Chiến lược giao dịch Golden Cross hai đường EMA

Tổng quan

Chiến lược này kết hợp giao cắt vàng của hai đường EMA, bộ lọc nhiễu ATR chuẩn hóa và chỉ báo xu hướng ADX, nhằm cung cấp cho nhà giao dịch các tín hiệu mua đáng tin cậy hơn. Chiến lược tổng hợp nhiều chỉ báo để lọc các tín hiệu giả, xác định các cơ hội giao dịch đáng tin cậy hơn.

Nguyên lý chiến lược

Chiến lược này sử dụng EMA chu kỳ 8 và 20 để xây dựng hệ thống giao cắt vàng hai đường EMA. Khi EMA chu kỳ ngắn cắt lên trên EMA chu kỳ dài, tín hiệu mua được tạo ra.

Ngoài ra, chiến lược còn thiết lập nhiều chỉ báo phụ trợ để lọc:

-

ATR chu kỳ 14, được chuẩn hóa, lọc các biến động giá quá nhỏ trên thị trường.

-

ADX chu kỳ 14, dùng để nhận biết sức mạnh của xu hướng. Chỉ xem xét tín hiệu giao dịch khi xu hướng mạnh.

-

SMA khối lượng chu kỳ 14, lọc các thời điểm có khối lượng giao dịch nhỏ.

-

Chỉ báo Super Trend chu kỳ 4/14, xác định hướng thị trường tăng hay giảm.

Sau khi thỏa mãn các điều kiện về hướng xu hướng, giá trị ATR chuẩn hóa, giá trị ADX và khối lượng, giao cắt vàng EMA mới kích hoạt tín hiệu mua cuối cùng.

Ưu điểm của chiến lược

-

Kết hợp nhiều chỉ báo, độ tin cậy cao

Chiến lược tích hợp nhiều chỉ báo như EMA, ATR, ADX, Super Trend, hình thành hệ thống lọc tín hiệu mạnh mẽ nhờ sự bổ trợ lẫn nhau, độ tin cậy cao.

-

Không gian điều chỉnh tham số lớn

Các tham số như ngưỡng giá trị ATR chuẩn hóa, ngưỡng ADX, chu kỳ nắm giữ đều có thể tối ưu hóa theo tình hình thực tế, chiến lược linh hoạt cao.

-

Phân biệt được thị trường tăng và giảm

Sử dụng chỉ báo Super Trend để nhận biết thị trường tăng hay giảm, áp dụng các tiêu chuẩn tham số khác nhau cho từng loại thị trường, tránh bỏ lỡ cơ hội.

Rủi ro của chiến lược

-

Khó khăn trong tối ưu hóa tham số

Tổ hợp tham số chiến lược phức tạp, việc tối ưu hóa khá khó khăn, cần backtest nhiều để tìm ra tham số tối ưu.

-

Rủi ro kích hoạt sai

Mặc dù có nhiều lớp lọc, nhưng do bản chất của các chỉ báo vốn có độ trễ, vẫn tồn tại rủi ro kích hoạt sai. Cần cân nhắc đầy đủ lý thuyết cắt lỗ.

-

Tần suất giao dịch thấp

Chịu ảnh hưởng của nhiều chỉ báo và bộ lọc, tần suất giao dịch của chiến lược sẽ khá thấp, có thể không có giao dịch trong thời gian dài.

Hướng tối ưu hóa chiến lược

-

Tối ưu hóa tổ hợp tham số

Tìm tổ hợp tham số tối ưu của các chỉ báo thông qua dữ liệu backtest phong phú.

-

Thêm học máy

Dựa trên lượng lớn dữ liệu lịch sử, sử dụng thuật toán học máy để tự động tối ưu hóa tham số chiến lược, đạt được tính thích ứng của chiến lược.

-

Xem xét thêm các yếu tố thị trường

Kết hợp thêm nhiều chỉ báo để đánh giá cấu trúc thị trường, tâm lý và các yếu tố khác, làm phong phú thêm tính đa dạng của chiến lược.

Tổng kết

Chiến lược này xem xét tổng thể các yếu tố xu hướng, biến động và khối lượng-giá, hình thành hệ thống giao dịch thông qua lọc đa chỉ báo và điều chỉnh tham số. Nhìn chung, chiến lược có độ tin cậy cao, có thể nâng cao hiệu quả giao dịch bằng cách tối ưu hóa thêm tổ hợp tham số và phương pháp mô hình hóa.

