Strategi Dagangan Persilangan Emas Dwi EMA

Gambaran Keseluruhan

Strategi ini menggabungkan persilangan emas dua EMA, penapis hingar ATR yang dinormalisasikan dan indikator arah ADX, bertujuan memberikan isyarat beli yang lebih boleh dipercayai kepada pedagang. Strategi ini menapis isyarat palsu melalui gabungan pelbagai indikator untuk mengenal pasti peluang dagangan yang lebih boleh dipercayai.

Prinsip Strategi

Strategi ini menggunakan EMA 8 kitaran dan 20 kitaran untuk membina sistem persilangan emas dua EMA. Isyarat beli dijana apabila EMA jangka pendek melintasi ke atas EMA jangka panjang.

Selain itu, strategi ini juga menetapkan beberapa indikator tambahan untuk penapisan:

-

ATR 14 kitaran, yang dinormalisasikan untuk menapis pergerakan harga yang terlalu kecil dalam pasaran.

-

ADX 14 kitaran, digunakan untuk mengenal pasti kekuatan arah aliran. Isyarat dagangan hanya dipertimbangkan dalam arah aliran yang kukuh.

-

SMA volum 14 kitaran, menapis titik masa dengan volum yang rendah.

-

Indikator Super Trend 4/14 kitaran, untuk menentukan arah pasaran bull atau bear.

Selepas memenuhi syarat arah aliran, nilai normalisasi ATR, nilai ADX dan syarat volum, persilangan emas EMA akhirnya akan mencetuskan isyarat beli.

Kelebihan Strategi

-

Gabungan pelbagai indikator, kebolehpercayaan yang lebih tinggi

Strategi ini mengintegrasikan pelbagai indikator seperti EMA, ATR, ADX, Super Trend, membentuk sistem penapisan isyarat yang kukuh melalui saling melengkapi, dengan kebolehpercayaan yang lebih tinggi.

-

Ruang pelarasan parameter yang luas

Parameter seperti ambang nilai normalisasi ATR, ambang ADX, kitaran pegangan boleh dioptimumkan mengikut keadaan sebenar, memberikan fleksibiliti strategi yang tinggi.

-

Dapat membezakan pasaran bull dan bear

Melalui indikator Super Trend, strategi ini menentukan pasaran bull atau bear, menggunakan standard parameter yang berbeza untuk pasaran bull dan bear, mengelakkan kehilangan peluang.

Risiko Strategi

-

Kesukaran pengoptimuman parameter yang tinggi

Gabungan parameter strategi adalah kompleks, menjadikan pengoptimuman sukar dan memerlukan ujian semula yang meluas untuk mencari parameter optimum.

-

Risiko pencetus isyarat palsu

Walaupun terdapat pelbagai penapisan, disebabkan sifat ketinggalan indikator, masih terdapat risiko pencetus palsu. Perlu mengambil kira teori henti rugi dengan secukupnya.

-

Kekerapan dagangan yang rendah

Disebabkan oleh pengaruh pelbagai indikator dan penapisan, kekerapan dagangan strategi ini akan menjadi agak rendah, dan mungkin tiada dagangan dalam jangka masa panjang.

Arah Pengoptimuman Strategi

-

Pengoptimuman gabungan parameter

Mencari kombinasi parameter indikator yang optimum melalui data ujian semula yang meluas.

-

Menambah pembelajaran mesin

Berdasarkan data sejarah yang banyak, menggunakan algoritma pembelajaran mesin untuk mengoptimumkan parameter strategi secara automatik, mencapai kebolehsuaian strategi.

-

Mempertimbangkan lebih banyak faktor pasaran

Menggabungkan lebih banyak indikator untuk menilai struktur pasaran, sentimen dan faktor lain, memperkayakan kepelbagaian strategi.

Kesimpulan

Strategi ini mempertimbangkan secara menyeluruh arah aliran, turun naik dan faktor harga volum, membentuk sistem dagangan melalui penapisan pelbagai indikator dan pelarasan parameter. Secara keseluruhan, strategi ini mempunyai kebolehpercayaan yang tinggi dan boleh meningkatkan kecekapan dagangan melalui pengoptimuman lanjut gabungan parameter dan kaedah pemodelan.

