이중 EMA 골든 크로스 거래 전략

개요

본 전략은 이중 EMA 골든 크로스, 표준화된 ATR 노이즈 필터 및 ADX 추세 지표를 결합하여 트레이더에게 더 신뢰할 수 있는 매수 신호를 제공하는 것을 목표로 합니다. 이 전략은 여러 지표를 종합하여 허위 신호를 필터링하고 더 신뢰할 수 있는 거래 기회를 식별합니다.

전략 원리

이 전략은 8주기와 20주기의 EMA를 사용하여 이중 EMA 골든 크로스 시스템을 구축합니다. 단기 EMA가 장기 EMA를 상향 돌파할 때 매수 신호가 생성됩니다.

또한 전략은 여러 보조 지표를 설정하여 필터링합니다:

- 14주기 ATR, 표준화 처리를 통해 시장에서 너무 작은 가격 변동을 필터링합니다.

- 14주기 ADX, 추세의 강도를 식별하는 데 사용됩니다. 강한 추세에서만 거래 신호를 고려합니다.

- 14주기 거래량 SMA, 거래량이 적은 시점을 필터링합니다.

- 4/14주기 Super Trend 지표, 매수/매도 시장 방향을 판단합니다.

추세 방향, ATR 표준화 값, ADX 값 및 거래량 조건이 충족된 후에야 EMA 골든 크로스가 최종적으로 매수 신호를 트리거합니다.

전략 장점

-

다중 지표 조합, 신뢰성 높음

이 전략은 EMA, ATR, ADX, Super Trend 등 여러 지표를 통합하여 지표 상호 보완을 통해 강력한 신호 필터링 시스템을 형성하므로 신뢰성이 높습니다.

-

매개변수 조정 가능성 큼

ATR 표준화 값 임계값, ADX 임계값, 보유 기간 등 매개변수는 실제 상황에 따라 최적화 및 조정이 가능하여 전략의 유연성이 높습니다.

-

매수/매도 시장 구분 가능

Super Trend 지표를 통해 매수/매도 시장을 판단하고, 각 시장에 대해 다른 매개변수 기준을 사용하여 기회를 놓치지 않도록 합니다.

전략 위험

-

매개변수 최적화 난이도 높음

전략 매개변수 조합이 복잡하여 최적화가 어렵고, 최적의 매개변수를 찾기 위해 많은 백테스트가 필요합니다.

-

지표 오발동 위험

여러 필터가 있음에도 불구하고 지표 본질적으로 지연성이 있기 때문에 오발동 위험이 있습니다. 손절매 이론을 충분히 고려해야 합니다.

-

거래 빈도 낮음

여러 지표와 필터의 영향으로 전략의 거래 빈도가 낮아질 수 있으며, 장기간 거래가 없을 수도 있습니다.

전략 최적화 방향

-

매개변수 조합 최적화

많은 백테스트 데이터를 통해 지표 매개변수의 최적 조합을 찾습니다.

-

머신러닝 추가

많은 과거 데이터를 기반으로 머신러닝 알고리즘을 사용하여 전략 매개변수를 자동으로 최적화하여 전략의 적응성을 구현합니다.

-

더 많은 시장 요소 고려

더 많은 지표를 결합하여 시장 구조, 심리 등의 요소를 판단하여 전략의 다양성을 풍부하게 합니다.

요약

본 전략은 추세, 변동성 및 거래량-가격 요소를 종합적으로 고려하여 다중 지표 필터링과 매개변수 조정을 통해 거래 시스템을 형성합니다. 종합적으로 볼 때, 이 전략은 신뢰성이 높으며, 매개변수 조합과 모델링 방식을 추가로 최적화하여 전략의 거래 효율성을 향상시킬 수 있습니다.

