Estratégia de filtro de compra com indicador duplo para sinais de compra

Visão Geral

A estratégia de filtro duplo com sinal de compra utiliza a combinação do Índice de Força Relativa Estocástico (Stochastic RSI) e das Bandas de Bollinger para identificar potenciais oportunidades de compra. A estratégia emprega múltiplos critérios de filtro para distinguir os pontos de compra mais lucrativos. Isso permite identificar momentos de compra de alta probabilidade em ambientes de mercado voláteis.

Princípio da Estratégia

A estratégia utiliza dois conjuntos de indicadores para identificar oportunidades de compra.

Primeiramente, utiliza o Stochastic RSI para determinar se o mercado está sobrevendido. Esse indicador combina o oscilador estocástico com sua média móvel suavizada. Quando a linha %K cruza acima da linha %D a partir de um ponto baixo, é considerado um sinal de sobrevenda. Aqui, é definido um limite: quando a linha %K está acima de 20, já é considerado sobrevenda.

Em segundo lugar, a estratégia utiliza as Bandas de Bollinger para identificar alterações de preço. As bandas são calculadas com base no desvio padrão dos preços, definindo bandas superiores e inferiores. Quando o preço se aproxima da banda inferior, é considerado um estado de sobrevenda. A estratégia define aqui um parâmetro de 2 desvios padrão, ampliando a faixa das bandas, filtrando assim mais sinais falsos.

Após obter os sinais de sobrevenda dos dois indicadores acima, a estratégia adiciona múltiplos critérios de filtro para identificar ainda mais o momento de compra:

- O preço acabou de romper a banda inferior das Bandas de Bollinger para cima.

- O preço de fechamento atual é superior ao preço de fechamento de N velas atrás, indicando força de compra.

- O preço de fechamento atual é inferior ao preço de fechamento do período de retrospectiva de longo ou médio prazo, favorecendo uma correção.

Após a avaliação combinada, quando um momento de compra é identificado, um sinal de compra é emitido.

Análise de Vantagens

Esta estratégia de filtro duplo possui várias vantagens:

- A utilização de dois indicadores torna o sinal de compra mais confiável, evitando sinais falsos.

- Múltiplos critérios de filtro evitam compras frequentes em mercados laterais.

- Combina o indicador estocástico para avaliar a sobrevenda e as Bandas de Bollinger para identificar anomalias de preço.

- Acrescenta um julgamento de força de preço, garantindo impulso de compra suficiente.

- Adiciona uma verificação de correção, aumentando ainda mais a confiabilidade do ponto de compra.

Em resumo, a estratégia integra múltiplos indicadores técnicos e meios de filtragem, tornando a identificação do momento de compra mais precisa e confiável, resultando em um melhor desempenho nas negociações.

Análise de Riscos

Embora a estratégia de filtro duplo tenha muitas vantagens, também existem alguns riscos a serem considerados:

- Uma configuração inadequada de parâmetros pode tornar os sinais de compra excessivamente frequentes ou conservadores, exigindo testes e otimizações cuidadosos.

- Múltiplos critérios de filtro podem perder algumas oportunidades de compra, não acompanhando movimentos rápidos do mercado.

- Quando os indicadores divergem, podem gerar sinais falsos, sendo necessário monitorar a consistência dos indicadores.

- A incapacidade de julgar a tendência pode gerar sinais falsos em mercados de baixa, resultando em perdas.

Para mitigar esses riscos, a estratégia pode ser otimizada da seguinte forma:

- Ajustar os parâmetros dos indicadores para equilibrar a sensibilidade dos critérios de filtro.

- Com a ajuda de um indicador de tendência, evitar sinais falsos em mercados de baixa.

- Adicionar mecanismos de stop loss.

Direções de Otimização

A estratégia de filtro duplo pode ser ainda mais otimizada nas seguintes dimensões:

- Testar combinações de mais indicadores técnicos para encontrar melhores formas de julgar o momento de compra, como VRSI, DMI, etc.

- Adicionar algoritmos de aprendizado de máquina para otimizar automaticamente os parâmetros.

- Adicionar um mecanismo de stop loss adaptativo. Quando o lucro atinge um certo nível, elevar gradualmente o nível de stop loss.

- Combinar indicadores de volume para garantir força de compra suficiente.

- Otimizar a estratégia de gerenciamento de capital, definindo quantidades dinâmicas de negociação para reduzir perdas por operação.

Ao introduzir tecnologias e métodos mais avançados, esta estratégia de filtro duplo pode obter uma seleção mais precisa do momento de compra e uma capacidade de controle de risco mais forte, resultando em retornos mais estáveis e confiáveis em negociações reais.

