黄金分割式平均回帰トレンド取引戦略

概要

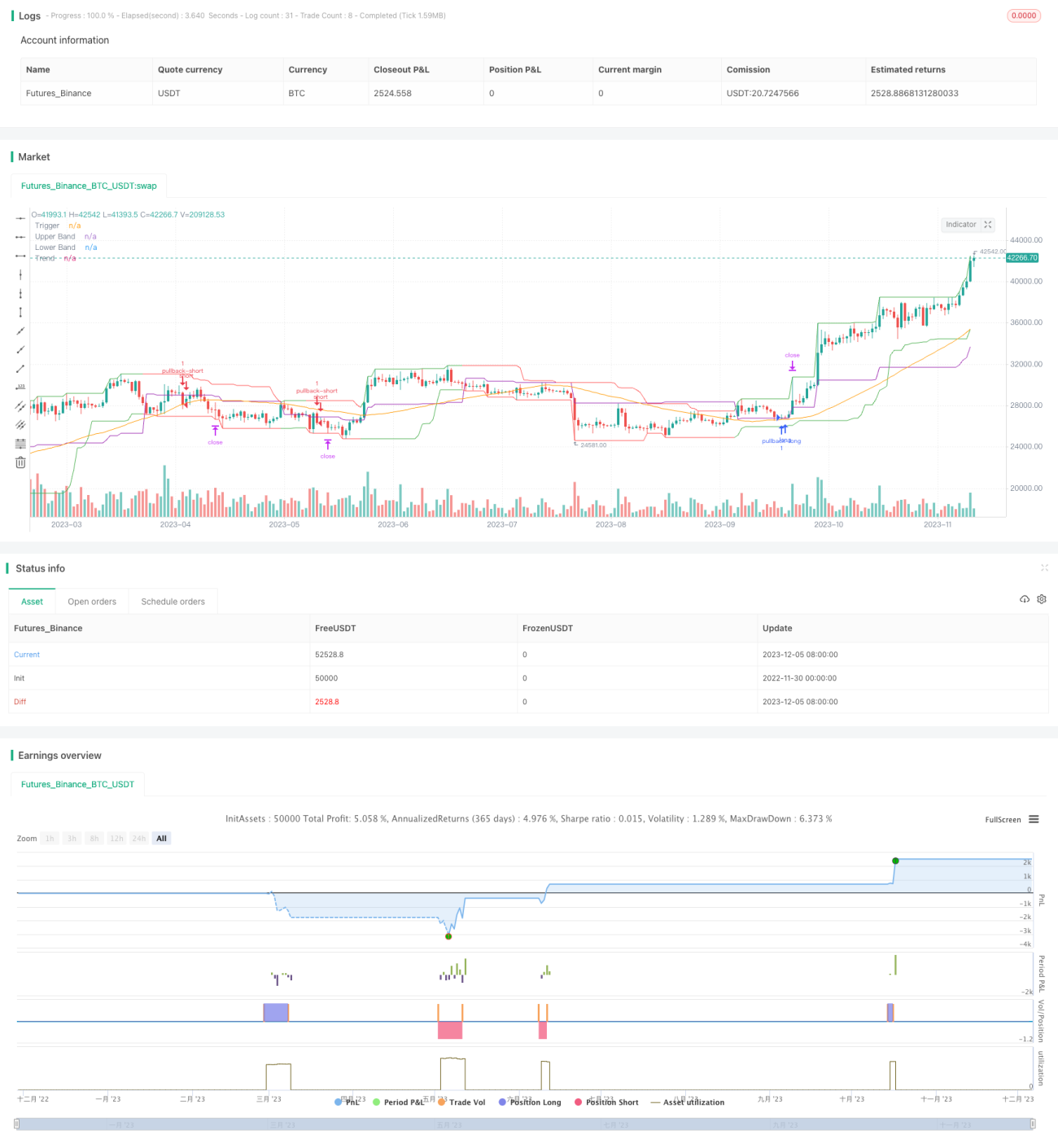

黄金分割による平均回帰トレンド取引戦略は、チャネル指標と移動平均線を活用して強いトレンド方向を特定し、価格が一定の割合でリトレースした後に、トレンド方向にポジションを開く戦略です。この戦略は、強いトレンド特性を持つ市場に適しており、トレンド相場で良好なパフォーマンスを得られます。

戦略の原理

この戦略の核となる指標は、チャネル指標、移動平均線、およびリトレーストリガーラインです。具体的には:

- チャネル指標は最高値と最安値から計算され、価格チャネルを特定するために使用されます。

- 移動平均線は、価格の全体的なトレンド方向を判断するために使用されます。

- リトレーストリガーラインは、価格がチャネルの境界から一定の割合で反発した後にポジションを開くために使用されます。

価格がチャネルの下限にタッチした場合、戦略は最安値を基準点として記録し、空売り許可フラグを設定します。価格が上昇した際、上昇幅がリトレース割合に達すると、反発点付近で空ポジションを開きます。

逆に、価格がチャネルの上限にタッチした場合、戦略は最高値を基準点として記録し、買い許可フラグを設定します。価格が下落した際、下落幅がリトレース割合の条件を満たすと、その付近で買いポジションを開きます。

したがって、この戦略の取引ロジックは、価格チャネルを追跡し、反転シグナルが発生した際に適切なポイントで既存のトレンドに介入することです。これはトレンドリトレース型取引戦略の一般的なパターンに該当します。

優位性分析

この戦略には主に以下の利点があります:

- 強いトレンド相場で良好なパフォーマンスを得られます。

- リトレース割合パラメータを調整することで、戦略のエントリーの厳格さを変更できます。

- 適切なドローダウンコントロールにより、1回あたりの損失を制限できます。

具体的には、戦略は主にトレンドの反転点でポジションを開くため、価格変動が大きくトレンドが明確な市場で効果的です。また、リトレース割合パラメータを調整することで、戦略のトレンド追跡の積極性を制御できます。最後に、ストップロス方式により1回あたりの損失を適切に管理できます。

リスク分析

この戦略には以下の主なリスクも存在します:

- 戦略は取引対象のトレンド特性に敏感です。

- リトレース割合の設定が不適切だと、過度に積極的または保守的になる可能性があります。

- ポジション保有期間が長くなる可能性があり、夜間リスクに注意が必要です。

具体的には、戦略を適用する取引対象のトレンド性が弱く、値動きが小さい場合、効果が低下する可能性があります。また、リトレース割合が大きすぎるか小さすぎると、戦略のパフォーマンスに影響を与えます。最後に、ポジション保有期間が長くなる可能性があるため、夜間リスクの管理にも注意が必要です。

上記のリスクを回避するために、以下の点を最適化することを検討できます:

- トレンド特性がより明確な取引対象を選択する。

- リトレース割合パラメータを調整し、最適なパラメータ組み合わせを探す。

- 利確Exitを設定し、ポジション保有期間を適切に制御する。

まとめ

黄金分割による平均回帰トレンド取引戦略は、シンプルな指標で価格トレンドとリトレースシグナルを判断し、強い相場でポジションを開いてトレンドを追跡する、典型的なトレンドシステムです。この戦略はパラメータ調整の余地が大きく、最適化により様々な市場環境に適応でき、リスク管理も合理的です。したがって、実戦検証と改善の価値がある戦略アプローチです。

/*backtest

start: 2022-11-30 00:00:00

end: 2023-12-06 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//

// A port of the TradeStation EasyLanguage code for a mean-revision strategy described at

// http://traders.com/Documentation/FEEDbk_docs/2017/01/TradersTips.html- 1