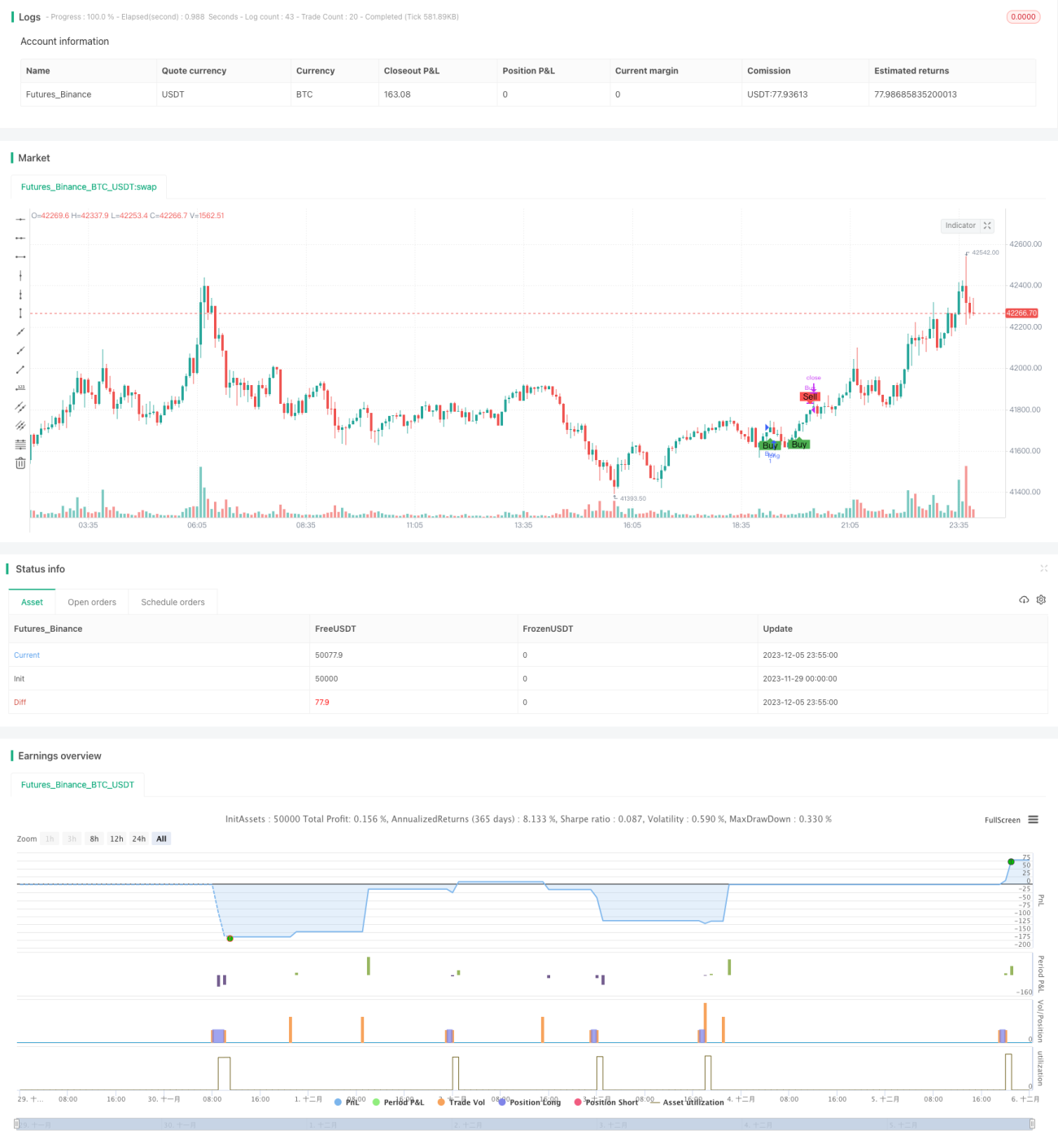

/*backtest

start: 2023-11-29 00:00:00

end: 2023-12-06 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//Description:

//This strategy is a refactored version of an EMA cross strategy with a normalized ATR filter and ADX control.

//It aims to provide traders with signals for long positions based on market conditions defined by various indicators.- 1