ダブル移動平均線クロスオーバー戦略

概要

これは移動平均線に基づくシンプルなアルゴリズム取引戦略です。短期と長期の移動平均線のゴールデンクロス(GC)とデッドクロス(DC)を利用して、買いと売りのタイミングを判断します。短期線が下から上に長期線を突き抜けた場合に買いシグナルが発生し、短期線が上から下に長期線を突き抜けた場合に売りシグナルが発生します。

戦略の原理

本戦略は主に移動平均線のトレンド追跡機能に基づいています。短期線のパラメータは小さく、価格変動に素早く反応します。長期線のパラメータは大きく、長期的なトレンドを表します。短期線が下から長期線を上回るということは、短期的な相場が反転し上昇トレンドに入ったことを意味します。逆に、短期線が上から長期線を下回るということは、短期的な相場が反転し下降トレンドに入ったことを意味します。これらのシグナルを捉えることで、トレンドに沿った取引が可能になります。

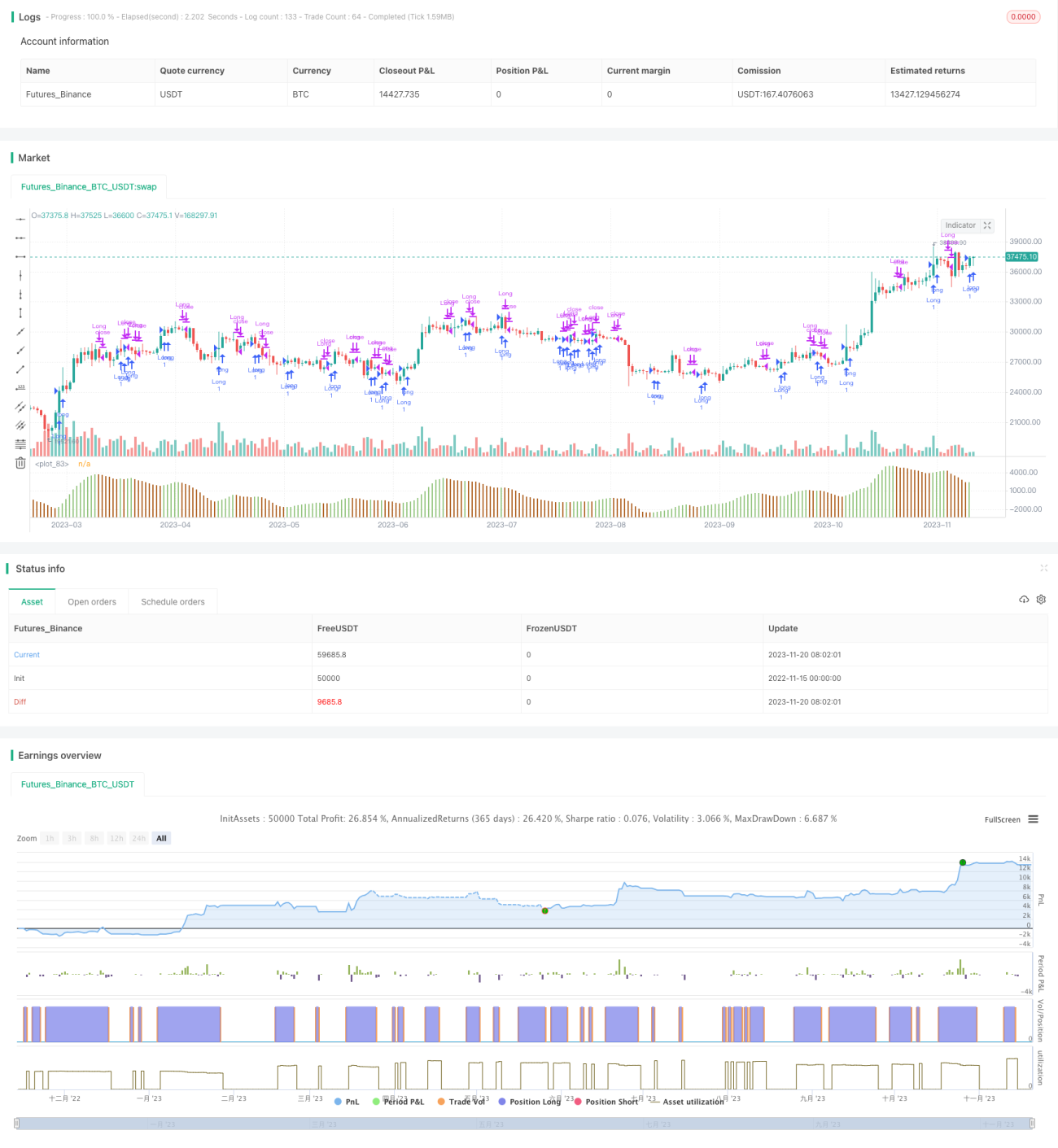

具体的には、本戦略では5日移動平均線(短期線)と34日移動平均線(長期線)の二重移動平均線を定義しています。毎日これら二つの移動平均線の値を計算し、短期線が下から上に長期線を突き抜けたかどうかを比較します。ゴールデンクロスが発生した場合はロング(買い)ポジションを取り、デッドクロスが発生した場合はポジションをクローズ(決済)します。

優位性分析

この戦略はシンプルで理解しやすく、実装も容易です。他の複雑な戦略と比較して、アルゴリズム取引の初心者により適しています。

二重移動平均線戦略は、市場のノイズを効果的にフィルタリングし、主要なトレンドを捉えることができます。短期線と長期線の日数パラメータを調整することで、異なる周期の相場変動に対応できます。

この戦略にはストップロス(損切り)メカニズムも組み込まれています。価格が逆方向に動き始め、短期線と長期線がデッドクロスを起こした場合、タイムリーに損切りを行うため、リスクを効果的にコントロールできます。

リスク分析

二重移動平均線戦略では、ストップロスが機能しない、曲線当てはめが失敗するなどのリスクが生じる可能性があります。具体的には、以下のような問題があります。

-

移動平均線には遅延性があるため、完全に反転した後にシグナルが発生することがあります。その場合、すでに得ていた利益が損失に変わってしまう可能性があります。

-

もみ合い相場では、偽のシグナルが何度も発生する可能性があります。これにより不必要な取引が増え、取引コストとスリッページ(滑り)損失が増大します。