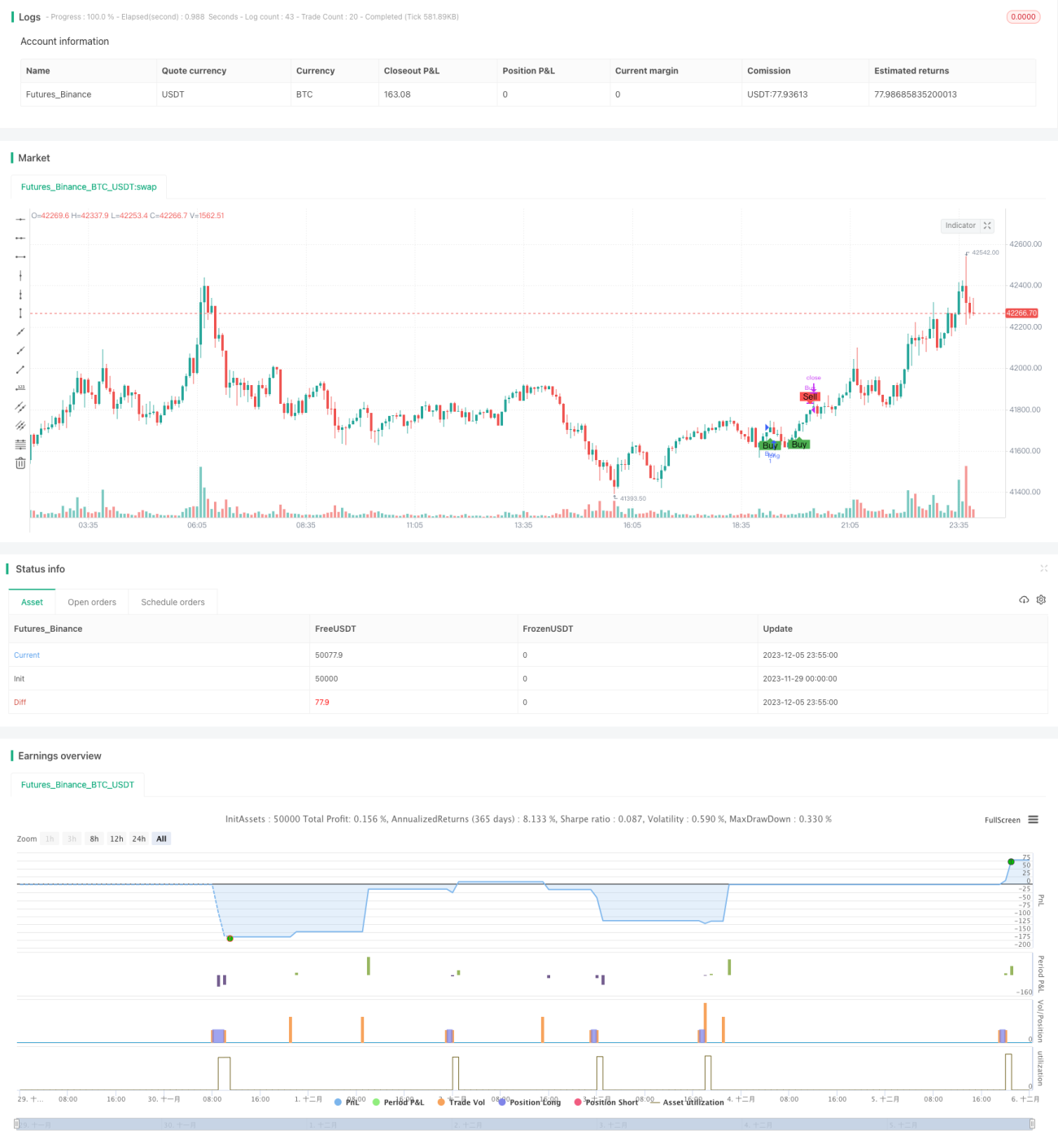

/*backtest

start: 2023-11-29 00:00:00

end: 2023-12-06 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//Description:

//This strategy is a refactored version of an EMA cross strategy with a normalized ATR filter and ADX control.

//It aims to provide traders with signals for long positions based on market conditions defined by various indicators.- 1