概要

慣性指標取引戦略は、相対変動指数(RVI)に基づくトレンドフォロー型のアルゴリズム取引戦略です。この戦略は、証券のRVIを計算することで、市場、株式、または通貨ペアのモメンタムとトレンドを測定します。これにより、長期的なトレンドの方向性を判断し、取引ポジションを構築するためのシグナルとします。

戦略の原理

この戦略の中核指標は慣性指標(Inertia Indicator)であり、0から100の間の値を取ります。指標が50を超えると正の慣性、50未満だと負の慣性を示します。慣性値が継続して50を超える限り、長期的な上昇トレンドと判断でき、逆に50未満であれば下降トレンドと判断します。

指標の計算プロセスは以下の通りです。

- 指定期間内の株価終値の標準偏差StdDevを計算する

- 本日の終値と前日の終値を比較し、上昇変動uと下降変動dを計算する

- uとdを計算し平滑化して、指標nUとnDを得る

- 相対変動指数nRVI = 100 * nU / (nU + nD)を計算する

- nRVIに対して指数移動平均を行い、最終的な慣性値nResを得る

nResが50より大きいと正の慣性を示し、買いシグナルが発生します。50未満だと負の慣性を示し、売りシグナルが発生します。

優位性分析

この戦略の最大の利点は、相場の流れに乗り、市場トレンドを捉え、レンジ相場での頻繁なポジション開設を避けられる点です。また、指標の計算が比較的単純で、計算リソースへの要求が低く、アルゴリズム取引に適しています。

リスク分析

この戦略の最大のリスクは、指標自体に遅延が存在し、転換点を100%捕らえることができない点です。これにより、最適なエントリーのタイミングを逃す可能性があります。また、指標のパラメータ設定も戦略のパフォーマンスに影響を与えるため、最適なパラメータを見つけるために大量のバックテストが必要です。

リスクを軽減するためには、他のテクニカル指標やファンダメンタル指標と組み合わせて使用し、より多くの要因でポジション開設を決定することが考えられます。同時に、1回の取引あたりのポジションサイズを管理する必要があります。

最適化の方向性

この戦略は以下の観点から最適化できます。

- パラメータ最適化。期間パラメータと平滑化パラメータの設定を変更し、最適なパラメータの組み合わせを見つける。

- 他の指標との組み合わせ。移動平均線やRSIなどの指標と併用し、より多くの要因で判断する。

- 動的なポジション管理。市場状況や指標の値に応じて、各取引のポジションサイズを動的に調整する。

- 自動ストップロス戦略。ストップロスの位置を設定し、1回の取引の最大損失を効果的に制御する。

まとめ

慣性指標取引戦略は、全体的に比較的シンプルで信頼性の高いトレンドフォロー戦略です。慣性指標を用いて価格トレンドの方向性を判断し、それに沿って取引ポジションを構築します。パラメータ最適化や指標の組み合わせなどにより戦略効果をさらに高めることができ、定量取引に適したアルゴリズム戦略です。

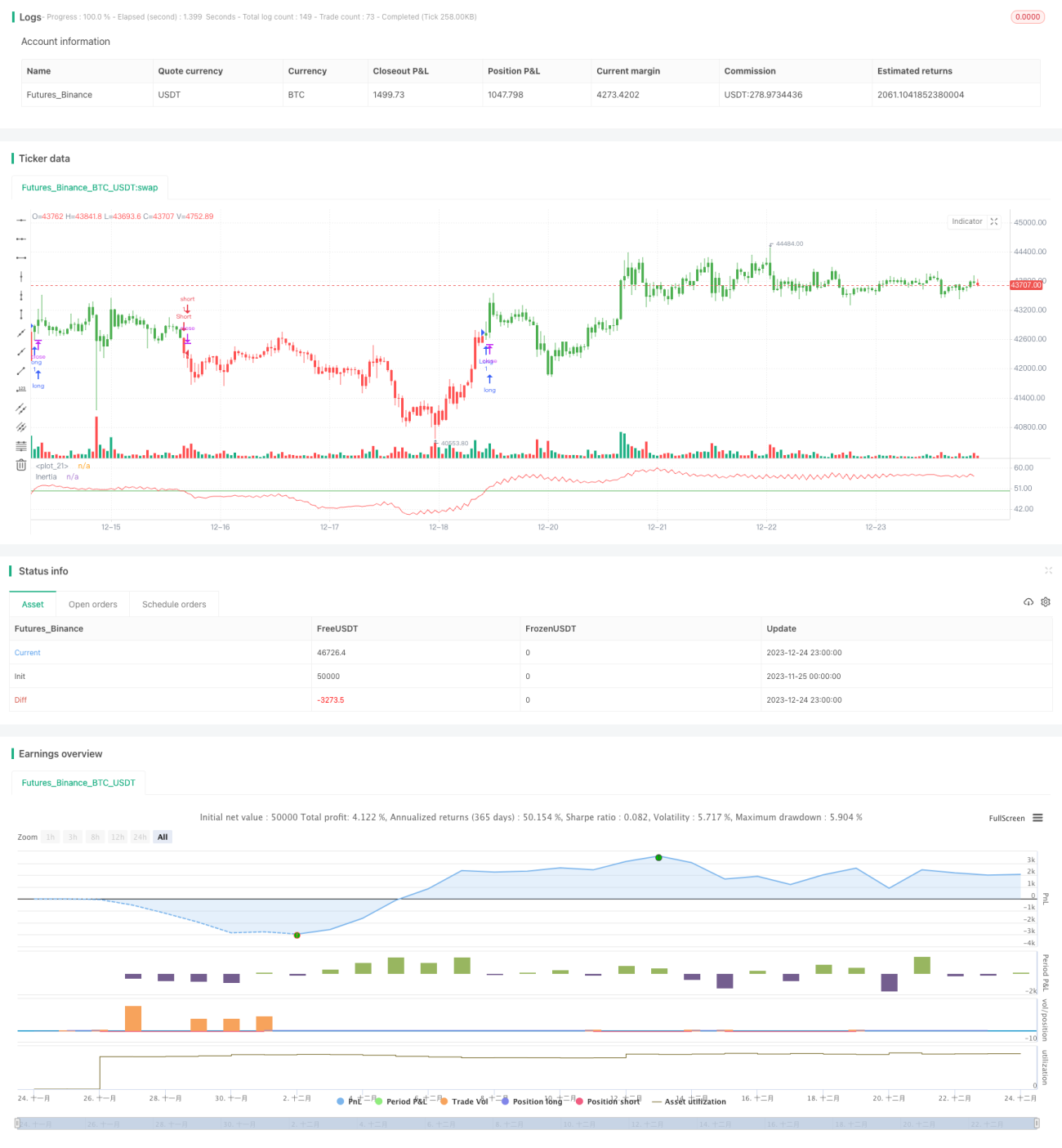

/*backtest

start: 2023-11-25 00:00:00

end: 2023-12-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 23/05/2017

// The inertia indicator measures the market, stock or currency pair momentum and - 1