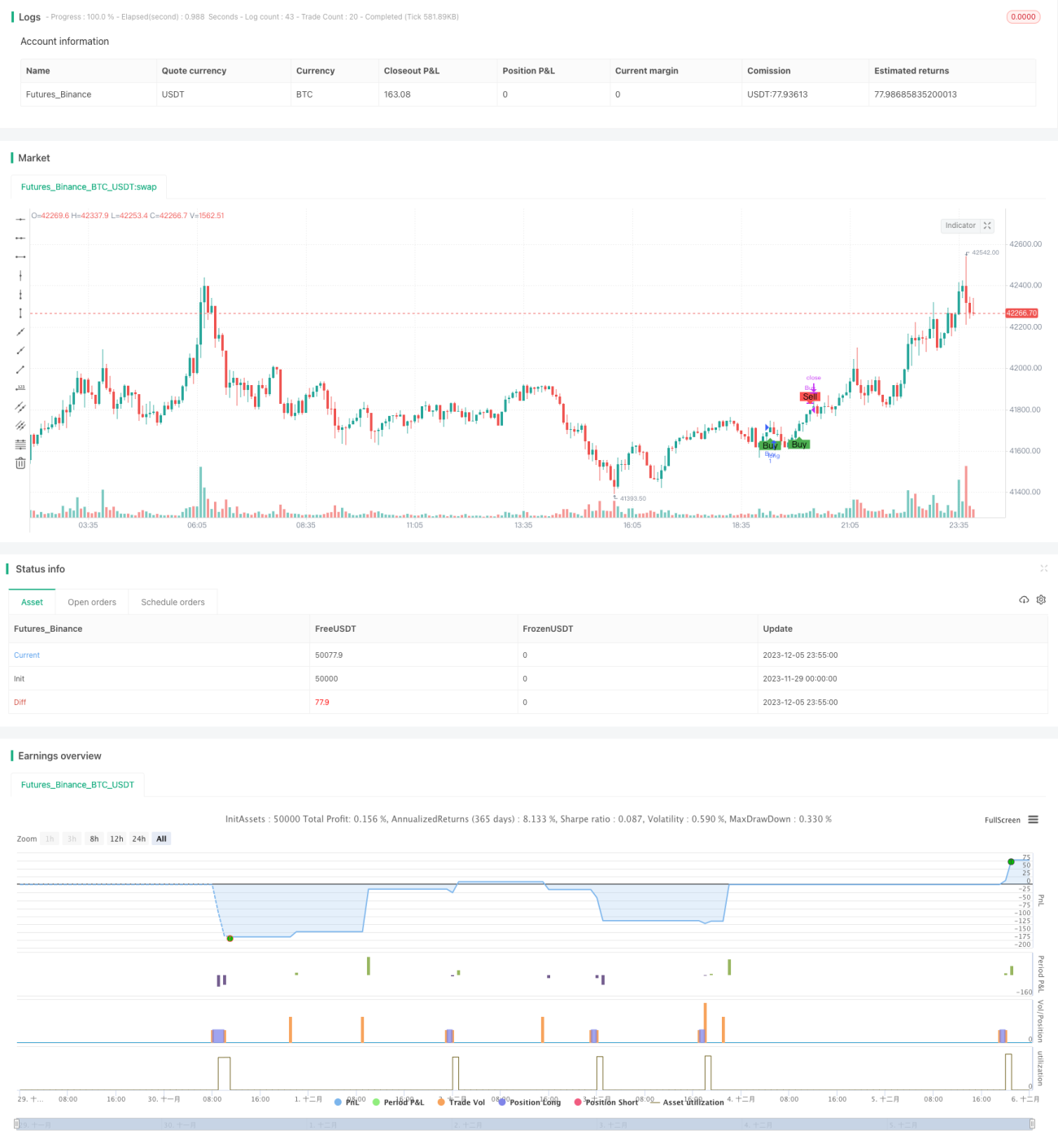

/*backtest

start: 2023-11-29 00:00:00

end: 2023-12-06 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//Description:

//This strategy is a refactored version of an EMA cross strategy with a normalized ATR filter and ADX control.

//It aims to provide traders with signals for long positions based on market conditions defined by various indicators.- 1