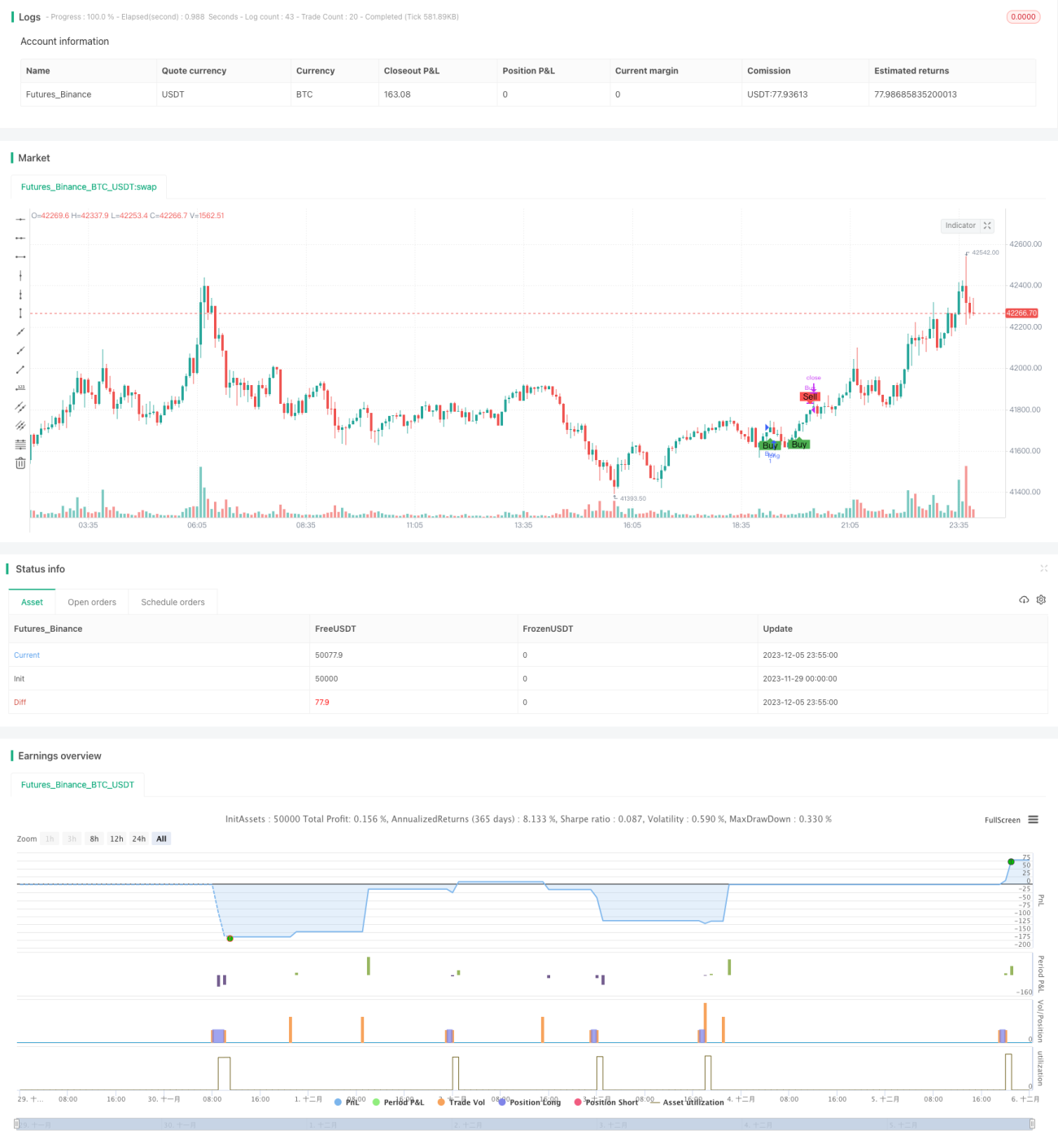

/*backtest

start: 2023-11-29 00:00:00

end: 2023-12-06 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//Description:

//This strategy is a refactored version of an EMA cross strategy with a normalized ATR filter and ADX control.

//It aims to provide traders with signals for long positions based on market conditions defined by various indicators.- 1