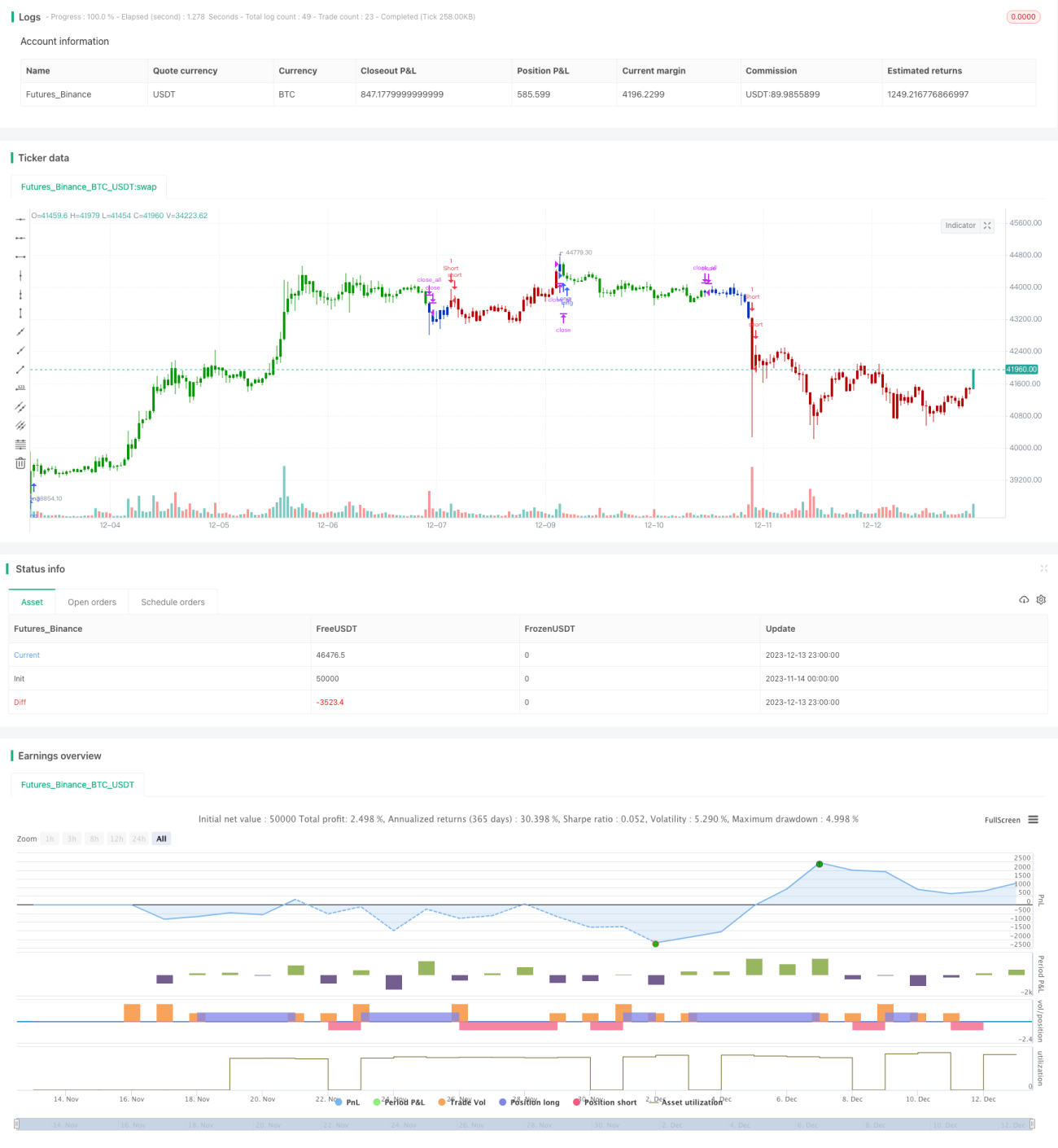

概要

ダブルリバーサル均衡戦略は、リバーサル戦略とフィルタ分解戦略を組み合わせた複合戦略です。この戦略はまず123リバーサルシステムで取引シグナルを生成し、その後経験モード分解(EMD)でフィルタリング処理を施し、両方の取引シグナルを統合することで高い勝率を実現します。

戦略の原理

123リバーサルシステム

123リバーサルシステムは、Ulf Jensenの著書『How I Tripled My Money in the Futures Market』に由来します。この部分の戦略はリバーサル型に分類されます。終値が前日の終値を2営業日連続で上回り、かつ9日スローKラインが50未満の場合に買いシグナルが発生し、終値が前日の終値を2営業日連続で下回り、かつ9日ファーストKラインが50超の場合に売りシグナルが発生します。

経験モード分解(EMD)

経験モード分解(EMD)は適応型のデータ解析手法です。データに含まれる異なる周波数成分を効果的に分離し、データの長期トレンドを抽出できます。ここでは長さを20、デルタを0.5、フラクションを0.1に設定し、価格の異なる周波数成分に基づいて取引シグナルを生成します。

シグナルの統合

ダブルリバーサル均衡戦略は、123リバーサルシステムと経験モード分解で生成された取引シグナルを統合し、両方のシグナルが一致した場合にエントリーを確定します。これにより戦略の勝率を向上させます。

優位性の分析

ダブルリバーサル均衡戦略は、リバーサル戦略とデジタル信号処理技術を組み合わせ、異なるモデルの強みを活用します。リバーサルシステムは短期の反転機会を捉え、経験モード分解は長期トレンドを捉え、両者を併用することで戦略の安定性が向上します。

また、この戦略は123パターンを導入することで、望ましくないリバーサルによる損失を回避できます。経験モード分解では適切なパラメータを設定することで、ノイズの一部をフィルタリングし、誤ったシグナルを削減できます。

リスク分析

ダブルリバーサル均衡戦略の最大のリスクはリバーサルの失敗です。123パターンの導入でその確率を減らせますが、リバーサル取引には本質的に大きな不確実性が伴うことを忘れてはなりません。また、経験モード分解は適応型フィルタリング手法ですが、極端な相場では機能しなくなる可能性もあります。

これらのリスクを管理するために、リバーサルのパラメータを適宜調整し、リバーサルシグナルをより信頼性の高いものにする必要があります。また、経験モード分解の代わりに異なるフィルタリング手法をテストし、より効果的なフィルタリングが得られるか検討することも有効です。さらに、少量の取引を維持し、1回の損失を過大にしないことも必要です。

最適化の方向性

この戦略は以下の点から最適化が可能です。

-

リバーサルシステムの異なるパラメータをテストし、最適なパラメータの組合せを確定する

-

ウェーブレット変換やヒルベルト変換など、異なるデジタルフィルタリング手法を試す

-

ストップロス戦略を追加し、1回の損失を管理する

-

他のインジケーターと組み合わせ、取引方向の正確性と信頼性を高める

-

資金管理を最適化し、最適な取引サイズ比率を確定する

まとめ

ダブルリバーサル均衡戦略は、リバーサル戦略とデジタル信号処理技術の利点を総合的に活用しています。適切なパラメータ設定によりリスクを管理し、安定した取引を実現します。この戦略は汎用性と拡張性が高く、推奨できる取引戦略です。

/*backtest

start: 2023-11-14 00:00:00

end: 2023-12-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 30/06/2020

// This is combo strategies for get a cumulative signal. - 1