-

本戦略はテクニカル指標に完全に依存しており、ファンダメンタル分析を組み合わせていません。重要なニュースに影響される相場では、効果が著しく低下する可能性があります。

-

ポジション管理とリスク管理が考慮されていません。予期せぬイベントにより戦略が破たんする恐れがあります。

最適化の方向性

本戦略の優位性を最大限に引き出し、リスクを低減するために、以下の点を最適化することが考えられます。

-

トレンド指標やボラティリティ指標と組み合わせ、より厳格なエントリー条件を設定し、偽のシグナルをフィルタリングします。例えばMACDやKDJ指標など。

-

適切なストップロスメカニズムを追加します。例えば、ゴールデンクロス後に一定の割合下落した場合に損切りする、または新高値(安値)形成後に一定の幅下落した場合に損切りするなど。

-

短期線と長期線の日数パラメータの組み合わせを最適化し、異なる周期の価格変動に合わせて調整します。パラメータの組み合わせ最適化により、最適なパラメータを探索できます。

-

市場全体のトレンドを判断するために株価指数を利用し、もみ合い相場での高頻度取引を避けます。

-

出来高の変化を組み合わせてトレンドシグナルの信頼性を検証します。例えば、出来高を伴ったブレイクアウトという条件を追加するなど。

まとめ

二重移動平均線戦略は非常に典型的なアルゴリズム取引戦略です。シンプルで直感的、実装が容易などの特徴を持ち、アルゴリズム取引の初心者が学び習得するのに非常に適しています。継続的なテストとパラメータ最適化により、良好な結果を得ることができます。しかし、この戦略にはシグナルの認識に遅れが生じる、偽のシグナルが発生しやすいなどの問題もあります。そのため、補助条件を追加してフィルタリングし、リスク管理を徹底することで、安定した収益を生み出す戦略にする必要があります。

/*backtest

start: 2022-11-15 00:00:00

end: 2023-11-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// This strategy is a modification to the "Bill Williams, Awesome Oscillator

// (AO) Backtest" strategy (Copyright by HPotter v1.0 29/12/2016)- 1