Resumo

Em suma, a estratégia de sinal de compra com filtro duplo utiliza vários indicadores técnicos como Stochastic RSI e Bandas de Bollinger, combinados com múltiplos critérios de filtro como força de preço e verificação de correção, para identificar momentos de compra de alta probabilidade e confiáveis. Com a otimização de parâmetros, definição de stop loss e outros aprimoramentos, essa estratégia pode se tornar uma das estratégias de negociação quantitativa com retornos estáveis.

Sua principal vantagem reside na combinação eficaz de indicadores e critérios de filtro, tornando o julgamento do momento de compra mais preciso. Os riscos e as direções de otimização são controláveis e solucionáveis. No geral, é uma estratégia quantitativa eficiente aplicável em negociações reais.

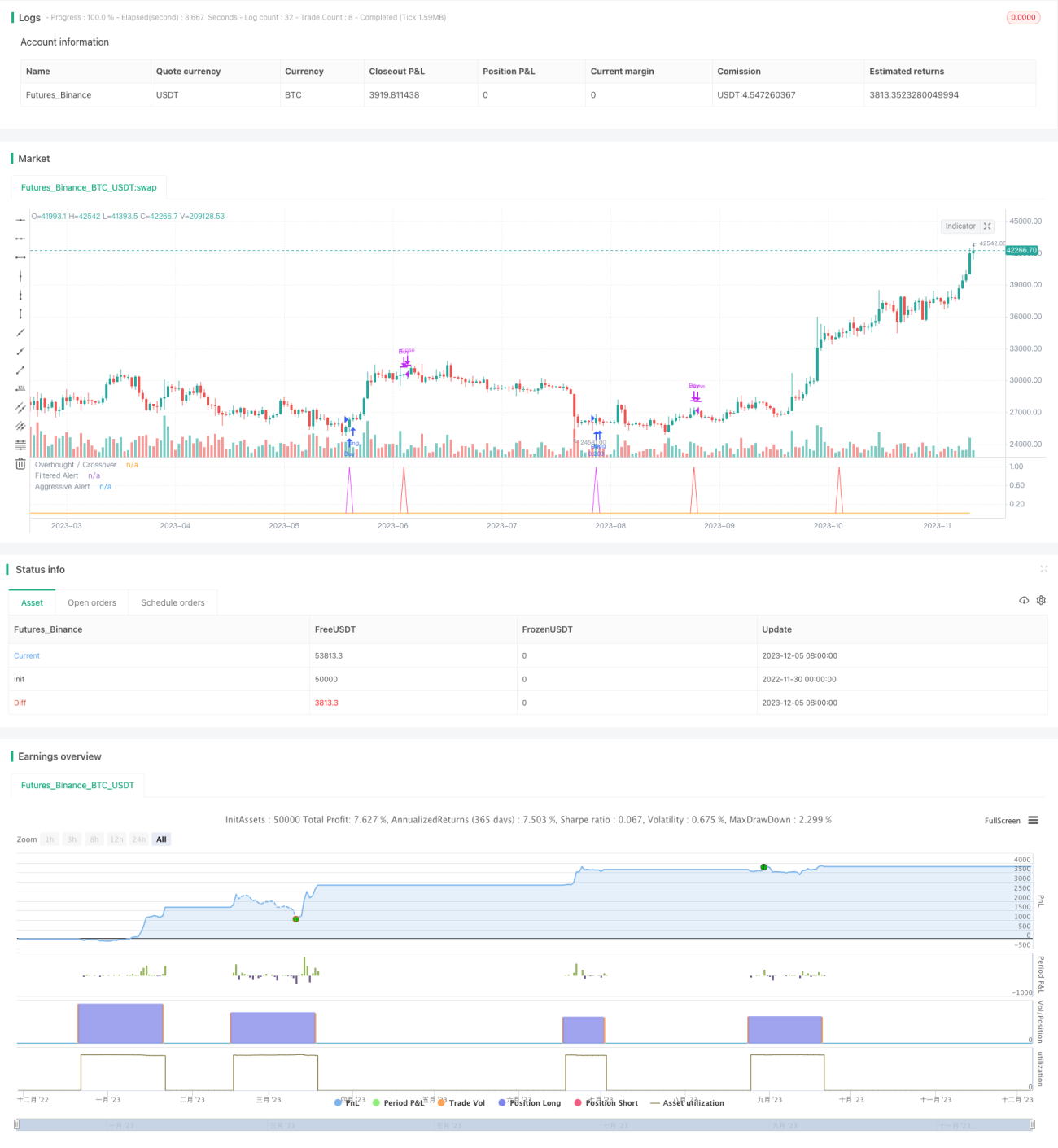

/*backtest

start: 2022-11-30 00:00:00

end: 2023-12-06 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SORAN Buy and Close Buy", pyramiding=1, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=10, overlay=false)

////Buy and Close-Buy messages- 1